Our VP, TJ Scherer, was quoted in an article from Captive.com, titled “Property Captives Flourish Despite Softening Market”, he explained how the softening P&C market has allowed for more breathing room for employers; you can find the full article here.

Spring Consulting Group, an Alera Group Company, has been shortlisted in Captive Review’s 2025 US Awards in the following categories:

- Actuarial Firm

- Captive Broking Services

- Captive Consultant

- Captive Service Professional

- Emerging Talent

- Employee Benefits Specialist

You can access the full shortlist here.

Spring Consulting Group, An Alera Group Company was listed as a finalist in Business Insurance’s 2025 U.S. Insurance Award Finalists. You can find the full list of finalists here.

Every year, the Risk and Insurance Management Society (RIMS) hosts its annual RISKWORLD conference, bringing together thousands of risk professionals to collaborate, learn, and shape the future of the industry. Set against the vibrant backdrop of Chicago, RISKWORLD 2025 delivered a powerful mix of emerging insights, strategic innovation, and spirited connection.

1) The Rise of Artificial Intelligence (AI) and Emerging Tech

With the ever-changing landscape of leave and accommodation laws, staying compliant remains a top priority for employers. This year’s conference offered valuable insights into managing the intersection of federal and state regulations. Experts shared practical advice on how to avoid common mistakes and streamline compliance efforts across diverse workforces. Here are some noteworthy sessions:

- In “Artificial Intelligence: What Is It, How Do I Recognize It, and How Do I Manage Its Risk?” speakers broke down AI fundamentals and explored strategies to manage model risk.

- The session “How AI Is Elevating Care Within Claims” highlighted practical use cases in automating claims workflows and improving outcomes.

- In “The New Cyber Battlefield: How AI Is Transforming Digital Attacks and Defenses,” experts demonstrated how AI is changing both the threat landscape and defense strategies.

2) Strategic Risk Management and Resilience Planning

This year reinforced that risk managers are no longer back-office advisors — they’re strategic partners at the leadership table. Many sessions emphasized using ERM and advanced analytics to drive proactive decision-making and build enterprise-wide resilience. Some hot-button presentations included:

- “Earn a Seat at the Table: Making Sure Risk Management Is Included in Strategic Decision-Making” laid out tactics to elevate the risk function’s role in C-suite conversations.

- “Unleashing the Power of Risk Culture: A Catalyst for ERM Success” explored how fostering a strong internal risk culture can fuel more resilient programs.

- “What Next? Leveraging Risk as an Input for Leadership Decisions” encouraged organizations to use risk data as a leadership tool — not just for compliance.

3) Innovations in Leave and Accommodation Management

With regulatory pressure mounting and the climate crisis accelerating, environmental risk and ESG transparency were center stage this year. Organizations are expected not just to comply, but to lead. Some sessions I found notable include:

- “Adapting Organizations to a Changing Climate: How to Achieve Business Resilience and Reporting Compliance” tackled strategies to meet climate goals while maintaining operational strength.

- In “The AI Impact on Climate Strategy and the World,” speakers discussed how data and technology are enabling more responsive environmental risk mitigation.

- “Viewpoints on ESG from the C-Suite to the Supreme Court” provided insights into navigating evolving ESG expectations at every organizational level.

4) Strategic Risk Management and Resilience Planning

Captives continue to stand out as a sophisticated solution for managing volatility, and their presence at RISKWORLD 2025 was stronger than ever — especially considering ongoing market hardening and cost pressure. I wanted to spotlight the following presentations:

- “From Safety Nets to Power Plays: How Captives Leverage Structured Reinsurance” outlined creative ways captives are being used to address volatility.

- “Beyond Traditional Coverage Boundaries: The Hidden Potential for Captives in an Evolving Risk Landscape” looked at how captives are expanding into non-traditional lines.

- “Captive Insurance: Better Solutions for Tomorrow’s Risks” focused on captive structures that support long-term resilience in a hardening market.

As always, RISKWORLD was more than just sessions and seminars, it was about connection, collaboration, and community. From insightful panels to spirited networking, this year’s conference underscored the expanding role of risk professionals in building organizational strength and foresight. The Spring team enjoyed every moment and is excited to see what next year’s conference has in store for us. We’ll see you at RISKWORLD 2026!

We are excited to announce that our Consultant, Aviel Shalev was named in Captive Review’s 2025 Ones to Watch. You can find the full list here.

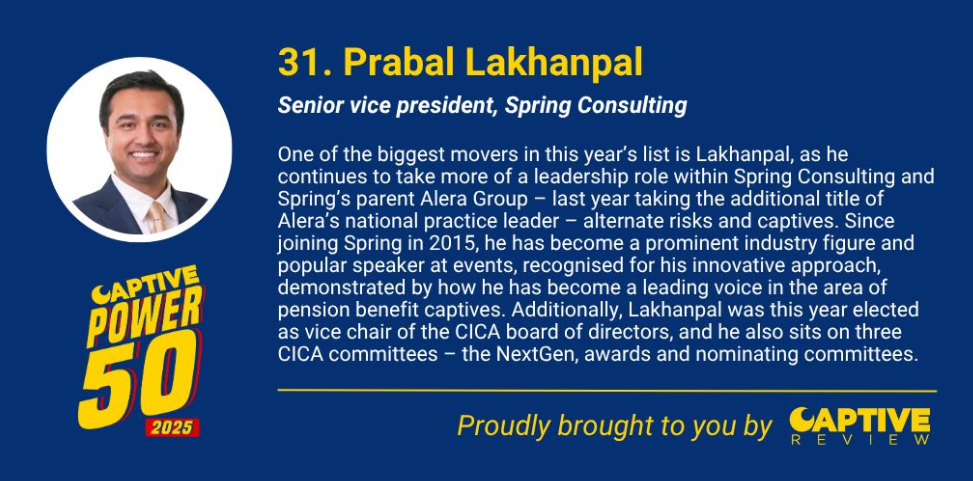

We would like to congratulate all CICA leaders who were recognized in Captive Review’s Power 50, including our SVP, Prabal Lakhanpal. The list spotlights top figures in the captives space, you can read more here.

Every year, Captive Review releases their Power 50 list, which spotlights top professionals in the world of captive insurance. This year our SVP, Prabal Lakhanpal was featured on the list at #31. Check out the full article here.

Medical stop-loss coverage protects organizations that self-insure their health plans from catastrophic medical and prescription drug claims. It has long been a valuable tool for small- and medium-sized employers seeking to limit their financial exposure to unexpected, high-cost claims. However, as healthcare and insurance dynamics shift, even large employers are increasingly turning to stop-loss coverage, particularly through captive insurance models.

1. Hardening Markets and Rising Premiums

Insurance markets have been hardening, with factors such as the lingering effects of the COVID-19 pandemic, economic uncertainty, and climate-related disasters (e.g., California wildfires, Hurricane Milton, etc) driving up premiums. Providers face higher operational costs due to regulatory changes and rising healthcare utilization, pushing insurers to reassess risks and raise prices. For self-insured employers, these market shifts result in increased reinsurance costs and reduced flexibility.

Captive medical stop-loss programs offer protection from these rising premiums by allowing employers to control claims funding and reserves. Captives offer a more customized solution compared to traditional insurers, enabling companies to mitigate costs while maintaining financial stability.

2. Volatile Claims and High Costs

Healthcare claims have become more unpredictable, especially with the rise of costly specialty treatments such as gene therapies and cancer drugs. This unpredictability can make it difficult for employers to forecast healthcare costs. A well-structured medical stop-loss program smooths out this volatility, helping employers manage cash flow by transferring risk to a captive. This approach allows for more predictable healthcare spending, similar to a fixed-premium model, despite the fluctuating nature of claims.

3. Rising Healthcare Costs

Healthcare costs continue to rise sharply, projected to increase by 8% annually due to higher care utilization and rising specialty medication costs. Traditional cost-shifting methods like high-deductible plans are no longer sufficient. Medical stop-loss coverage through captives offers a long-term solution by allowing employers to establish formal reserves and fund future high-cost years. This enables them to take a proactive approach to managing healthcare costs while improving benefits offerings.

4. Enhanced Control and Transparency

Captive stop-loss programs give employers more control over plan design and claims management. With greater access to data, employers can make informed decisions about cost drivers and health management initiatives. They can also secure better rebates on pharmacy benefits, reducing overall spending. Employers using captives as a purchasing platform to carve out pharmacy benefits, see overall Rx spend decrease, often saving 15-30% on net pharmacy claims. Captives provide the flexibility to tailor coverage to an employer’s unique needs, aligning with broader financial and risk management strategies.

A Multi-Layered Protection Strategy

In a volatile healthcare environment, captive medical stop-loss coverage offers employers a customizable, multi-layered approach to risk management. It enables organizations to not only manage current challenges but also shape a sustainable future for their healthcare benefits.

Our SVP, Prabal Lakhanpal was quoted in an article from Insurance Business on the rise of popularity in captive solutions and how it is shifting market roles. You can find the full article here.