Every year, Captive Review releases their Power 50 list, which spotlights top professionals in the world of captive insurance. This year our SVP, Prabal Lakhanpal was featured on the list at #14. Check out the full article here.

Pension risk transfer (PRT) strategies, particularly buy-ins and buy-outs, have become a cornerstone for organizations looking to reduce pension-related risk and expense. Over the past several years, transaction volume has exceeded $45 billion annually, with recent activity surging in Q4 to $28 billion, driven by the largest quarter of buy-ins in US history.1

On paper, the story is clear. Strong funding levels, favorable economic conditions, and a competitive insurance market have created the ideal environment for action.

But there is a more important question beneath the surface. Are organizations choosing the best strategy, or simply the most familiar one?

Although traditional insurance is common, simplicity should not be confused with efficiency.

The Hidden Trade-Off in Commercial Transactions

Commercial insurance solutions are built to generate profit. That reality is embedded in every transaction.

Pricing typically includes:

- Risk margins

- Capital charges

- Administrative costs

- Insurer profit

These are not minor line items. They are fundamental components of the structure. So while a buy-out may deliver a clean accounting outcome, it often comes at a premium that exceeds the true economic value of the obligation. In other words, organizations may be reducing risk, but they are also giving away value.

A Smarter Alternative: Captive Buy-Ins and Buy-Outs

A growing number of plan sponsors are rethinking the default by leveraging captive insurance companies to execute buy-ins and buy-outs. This approach shifts the equation. Instead of transferring both risk and economics to a third party, organizations can retain greater control while still achieving meaningful risk transfer.

Why Captives Change the Equation

Who Should Consider this Option?

The transaction can be structured in a myriad of ways that allows ultimate flexibility to plan sponsors while maximizing savings and financial stability. Frozen and accruing plans alike can take advantage of captive strategies. The real issue is not feasibility. It is that most organizations have only been shown one path.

Captive strategies introduce a more deliberate approach. One that reduces cost, preserves control, and aligns financial outcomes more closely with long-term objectives. For organizations willing to challenge convention, the opportunity is significant.

Start the Conversation

For organizations evaluating their PRT strategy, the path forward does not have to be limited to traditional options. The most effective approach starts with understanding the full range of what is possible and aligning that strategy with your financial and operational goals.

Spring Consulting Group has been at the forefront of designing and implementing captive-based PRT solutions, helping organizations move beyond one-size-fits-all transactions toward more efficient, controlled outcomes. If you are exploring your next step, now is the time to ask a different set of questions and consider whether your current approach is truly optimal. Connect with your Spring Consulting Group contact to continue the conversation.

1LIMRA: U.S. Single Premium Pension Risk Transfer Product Sales Jump 132% in the Fourth Quarter of 2025 https://www.limra.com/en/newsroom/news-releases/2026/limra-u.s.-single-premium-pension-risk-transfer-product-sales-jump-132-in-the-fourth-quarter-of-2025

Overview

The medical stop-loss market is experiencing significant upheaval as claim frequency and severity reach unprecedented levels. These developments have fundamentally altered the pricing landscape, with carriers adjusting their strategies in response to deteriorating loss ratios and mounting claim costs.

Rising Claims: Frequency and Severity

In 2025, claims well exceeded target loss ratios. The surge in stop-loss claims reflects broader trends in the healthcare market. Three primary factors are driving this increase: rising costs per medical service, higher incidence rates of severe diagnoses, and the introduction of expensive new treatments, drugs, and therapies. While these developments were anticipated given long-term healthcare cost trends, the magnitude and pace of change have exceeded many projections.

Cancer remains the dominant driver of stop-loss claims across the market, leading in both claimant count and total claim dollars. Cardiovascular conditions typically rank second, while newborn complications have emerged as a significant contributor, particularly for claims exceeding $1 million. Although cell and gene therapies have not yet been major contributors to historical claims, they represent a growing risk. The proliferation of these therapies is expected to further exacerbate both the frequency and severity of large claims in the coming years.

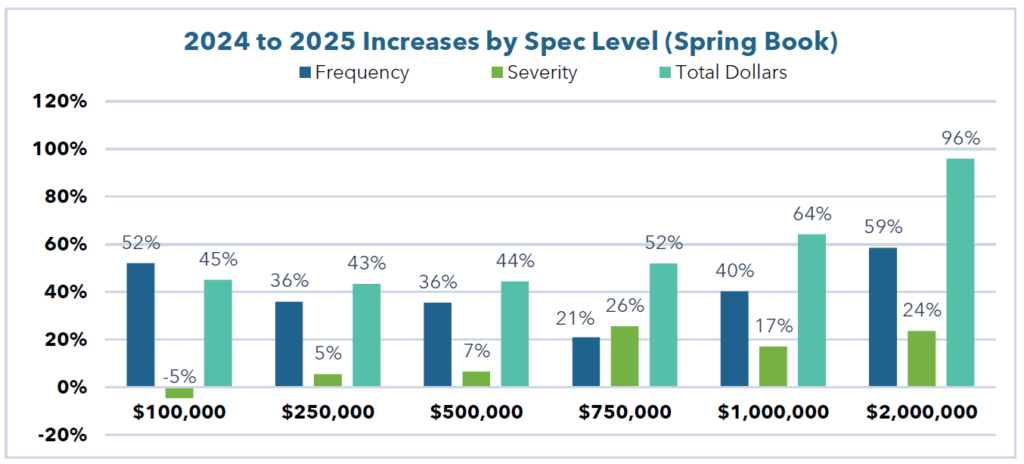

Reviewing data across our book of business and the broader industry reveals a significant acceleration in large-claim frequency across multiple threshold levels:

Claims exceeding $250,000 have grown substantially across the industry. Voya reported an 11% increase from 2023 to 20241. Spring’s internal data shows a more dramatic trajectory, with a 27% frequency increase from 2023 to 2024, followed by a 36% jump from 2024 to 2025 (a 72% cumulative increase from 2023 to 2025). In addition to increased frequency, severity rose by 21% on a per-claimant basis from 2023 to 2025, with total claim dollars for claims exceeding $250,000 increasing by 108% on a PEPM basis.

For claims above $500,000, the trend is equally concerning. TMHCC reported a 113% frequency increase from 2021 to 2024, including a 35% increase from 2023 to 2024 alone2. Internal data reflects a 95% increase in frequency from 2023 to 2025 (36% from 2024 to 2025), coupled with a 29% increase in per-claimant severity over the same period (7% from 2024 to 2025). As a result, total claim dollars exceeding $500,000 surged by 152% from 2023 to 2025 (44% from 2024 to 2025).

At the $750,000 threshold, Voya documented a 15% frequency increase from 2023 to 20241. Internal analysis shows a 21% frequency increase from 2024 to 2025, along with a 26% severity increase over the same period. Total claim dollars above $750,000 rose by 52% from 2024 to 2025. Comparing 2023 to 2025, frequency increased by 115%, per-claimant severity increased by 45%, and total claim dollars increased by 190%.

Million-dollar claims present perhaps the most striking picture. Sun Life reported a 61% increase in frequency from 2021 to 2024, including a 29% increase from 2023 to 20243. TMHCC reported a 113% frequency increase from 2021 to 2024, with a 35% rise from 2023 to 20242. QBE documented a 49% increase from 2021 to 2024 and a 32% increase from 2023 to 20244. From 2022 to 2025, Spring’s internal data shows a 131% increase in frequency. Total claim dollars exceeding $1 million have increased by over 200% from 2023 to 2025.

At the highest threshold of $2 million, TMHCC reported frequency increases of 105% from 2021 to 2024, 65% from 2022 to 2024, and 22% from 2023 to 20242. Internal data shows a 59% frequency increase from 2024 to 2025 and a 162% increase from 2022 to 2025. Total claim dollars on claims over $2M have increased 96% from 2024 to 2025.

Impact of Pharmacy Claims

Pharmacy claims have steadily increased as a percentage of total claims over the past several years, both for underlying medical claims and stop-loss claims. Across one client block, we have seen pharmacy’s share of claims for stop-loss claimants more than double from 2019 to 2025 (from under 15% of claims to 30%). This underscores the growing role of pharmacy costs not only in aggregate claim spend, but specifically among high-cost stop-loss claimants.

Carrier Loss Ratio Deterioration

The surge in claims has materially impacted carrier profitability. Many major carriers reported higher loss ratios in 2024 compared to 2023, including industry leaders such as Cigna and United5,6. Cigna explicitly identified stop-loss as the primary driver of its increased loss ratio, highlighting the outsized impact of this line of business6.

Market Hardening and Premium Increases

The combination of rising claims and deteriorating loss ratios has prompted a fundamental shift in carrier behavior. Double-digit premium increases have become commonplace and are directly attributable to the underlying claim trends. However, the current premium environment reflects more than actuarial updates to projected claims.

The market has entered a hardening phase as carriers shift their strategic focus from growth to profitability. This shift has reduced the competitive pressure that previously constrained premium increases. Carriers are demonstrating less willingness to aggressively price for new business, recognizing that underpricing in the current environment poses unacceptable financial risk.

In their 2025 survey, Aegis reported stop-loss premium increases of 9% to 11%, with long-term premium growth expected to range from 10% to 12%8. These figures likely understate future increases, as 2025 rates were developed using partial 2024 claims data. Continued deterioration in claim experience through 2025 is expected to drive further premium escalation in 2026 and 2027.

This dynamic has created a compounding effect on premiums. Rates are first increasing to reflect higher projected claims and then receiving additional upward pressure as carriers apply less aggressive pricing relative to those projections. The result is a premium environment shaped by both actuarial realities and a strategic recalibration of carrier risk appetite.

The Role of Captive Insurance Companies

Captive insurance companies help employers manage total cost of risk by retaining a portion of medical stop-loss risk in house, allowing organizations to capture risk margin that would otherwise go to the commercial carriers. This becomes increasingly valuable in a hardening market, where carriers embed greater margin into premium rates.

QBE reports increased interest in medical stop-loss captives and notes that captives have delivered great value to employers4. Stealth estimates that captives now represent 10% of the MSL market7. Across our own book of business, we have observed many clients achieve strong results through stop-loss captive structures.

Outlook

The convergence of accelerating claim frequency, rising severity, and market hardening suggests that the current premium environment is likely to persist in the near term. Absent a reversal in underlying healthcare cost trends or the introduction of effective cost-containment measures, employers and plan sponsors should expect continued upward pressure on stop-loss premiums.

The market appears to be in a transitional phase, with carriers recalibrating pricing models to reflect a new reality of elevated claim costs and reduced tolerance for underpricing risk.

1Voya. Stop Loss Paid Claims Analysis 2025. Available at: https://www.voya.com/voya-insights/stop-loss-paid-claims-analysis-2025

2TMHCC. 2025 Annual Report. Available at: https://www.tmhcc.com/en-us/-/media/project/tokio-marine/tmhcc-us/documents/2025-annual-report.pdf

3Sun Life. Medical Stop Loss Market Report. Available at: https://sunlife.showpad.com/share/O4RCCHRh9ke9xod6BdbOz

4QBE. 2025 Accident & Health Market Report. Available at: https://www.qbe.com/media/qbe/north-america/usa/files/accident-health/2025-ah-market-report.pdf

5Becker’s Payer Issues. Payers Ranked by 2024 Medical Loss Ratios. Available at: https://www.beckerspayer.com/payer/payers-ranked-by-2024-medical-loss-ratios/

6The Cigna Group. Fourth Quarter and Full Year 2024 Results. Available at: https://newsroom.thecignagroup.com/2025-01-30-The-Cigna-Group-Reports-Fourth-Quarter-and-Full-Year-2024-Results,-Establishes-2025-Outlook-and-Increases-Dividend

7Stealth Partner Group (Amwins). State of the Market 2025. Available at: https://www.amwins.com/docs/default-source/external-linked-documents/stealth-docs/stealth_sotm_2025.pdf

8Aegis. 2025 Medical Stop-Loss Premium Survey. Available at: https://www.aegisrisk.com/stop-loss-premium-survey

Spring Consulting Group, an Alera Group Company, has been shortlisted in Captive Review’s 2026 US Awards in the following categories:

- Actuarial Firm

- Captive Broking Services

- Captive Consultant

- Captive Service Professional (TJ Scherer)

- Emerging Talent (Aviel Shalev)

- Employee Benefits Specialist

You can access the full shortlist here.

The 2026 CICA International Conference once again proved why it is the premier gathering for the captive industry, bringing together a vibrant mix of seasoned experts and “NextGen” leaders of tomorrow. As the only non-domiciled captive insurance association, CICA provides a unique opportunity for stakeholders across the captive space to network, engage in insightful sessions and discuss market trends. Here are the pivotal topics that defined the 2026 conference.

Optimizing Legacy Captive Programs

As the captive industry matures, many organizations are shifting their focus from initial formation to the long-term optimization of existing structures. This year’s sessions emphasized the importance of periodic “checkups”, which can help ensure a legacy captive continues to drive maximum enterprise value in a shifting market. Some notable sessions include:

-The session, “Strategic Use of Captives in Employee Benefit Design” provided actionable insights to turn stop-loss programs into strategic, sustainable solutions that support long-term healthcare financing objectives.

– The presentation, “Unlocking Efficiency: Integrating Employee Benefits & P&C Captives for Strategic Risk Management” featured a detailed case study exploring how integrating employee benefits captives with property & casualty (P&C) captives can unlock new efficiencies, reduce costs, and create more resilient risk management structures.

– The session, “The Power of Diversification: Strengthening Captives Across Risk Types”, featured risk managers from IGH Hotels and UCLA, along with Spring’s Chief P&C Actuary, who discussed the advantages of multi-line captives and shared their firsthand experiences

– An exclusive training for domicile regulators, titled “Leveraging Captives for Medical Stop Loss and Employee Benefits”, focused on potential pitfalls and challenges regulators should be aware of to ensure proper oversight and effective regulation of captives in this area.

Talent Development and “NextGen” Initiatives

With a strong emphasis on mentorship and soft skills, several sessions focused on how we can support junior colleagues as they develop into future leaders in the captive space. Empowering the next generation is vital for maintaining the momentum of the industry as veteran leaders begin transitioning out of their roles. Here are some presentations we found particularly valuable:

– The session, “Cultivating the Next Generation of Leaders: Attracting and Mentoring Young Talent” focused on how we can better attract and engage the next generation of leaders by promoting industry visibility, fostering mentorship, and creating pathways for emerging talent to thrive.

– As captive insurance has historically been a male-dominated field, the panel discussion, “Women in Leadership – Driving the Future of Captive Insurance”, brought together accomplished leaders to share personal experiences, practical insights, and forward-looking perspectives on the future of the industry.

– One of our favorite parts of the conference is the annual CICA Student Essay Contest! This initiative gives undergraduates the opportunity to establish a hypothetical captive for a specific case study, including selecting policy options, determining underwriting approaches, and developing pricing strategies.

Navigating Regulatory and Tax Complexities

Regulatory changes continue to be a significant concern for captive owners. With evolving geopolitical dynamics and shifting regulations, staying up to date is critical for ensuring compliance and mitigating risk. Some notable compliance-focused sessions included:

– The 101 session, “A Beginner’s Guide to Captive Insurance Tax Basics”, panelists explained how captives are generally taxed, why insurance status matters, and the difference between being taxed as an insurance company versus a traditional business.

– The presentation, “Taxing Times: Federal, State and Cross-border Tax Considerations for Your Current or New Captive”, brought together four tax experts to discuss compliance updates and outline practical guidelines for effective tax planning within the captive space.

– In the session, “IRS and Captives – Today and Tomorrow”, tax experts discussed a range of regulatory updates and how they may impact both smaller and larger captives.

As always, the CICA Annual Conference provided a valuable platform for networking, learning, and sharing ideas within the captive insurance community. It was a privilege to engage with so many passionate professionals dedicated to driving innovation and shaping the future of captives. As we look ahead, we remain committed to staying at the forefront of these evolving trends and delivering forward-thinking solutions to our clients. We look forward to continuing these conversations and seeing everyone next year.

In a recent article published by Captive Intelligence, our SVP, Prabal Lakhanpal, and Senior Consulting Actuary, Nick Frongillo, explain how severe claim frequency and severity in Medical Stop Loss is impacting employers and strategies to respond to deteriorating loss ratios and mounting claim costs. You can find the full article here.

We are excited to announce that our SVP, Prabal Lakhanpal, has been elected as the Captive Insurance Companies Association (CICA)’s chair. You can find Captive Intelligence’s full announcement here.

Our Senior Vice President, Prabal Lakhanpal, has been appointed to the Captive Insurance Companies Association (CICA)’s Board of Directors for 2026-2027. You can find captive.com’s full article here.

We’re excited to announce that our SVP, Prabal Lakhanpal, has been recognized as Risk & Insurance’s Captives Power Brokers of the year! You can his full winner’s profile here.