People

Topics

Share

It has been 30 years since the Family and Medical Leave Act (FMLA) was passed at the federal level under former President Bill Clinton. FMLA grants eligible employees with unpaid, job-protected leave for qualifying family and medical reasons with continued employer-sponsored group health insurance coverage, if applicable. Since then, some adjustments to FMLA have been made, such as the inclusion of workers with a family member in the military and those in a legal, same-sex marriage. However, the evolution has been slow and limited; many believed or at least hoped that over time FMLA would evolve into a paid leave model, but over the last three decades, it is states that have taken initiative in establishing PFML programs for their workers.

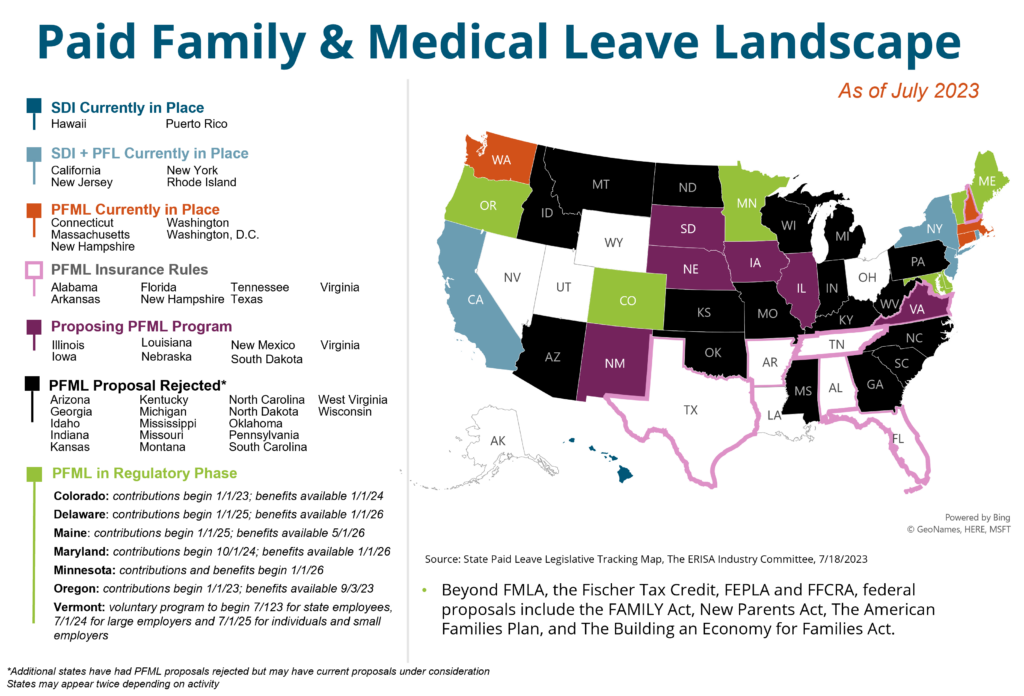

Starting with California in 2004, 11 states and Washington, D.C. now have some type of established PFML program, with several other states including Maryland, Colorado, and, most recently, Minnesota, in the regulatory phase where a law has passed but benefits are not yet available. Plans vary by percentage of wage replacement, maximum weekly benefits, the contribution split between employer and employee, benefit duration, and other factors. The newest trend in PFML law, however, relates to PFML as an insured product.

PFML Insurance Rules

Recently, states including Virginia, Tennessee, Florida, and Alabama have passed legislation related to a voluntary PFML insurance product, as opposed to the more traditional, mandatory PFML programs that we had been seeing in previous years. With this new model, state laws create a new line of family leave insurance that may be written as an amendment or rider to a group disability income insurance policy, or as a separate group insurance policy purchased by an employer.1 Employers may offer the product for their employees without obligation to do so, in a setup similar to other voluntary benefits like short-term disability or vision insurance. In this way, it is purchased through an employer but at the individual’s expense and discretion and a third party insurance carrier is used to carry out the program.

As an example, under the Tennessee Paid Family Leave Insurance Act, a new line of insurance called paid family leave (PFL) insurance has been established. It can be offered as a rider or included in a policy for short-term disability, life insurance, or as a standalone PFL policy. Qualifying reasons for a leave of absence include the birth or adoption of a child, placement of a child for foster care, care for a family member with a serious health condition, and reasons related to a family member’s active military duty. The insurance is purchased through an employer arrangement, but unlike the voluntary program launched this year in New Hampshire, there are no tax incentives for employers who offer the PFL product.

Preliminary Results

PFML as an insurance product is a new concept that we expect to evolve over time.

Take-up by employers will likely vary on their size, culture, geographic spread, and most importantly their current benefit offerings. Some employers may appreciate the model law as a guide to providing a new benefit for employees, or a competitive benefit to what is offered in other states so that equity could be achieved across locations. Others could feel it is too costly for them to offer, or they may already have equivalent benefits in place. Whatever the case, employees are becoming increasingly aware of these laws, and employers need to be ready to explain why they are or are not supporting them.

At the state level, it may be an intermediary step to the establishment of a mandatory PFML program, or it may be a way of offering some benefit without the budgetary and resource constraints required to build out a more traditional plan.

This new wave of PFML laws is just getting started, however, and our team will be closely monitoring utilization and legislative developments. In the meantime, check out our absence management services here or get in touch with our team if you have questions about the direction of PFML.

1 (2023). Absence Advisory June 2023. Aflac

Related Content

Point Solution Spotlight: Employer Strategies for Menopause Support

Menopause support has rapidly shifted from a taboo topic to a fast-growing area of interest in an employer’s benefits offering, […]

Home Diagnostic Testing: What Employers Need to Know Now

Implications for Cost, Care Quality, and Employee Engagement At-home diagnostic testing has shifted from a convenience to a standard part […]

Captive Review: POWER 50 2026: Prabal Lakhanpal #14

Every year, Captive Review releases their Power 50 list, which spotlights top professionals in the world of captive insurance. This year our […]