You’ve had your P&C captive for years and it has continued to perform well throughout. So, what next? How do you capitalize on this success and build on your captive or rebuild an underperforming aspect of it? One word: Refeasibility. Okay, so ‘refeasibility’ isn’t really a word (according to Oxford Dictionary). At least it hasn’t been traditionally, but it is one that needs to be on the tip of the tongue of every captive owner. It is a word that has become somewhat synonymous with captive optimization and very accurately describes what captive owners need todo with an older captive: conduct a new (re)feasibility study.

The Importance of Refeasibility

As with all other business matters, your company’s captive needs and goals are likely to change over time, especially with new and emerging risks sprouting up frequently. Much like your family car, a captive should have a check up on a periodic basis. As a captive matures and companies evolve, captives need to be re-examined to determine if changes should be made to align with current organizational needs. Key reasons for this re-examination include the following:

- Positive or negative experience

- Example: unexpected adverse loss experience, such as supply chain interruption, resulting in business income loss not covered by insurance

- Surplus release or addition

- Example: surplus growth for the captive has been good and, as a result, there is now opportunity to add/expand coverages insured in the captive

- Opportunities to add new lines of coverage (that perhaps didn’t exist or weren’t relevant before)

- Example: Employee benefits or cyber risk

- Change in the risk profile of various risks

- Example: Litigiousness is on the rise in the insured’s industry and additional protection is needed

- Changes in the regulatory environment

- Generally speaking, regulatory changes have impacted business directly or indirectly, resulting in loss of revenue. This is a leading concern for small business owners.

- Changes in law (such as those resulting from case law outcomes like the recent Commissioner vs. Avrahami case)

To address all these potential changes, our Spring CARE (Captive Analytical Risk Evaluation) team recommends a captive evaluate its risk appetite and risk exposure at least every five years. Are you still writing the right lines in your captive? Are you still in the right domicile? Would a different structure be more profitable? Would other service providers make a difference? Have your claims changed significantly? Have regulations changed over the years? All this and more can be answered with a good review of your captive by a professional consultant.

Captive optimization starts with a captive refeasibility study. Every refeasibility study is different to varying degrees; the scope and resources required to conduct the study are dependent on the captive’s current structure, the events (if any) that triggered the study and the goals of the company. That said, through our Spring CARE system, we follow a carefully-constructed evaluation structure when our team works through the process of evaluating captive client’s existing captive. Generally speaking, we follow and recommend the following process in conducting a refeasabiity study, starting with goals and ending with measurement.

Goals Stage

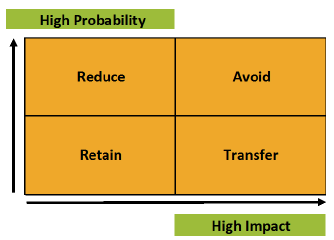

In this initial stage, it is important to focus on confirming the goals and objectives of your captive, both new and old. Have the older goals been achieved? How have the goals changed over the years? This is acritical step in laying the groundwork and direction of your refeasibility project. Also critical at this early point is the collection of data. We consider the data to be collected here as not only the stats and facts of the captive, but also the more subjective (non-paper) data that can be gleaned through management interviews and informal stakeholder surveys. Finally, in any good refeasibility study, it is very important to identify changes in your risk profile. The risk matrix to the right shows the four classic actions a company can use to handle each of their risks (DeLoach 2000).

Typically, high probability or high impact risks should be considered for insuring in your captive. Some of the most common risks to insure in captives are listed below . Emerging risks should also be considering in this assessment. For example, A new technology like driverless cars will create both risk and/or opportunities across various industries.

Coverages commonly written into captives:

| Employee Benefits Risk | Property & Casualty Risks |

| AD&D | Auto Liability |

| Life/Loss of Key Employee | Business Interruption |

| Long-Term Disability | Directors & Officers Liability |

| Medical Stop-Loss | General Liability |

| Voluntary Benefits | Professional Liablity |

| Retiree Benefits | Property (deductible or excess layer) |

| Pension Buy-Outs/Buy-Ins | Trade Credit |

| Workers’ Compensation | |

| Commercial Policy Excluded Risk |

Impact Stage

You want to be sure you have a clear idea of what you’re looking to accomplish, and to what extent. The Impact Stage of a refeasibility study involves looking at all the different pieces of t he captive puzzle to determine how they would be affected by the changes you’re considering. A few activities that a professional captive optimizer would look to accomplish in this phase would be:

- Conducting an analysis of your risk financing optimization

- Reviewing your current reinsurance levels and optimizing your reinsurance use

- Stress testing of the captive with reasonable adverse case outcomes

Strategies Stage

It’s important to outline the methods you plan on utilizing in your captive refresh; in this Strategies Phase, a professional captive optimizer would first analyze any additional lines of coverage that could be insured by your captive.

Secondly, a surplus management strategy would be developed. There are various considerations in appropriately managing the capital and surplus levels over the life of a captive, including average cost of capital, retention levels, reinsurance use, taxes and a number of others that a team of actuaries and consultants would review and develop strategy to address.

Structure Stage

Now that you know what you want to do and how, it’s time to take a closer look at how it will all work together in a logical structure. Market changes should give you some food for thought. For example, pure captives are increasingly changing to sponsored entities. In this Structure Stage, it is important to identify investment management best practices as well as the optimal collateral structure.

Measurement

Finally, all sound captive projects end with measurement. This is the time to collect new data and determine to what extent goals were met, and impacts made. A great deal of this stage relies on the creation of solid industry benchmarks to measure current and future captive performance against. It is also important in the Measurement Stage for the optimization team to develop implementation plans based on their findings and make actionable recommendations for helping you achieve the goals that were established in the first phase of this project. At the conclusion of the measurement phase, a professional captive optimization team, such as our Spring CARE team, would produce a refeasibility report for your captive. In this report, all of the findings of the refeasibility study are outlined and reviews along with the recommendations developed in this phase. These findings can serve as a base line for measurement.

Conclusion

Regardless of how old or new your captive is, there are a number of internal and external factors that have changed since it was created. With all the changes taking place in the industry, it is a great time to have a professional come in and not only take a snapshot of how your captive is currently performing, but also help you project and strategize where your captive should be in the future. Now is a great time for a captive refeasibility study.

Related Content

Captive.com: Property Captives Flourish Despite Softening Market

Our VP, TJ Scherer, was quoted in an article from Captive.com, titled “Property Captives Flourish Despite Softening Market”, he explained […]

Captive Review: 2025 US Awards Shortlist (Spring Consulting Group)

Spring Consulting Group, an Alera Group Company, has been shortlisted in Captive Review’s 2025 US Awards in the following categories: […]

Business Insurance: Spring Consulting Group Listed in 2025 U.S. Insurance Award Finalists

Spring Consulting Group, An Alera Group Company was listed as a finalist in Business Insurance’s 2025 U.S. Insurance Award Finalists. You […]