Obesity is not a choice or a moral failing. It is a chronic, multifactorial disease with metabolic, behavioral, psychological, and environmental underpinnings. As employers, benefits managers, and health plan stewards, you must ask: Do you have all the pieces you need to manage obesity effectively? Offering a single tool will rarely suffice.

What Is a Weight Management & Metabolic Health Program?

A weight management and metabolic health program is a coordinated intervention set designed to address obesity and its underlying metabolic irregularities over time. These programs typically combine:

- Clinical evaluation of metabolic markers (for example, insulin resistance, lipid profiles, inflammation) ¹

- Nutritional counseling customized to metabolic needs

- Frequent and ongoing monitoring, follow-up, and adjustment

- Behavior change support, including coaching and psychological or mental health resources

- Physical activity and exercise guidance to preserve muscle and improve metabolism

- Medication support when clinically appropriate (including GLP-1 or including obesity GLP-1 agonists and other weight loss agents) ³

A high-performing program does not treat obesity simply as excess weight. Instead, it views obesity as a chronic disease that requires continuous management and adaptation.

Direct Primary Care

Obesity affects more than 40 percent of U.S. adults and is a major contributor to type 2 diabetes, cardiovascular disease, nonalcoholic fatty liver disease, certain cancers, osteoarthritis, and sleep apnea¹. Recognizing obesity as a disease rather than a behavioral failure shifts the paradigm. It demands a coordinated multi-pronged strategy, not a simplistic “eat less, move more” approach.

The causes of obesity are complex. Genetic predisposition, hormonal dysregulation, gut microbiota, psychosocial stressors, sleep disruption, food environment, and socioeconomic factors all play roles². Because of this complexity, no single solution such as a pill or injection can resolve the disease in isolation.

GLP-1 medications such as semaglutide and tirzepatide have demonstrated promising results in clinical trials for weight loss and improvements in metabolic health markers3. However, real-world adoption, drug discontinuation, and weight regain remain significant challenges. One analysis found that more than 50 percent of patients using GLP-1s for weight management stopped treatment within 12 months³. After discontinuation, biological adaptations lead many to regain much of the lost weight within a year. These patterns underscore that GLP-1s are powerful but only one piece of a broader strategy.

The Cost and Employer Dilemma

Employers contemplating coverage for GLP-1s face a difficult tradeoff. On one hand, these medications are expensive and can significantly increase pharmacy spending. A recent survey indicated employers are rethinking their strategy and many employers covering these medications today are considering a change. High discontinuation rates and uncertain long-term value make ROI calculations complex.

On the other hand, effective obesity management and improved metabolic health can reduce downstream costs associated with diabetes, cardiovascular disease, joint issues, and productivity loss⁴. Employers must decide whether to cover GLP-1s, and if they do not, how else to invest in comprehensive wellness and chronic condition management programs.

Benefits to Patients and Providers

For Patients

- Improved metabolic outcomes, including better insulin sensitivity and blood pressure

- Sustainable weight loss when combined with behavioral interventions

- Reduced risk of obesity-related comorbidities

- Enhanced quality of life, mobility, and mental well-being

- Lower likelihood of requiring invasive procedures such as bariatric surgery

Programs that integrate behavioral and psychological support help patients address emotional eating, stress, and motivation, which are often critical to long-term success.

For Providers

- Structured care pathways for chronic obesity management

- Data and feedback loops that allow for continuous monitoring and early intervention

- Clearer alignment with evidence-based best practices

- More efficient coordination between primary care, nutritionists, and behavioral specialists

Providers participating in holistic programs are better positioned to support patients in achieving sustainable outcomes rather than focusing solely on short-term weight loss².

Key Questions for Your Point Solution

When evaluating or designing a weight management and metabolic health program, consider the following questions:

- Does the program address underlying metabolic dysfunction rather than just weight loss?

- Are healthy behaviors supported over time, not only during initial engagement?

- Is psychological or behavioral support part of the design?

- If medications such as GLP-1s are offered, are they integrated within a structured clinical framework?

- Does the program emphasize preservation of lean muscle mass through physical activity and nutrition?

- Is there flexibility to adapt the program as patient needs and results evolve?

- Do providers have sufficient training and resources to sustain engagement?

- Is there a clear cost-benefit analysis and a defined measurement strategy for ROI?

Takeaways & Recommendations

Effectively addressing obesity requires viewing it through the same lens as other chronic diseases, with a long-term management strategy rather than a quick fix. Employers, providers, and health plan leaders must recognize that no single intervention can succeed in isolation. A comprehensive weight management and metabolic health approach combines medical treatment, behavioral support, nutrition, and ongoing engagement. While GLP-1 therapies have shown promise, they are only one component of a multifaceted solution. Without lifestyle changes and behavioral health integration, the long-term success of these medications is limited. Employers evaluating whether to cover GLP-1s should consider both the financial implications and the broader care framework necessary for success. Those that do offer coverage can maximize outcomes by ensuring these medications are paired with coaching, nutritional counseling, and continued follow-up. For those unable to include them, investing in alternative wellness initiatives and chronic condition management programs can still demonstrate support for employee health. Ultimately, effective obesity management depends on aligning all available tools (clinical, behavioral, educational, and organizational) to create a system that promotes sustainable metabolic health over time⁵.

1FAIR Health. (2024). Obesity and GLP-1 Drugs: A FAIR Health White Paper. Retrieved from https://s3.amazonaws.com/media2.fairhealth.org/whitepaper/asset/Obesity%20and%20GLP-1%20Drugs%20-%20A%20FAIR%20Health%20White%20Paper.pdf

2McKinsey Health Institute. (2025). The Path Toward a Metabolic Health Revolution. Retrieved from https://www.mckinsey.com/mhi/our-insights/the-path-toward-a-metabolic-health-revolution

3American Journal of Clinical Nutrition. (2025). GLP-1 Clinical Trial Findings. Retrieved from https://ajcn.nutrition.org/article/S0002-9165%2825%2900240-0/fulltext

4Cigna/Evernorth. (2024). Employer Strategies for Sustainable GLP-1 Coverage. Retrieved from https://newsroom.cigna.com/employer-strategies-for-sustainable-glp1-coverage

5Luminare Health. (2025). GLP-1s and the Cost of Obesity. Retrieved from https://www.luminarehealth.com/site/media/Files/LH-3270-White-Paper_GLP-1s.pdf

Cell and Gene Therapy (CGT) represents a revolutionary approach to the treatment of rare and complex diseases. Cell therapy is the transfer of live cells, into a patient to lessen or cure a disease using cells from the patient or a donor. Cell therapy can be used to treat a variety of conditions, including cancer, autoimmune diseases, and neurological disorders1,4,5.

Gene therapy alters faulty genes or replaces them with healthy ones to correct genetic disorders at the molecular level. Unlike traditional treatments that often focus on managing symptoms, gene therapy targets the underlying cause of a disorder, offering a potential one-time curative intervention that could radically improve the quality of life for patients. With nearly all gene therapies designed to provide durable effects from a single administration, these cutting-edge therapies are considered transformative, particularly for rare and genetic diseases that have long lacked effective treatment options.

Currently, there are over 30 FDA-approved cell and gene therapy treatments5 in the United States, with more than 4,000 therapies at various stages of development. While prevalence and incidence rates are low today, experts predict the treatable population will increase 11.5 times over the next five years, reaching nearly 50,000 patients in the US alone1,5. This growth is driven not only by the increased pace of FDA approvals for more prevalent diseases but also by greater access to qualified providers and facilities.

Cell and gene therapies are closely related and often overlap. In some cases, both are used together to treat diseases. For example, cell-based gene therapy involves removing cells from a patient, modifying them using gene therapy, and then reintroducing the modified cells into the patient’s body. Treatments for Duchenne Muscular Dystrophy (DMD), certain cancers, and spinal fusion are just a few examples3,4.

How Cell and Gene Therapy Will Transform Healthcare in the Next Decade

Cell and gene therapy are poised to radically transform healthcare over the next decade by offering potential cures for currently untreatable diseases, such as genetic disorders, certain cancers, and neurological conditions. These therapies allow for more targeted and potentially life-changing treatments. The ability to address the root cause of diseases, rather than simply managing symptoms, could lead to a paradigm shift in medical treatment. Conditions like sickle cell anemia, cystic fibrosis, Parkinson’s disease, and even HIV may benefit from these breakthroughs. This shift could foster a focus on preventative and curative approaches, moving away from the current treatment protocols that primarily manage symptoms.

These therapies have already caused significant disruptions in the pharmaceutical industry, pushing beyond traditional methods of disease management to fundamentally curative approaches. In the short term, more than a dozen new therapies could gain approval in 2024, including treatments for multiple myeloma and leukemia. In 2025, new treatments for hemophilia A and cutaneous melanoma could be approved. By 2026, there is potential for gene therapies targeting wet age-related macular degeneration and knee osteoarthritis, a condition affecting millions1.

- Advancements in Cancer Therapy2,3,4: CAR-T cell therapy uses a patient’s immune cells to specifically target and attack cancer cells, creating a personalized approach that could be more effective.

- Regenerative Medicine2,3,4: Stem cell therapies are being explored to regenerate damaged tissues and organs, offering potential treatment options for conditions like heart disease, diabetes, and neurodegenerative diseases.

- Personalized Medicine2,3,4: Cell and gene therapy may result in highly customized treatments tailored to an individual’s specific genetic makeup.

- Improved Treatment Outcomes2,3,4: Patients may no longer need to manage symptoms of chronic diseases, but rather address the underlying genetic causes, providing long-term and potentially curative solutions.

The Future of Treating Chronic Conditions

In the next decade, cell and gene therapies may expand beyond rare genetic conditions and cancers to include areas like cardiology and neurology, including high-profile diseases such as ALS and coronary artery disease. The prospect of next-generation viral-vector therapies for neurodegenerative conditions like Parkinson’s disease suggests the possibility of curing these lifelong diseases rather than simply managing them. Gene therapy could also disrupt transplantation by reducing, or even eliminating, the need for donor organs. Therapies could enable patients’ own cells to regenerate damaged tissues, bypassing immunosuppression or the need for transplantation entirely offering a groundbreaking alternative to transplants and potentially alleviating the donor shortage crisis.

Targeted Cell and Gene Therapy: In Vivo and Ex Vivo Approaches

Both in vivo and ex vivo therapies will play crucial roles in the future of cell and gene therapy. In vivo therapies involve directly administering a therapeutic agent into the patient, allowing for gene modification within the body to treat diseases affecting complex tissues and organs. This approach holds promise for treating conditions like heart disease and central nervous system disorders. In contrast, ex vivo therapies involve removing cells from a patient or donor, editing those cells in a controlled environment, and reintroducing them into the patient. This method has been particularly effective in CAR-T cell therapy for certain cancers, offering precise gene editing in a controlled setting.

As these techniques mature, they will expand into areas beyond oncology and hematology. For instance, 51% of current cell therapy pipelines are focused on CAR-T therapies, while other areas, such as RNA therapies and non-genetically modified cell therapies, are rapidly growing to address conditions ranging from pancreatic cancer to Duchenne Muscular Dystrophy1.

Systemic and Economic Challenges of Scaling Cell and Gene Therapy

Cell and gene therapies are inherently complex, and large-scale adoption requires healthcare systems to navigate both logistical and economic challenges. With over 4,000 therapies currently in development, 650 of which are in Phase II or beyond1, the healthcare ecosystem must adapt quickly to accommodate a surge of new treatments. Key factors include:

- Regulatory Adaptation and Oversight4: As therapies approach the market, regulatory bodies like the FDA’s Office of Tissues and Advanced Therapies (OTAT) will need to streamline and update guidelines to ensure safety and effectiveness. With over 100 therapies in Phase III trials, regulatory adaptations may be necessary to expedite approvals while balancing innovation with patient protection.

- Cost and Accessibility4: Cell and gene therapies are costly, with many treatments exceeding $1 million per patient. To manage the financial burden, outcome-based payment models, such as value-based pricing, subscription models, and risk-pooling arrangements, are being explored to make life-changing therapies accessible without straining employers and insurers financially. Employers may need to re-evaluate benefit plans to address these high-cost treatments.

- Healthcare Delivery Infrastructure2,4: Widespread adoption of cell and gene therapy will require specialized treatment centers and care delivery protocols. Advanced digital infrastructure will also be needed to support long-term patient monitoring, given the durability of gene therapies and the need for consistent data on success. Healthcare providers will need to educate and train professionals across specialties to provide appropriate follow-up and supportive care.

What’s Next for Cell and Gene Therapy?

The cell and gene therapy pipeline is robust, with 348 therapies expected to come to market within the next 3-5 years1. This includes new therapies for neurology and cardiology, areas where gene therapy has historically been less prevalent. As gene and cell therapies diversify into new specialties, they offer new avenues for treating complex diseases that have previously had limited therapeutic options. For example, in oncology, therapies are being developed for hard-to-treat cancers such as pancreatic, liver, and head and neck cancer. In neurology, therapies for conditions like ALS and Huntington’s disease are progressing through clinical trials and could open the door to targeted, long-term treatments for these debilitating diseases.

Moving from Treatment to Cure

Over the next decade, as gene therapies evolve from symptomatic treatments to curative solutions, the approach to chronic and genetic diseases may be forever altered. From reducing the need for transplantation to curing neurodegenerative diseases with a single treatment, cell and gene therapy has the potential to fundamentally redefine healthcare and patient outcomes. By addressing diseases at their genetic roots, gene therapy may offer patients a future free from the limitations of chronic illness, providing transformative solutions, health, and hope for those affected by genetic and complex diseases. Additionally, while the upfront costs of gene therapy can be high, these treatments could ultimately reduce long-term healthcare expenses by minimizing the need for ongoing care and costly treatments for chronic conditions.

As this field advances, cell and gene therapy’s impact on healthcare will be profound, laying the groundwork for a future in which medicine is curative, not just therapeutic. The next 10 years hold the promise of remarkable change, and as cell and gene therapies move from research labs to patient bedsides, the healthcare industry and society at large will need to prepare for a world where “treatment” is redefined by the power of genetic science.

1 https://www.asgct.org/publications/landscape-report

2 https://icer.org/news-insights/press-releases/icer-publishes-final-evidence-report-on-gene-therapies-for-sickle-cell-disease/

3 https://www.mckinsey.com/industries/life-sciences/our-insights/how-could-gene-therapy-change-healthcare-in-the-next-ten-years

4 https://www.milliman.com/-/media/milliman/pdfs/articles/managing_risks_related_to_gene_and_cell_therapies_for_self-insured_employers_with_stop-loss-coverage.ashx

5 https://www.fda.gov/vaccines-blood-biologics/cellular-gene-therapy-products

In August 2022, the Inflation Reduction Act (IRA, P.L. 117-169) was signed into law, bringing significant changes to Medicare. The law expands benefits, reduces drug costs, and improves the sustainability of the program, providing meaningful financial relief to millions of Medicare beneficiaries by enhancing access to affordable treatments1.

For the first time, Medicare now has the authority to directly negotiate the prices of certain high-cost, single-source drugs that lack generic or biosimilar competition. This groundbreaking provision is designed to help control costs and ease the financial burden on both the program and its participants.

Medications Selected for Price Negotiation

The Centers for Medicare & Medicaid Services (CMS) identified the initial group of drugs for negotiation based on multiple criteria, including the drug’s cost and the number of Medicare Part D enrollees currently using them. CMS engaged in direct negotiations with drug manufacturers to secure lower prices for some of the most expensive brand-name medications.

This negotiation process includes CMS presenting a final offer to the manufacturer, which can either accept or reject the proposal. The outcome? CMS and participating manufacturers have finalized pricing agreements, with Maximum Fair Prices (MFP) for ten selected drugs set to take effect on January 1, 20261,4.

This initiative is part of a broader, multi-year effort. By February 2025, CMS will select up to 15 additional drugs covered under Medicare Part D for negotiation, with new prices projected to be implemented in 2027. Another 15 drugs will be chosen in 2028, and an additional 20 the following year, expanding the reach of negotiated price reductions as required by the IRA4.

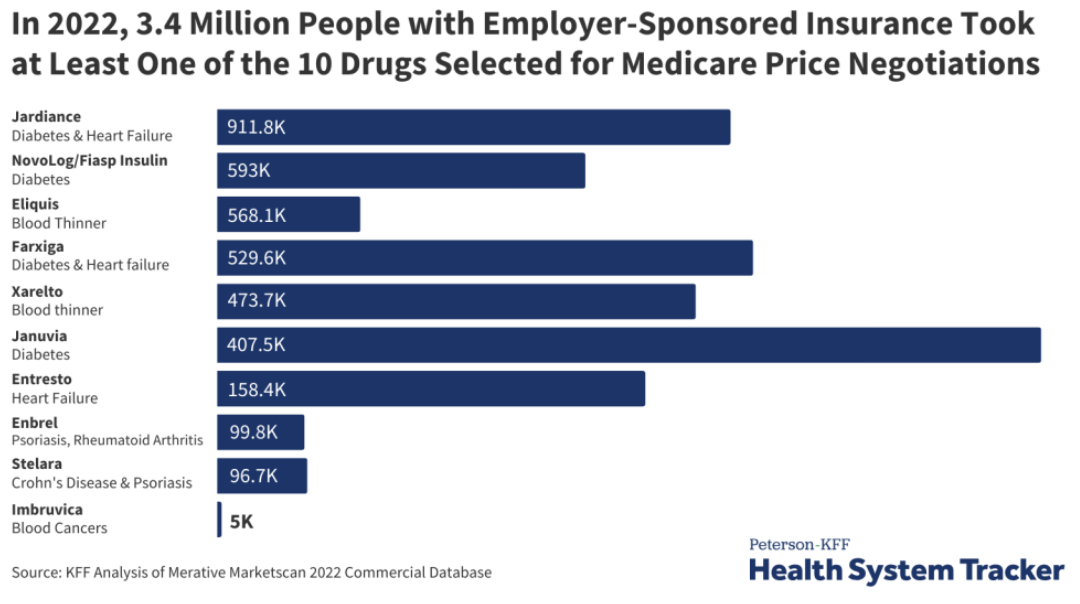

Although the Medicare drug price negotiations don’t apply to private insurance, 3.4 million people with employer coverage take at least one of the selected drugs. The ten medications are listed in the below graph3.

How Does This Affect Commercial Insurance?

Although these Medicare negotiations do not directly apply to private insurance, they could still have ripple effects on commercial drug pricing. Currently, 3.4 million people with employer-sponsored coverage use at least one of the drugs selected for negotiation3.

The impact on commercial insurance remains uncertain. Some experts suggest that lower Medicare prices could result in higher costs for private insurers as manufacturers look to recoup losses. Conversely, others believe that the negotiated Medicare prices could serve as a benchmark, potentially leading to lower prices in the private sector as well3.

While it’s too early to tell how private insurance will be affected, the ongoing Medicare drug price negotiations will be a closely watched development in the healthcare landscape.

To stay updated on this topic and learn more, click here.

1 Negotiating for lower drug prices works, saves billions. CMS. August 15, 2024. Accessed September 13, 2024. https://www.cms.gov/newsroom/press-releases/negotiating-lower-drug-prices-works-saves-billions

2 https://www.ajmc.com/view/lower-drug-prices-announced-under-medicare-negotiation-program

3 https://www.kff.org/medicare/issue-brief/explaining-the-prescription-drug-provisions-in-the-inflation-reduction-act/

4 https://www.cms.gov/inflation-reduction-act-and-medicare#:~:text=The%20Inflation%20Reduction%20Act%20makes,and%20limiting%20increases%20in%20prices

Unfortunately, news of rising healthcare costs seems less like news and more like the norm. In the last two years, we saw medical cost trend level out a bit, but it’s projected to spike back up. According to a recent survey by PwC’s Health Research Institute, the projected medical trend for 2024 is around 7% year over year, about the same as it was for 2021 and higher than both 2022 and 2023. Other sources predicted an even higher trend, coming in around the 8% – 9% range. Much of the cost burden falls on employees. The Kaiser Family Foundation reports that employees will pay an average of $6,575 for their health plan on a family basis, and around $1,400 for single coverage.

Cost Drivers

What’s behind the increase? There are a range of factors working behind the scenes here, most notably:

- Specialty drug and pharmacy costs. This is perhaps the biggest pain point when we think about overall healthcare costs, with specialty drugs or cell/gene therapy drugs seeing double-digit price increases year over year. The influx of demand for weight loss medications is a significant factor.

- Inflation. While the worst of inflation this go-around might have come and gone, inflationary impacts are typically delayed in the healthcare sector due to the lengths of contracts. This means that provider costs have risen, and that dynamic is playing out in the price of care.

- Healthcare worker shortage. The U.S. Bureau of Labor Statistics projects a need for 1.1 million new registered nurses across the U.S., and an Association of American Medical Colleges report projects a shortage of between 54,100 and 139,000 physicians by 2033.

- The worker shortage is further heightened by the next cost driver: increased utilization. As we finally stave off the extreme effects of COVID-19, healthcare consumers are back in a way they haven’t been since pre-pandemic. According to the International Foundation of Employee Benefit Plans (IFEBP), much of this uptick in utilization is due to chronic conditions.

- Catastrophic claims. IFEBP reports that catastrophic claims are responsible for nearly 20% of cost increases.

It is our job as health and welfare consultants to help employers navigate this landscape and identify solutions that can address the cost curve.

Combative Strategies

In such a difficult environment, it’s important to discern any tactics you can take to establish more control over your plans and create a sustainable program that works better for your organization and your employees. Here are a few of the strategies we typically evaluate on behalf of our clients:

- Alternative funding. By considering an alternative risk financing vehicle like captive insurance, employers can expect to save between 10% and 30% on costs in the long run. However, a range of self-insured models exist for organizations lacking the risk appetite for a single parent captive. This is a trend that has caught on. IFEBP reported that 79% of employers surveyed are self-insured. A captive or similar solution is even more powerful if paired with stop-loss insurance, which can protect against those catastrophic claims we mentioned above.

- Pharmacy benefits strategy evaluation. With the staggering prescription drug prices we are seeing, it is imperative that you ensure your Pharmacy Benefit Manager (PBM) is truly working on your behalf by considering a PBM audit, contract review, or market check. In addition, make sure that you have protocols in place for utilization control, like prior authorization. We also work with clients to improve plan design, utilize clinical programs geared toward population health goals, and dig into data to make informed decisions around possible solutions, whether they be formulary changes, point solutions, or something else.

- Wellbeing. Often overlooked as a buzzword, wellbeing programs can have an impact on your bottom line. To yield results, it’s important to be targeted toward workforce demographics, ensure you can measure success, and that employee engagement is maximized.

- Plan design. It may be time to reevaluate items like cost-sharing (high deductible health plans, copays, etc.), dependent eligibility, the inclusion of telemedicine and mental health, and more.

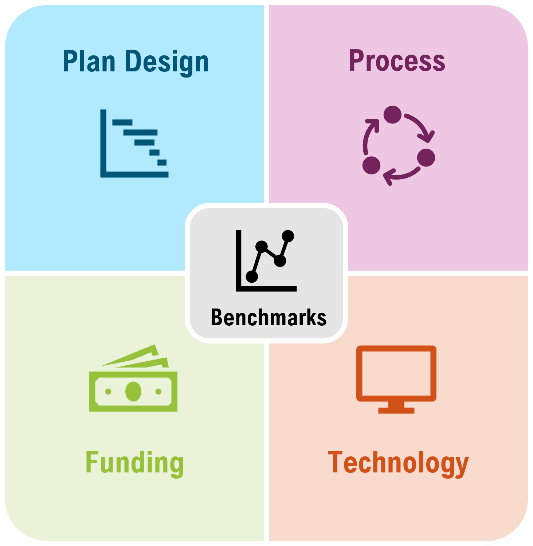

At Spring, we work across four main pillars: plan design, process, technology, and funding while leveraging benchmarks to look comprehensively across clients’ programs and identify areas for improvement. If you could use objective guidance on how your organization might be able to better manage rising healthcare costs, please get in touch.

Current State

Weight loss medications, Glucagon-like peptide-1 receptor agonists (GLP-1RA) s, have risen in popularity beyond anyone’s imagination and there is no sign 2024 will be any different. Endorsements by top Hollywood celebrities, aggressive and compelling consumer marketing, new direct-to-consumer options, and research demonstrating their benefits related to both heart and kidney disease, have left employers wondering if they should rethink their coverage choices.

Many employers have seen the impact on their budgets, adding on average $15,000 annually per patient in pharmacy costs. It is common for employers to focus only on short-term impacts and fail to connect the benefits of weight loss to long-term health care costs and goals. On average, patients who are overweight may incur healthcare costs that are 50% higher than someone of a healthy weight. Is it time we shift our thinking and focus more on the long-term? Is it possible that there is a subset of your population that would benefit from these medications? Would you reconsider your position if the right safeguards were in place?

The Bigger Picture

Did you know?1

- The National Institute of Diabetes and Digestive and Kidney Diseases, reports more than 42% of American adults are obese or severely obese, a rate that has almost doubled since 1980.

- Obesity is second only to smoking as a preventative cause of death in the United States.

- Every 5-point increase in BMI results in a 32% increase in risk of developing heart failure.

The American Medical Association (AMA), the World Health Organization (WHO) and other medical boards have recognized obesity as a chronic disease by for well over a decade. It is a complex metabolic condition that is impacted by genetics, behavior, and environment. Obese individuals have too much fatty tissue stored as energy within their bodies and their ability to change the body’s response to excess fatty tissue is often unsuccessful despite great efforts. 1 2 3

Obesity’s role in the development and/or progression of many chronic diseases, such as type 2 diabetes, hypertension, cardiovascular disease, kidney disease, stroke, sleep apnea, osteoarthritis, and certain types of cancer, is well documented. A person with obesity has an 80-85% risk of developing type 2 diabetes, and cancers associated with excess weight contribute to 40% of all cancers. It is easy to overlook that obesity not only impacts the physical body but also a person’s mental health.

The CDC reports that more than 50% of adults diagnosed with moderate to severe depression who were also taking an antidepressant were obese. Overall, 43% of adults with depression were obese compared with 33% of adults without depression, and women with depression were more likely than men to be obese. This was true across all age groups among women and was also seen in men aged 60 and older. 3 4

To Include or Exclude

As we enter 2024, the demand for weight loss medications continues and is anticipated to increase since much of 2023 was plagued with drug shortages. Despite these shortages, the average employer saw double digit increases in the GLP-1RA category which includes drugs for both diabetes and weight loss. Many employers continue to struggle, unable to justify unrestricted access and coverage for their members while striving to offer benefits that provide value and fair access.

As employers look for innovative ways to combat soaring healthcare costs, re-evaluating coverage of weight loss medications to a subset of members could be a critical piece of the puzzle. The International Foundation of Employee Benefit Plans (IFEBP) reports that 22% of employers in the U.S. currently cover prescription drugs for weight loss, and 32% offer weight management programs. Another survey showed up to 42% of employers were revisiting coverage for 2024 and beyond. 5 6 3

This year started off with somewhat of a curveball in this area, with Eli Lilly announcing LillyDirect, a direct-to-patient portal, allowing some patients to obtain its newly released drug, Zepbound (tirzepatide) for as little as $25 a month. LillyDirect uses the telehealth platform, FORM, where patients reach independent telehealth providers who can complement a patient’s current doctor or serve as an alternative care option. This news has been received with mixed emotions. Many obesity experts feel this is a long overdue service that improves access and addresses affordability concerns. Others feel this is another move by manufacturers to circumvent health plan sponsors and improve their market share. Many are calling for transparency between telehealth providers and the pharmaceutical company to rule out any conflicts of interest. 7

If you are exploring adding weight-loss drug coverage to your plan, a critical first step is to ensure members are educated about these drugs, essentially demystifying the media hype. The truth is these drugs are expensive, have side effects, and cannot do the job alone. Inadequate education regarding the side effects and how to manage them has caused many people to stop therapy, resulting in wasted healthcare dollars. The medications must be part of a comprehensive program that highlights the importance of healthy food and physical exercise. Members need to understand their responsibilities and how they will be held accountable for demonstrating their continued commitment to the plan. It has been demonstrated that those who stop the drugs regain, minimally, 75% of the weight because long-term behavioral changes and/or healthy eating habits did not form. 8 2 9 10 3

Employers also need to find ways to monitor their financial interests, such as:

- They must be active participants in designing coverage criteria and ongoing monitoring parameters.

- They must ensure they create a comprehensive approach, complete with a robust clinical review and ongoing monitoring at frequent intervals to evaluate a member’s response to therapy. As part of that, employers need to recognize the importance and impact that social determinants of health and health equity have when discussing weight.

- Determine ways to implement opportunities for members to access healthy food choices and physical activity and add additional wellness incentives to your benefit offerings.

- Be sensitive to the views/ or needs of your employees; do not make the out-of-pocket expenses so significant that they essentially restrict access.

- Finally, monitor your financials closely, request frequent in-depth reporting, and hold your PBM accountable for ensuring appropriate coverage/monitoring, access to competitive pricing, rebate incentives and formulary placement.

Conclusion

Ultimately the choice to cover these medications is an organizational decision, but it’s critical to have all the information necessary to make this decision, starting with a robust view of your population demographics. With high rates of obesity for most health plan sponsors, a prudent and thoughtful approach to expanding weight-loss coverage will be required. Attempts like this to tackle the obesity epidemic could produce long-term savings with lower overall healthcare costs, prevention of progression of existing diseases, and, most importantly, a better quality of life and employee experience. It has also been demonstrated that many people would remain at a job solely to retain coverage if offered and approximately 44% of people surveyed reported that coverage of these medications could be an important decision point in whether to accept a new position. 11 4 12 13 14 6 8

No matter your decision on offerings, the more you can offer through communications and education will help your plan participants make informed decisions and understand their role in achieving and keeping weight off. To realize tangible results, all parties must be committed. If you could use guidance around weight loss drug strategy or would like a clinical pharmacist to assess your population and needs, please get in touch with the Spring Team team.

1 https://www.cdc.gov/obesity/data/adult.html

2 Obesity Statistics. The European Association for the Study of Obesity.

3 Public Health Considerations Regarding Obesity. StatPearls

4 https://www.hsph.harvard.edu/obesity-prevention-source/obesity-consequences/health-effects/

5 https://ir.accolade.com/news-releases/news-release-details/glp-1-coverage-employer-plans-could-nearly-double-2024

6 https://www.cdc.gov/nchs/products/databriefs/db167.htm

7 https://investor.lilly.com/news-releases/news-release-details/lilly-launches-end-end-digital-healthcare-experience-through

8 https://icer.org/news-insights/press-releases/icer-publishes-evidence-report-on-treatments-for-obesity-management/

9 https://www.webmd.com/diet/obesity/obesity-health-risks

10 https://www.npr.org/sections/health-shots/2023/01/30/1152039799/ozempic-wegovy-weight-loss-drugs

11 https://jamanetwork.com/journals/jama/fullarticle/2812936

12 https://www.ama-assn.org/press-center/press-releases/ama-urges-insurance-coverage-parity-emerging-obesity-treatment-options

13 https://www.milliman.com/en/insight/payer-strategies-glp-1-medications-weight-loss

14 https://www.niddk.nih.gov/

Spring has been recognized as one of the Top Employee Benefits Consulting firms in Massachusetts by Mployer Advisors, who focus on connecting employers with top-rated insurance advisors. We’d also like to congratulate our colleagues at Boston Benefit Partners, An Alera Group Company, for making the list as well! You can find the full update here.

Demand for new weight loss medications continues to rise and employers remain concerned about budget impacts if they decide to offer these costly medications as part of their benefit package. These medications, known as GLP-1 agonists have skyrocketed in popularity and are thought to be “miracle drugs” by many. The reality is that weight loss requires a multi-modal approach and not all people who use them will achieve significant weight loss. Studies have shown that once discontinued, patients gain an average two-thirds of the weight back1. The reality is there is no miracle cure, but these medications have helped to destigmatize obesity and make clear the benefits of taking a multi-faceted approach to sustain weight loss.

Employer Case Study

As is the case with many organizations, weight loss drug strategy was recently of particular interest to one of our clients, edHEALTH. The client was interested in the positive impacts yielded but was daunted by the complex dynamic of long-term cost versus benefit.

Spring assisted edHEALTH in assessing a best practice avenue for weight loss drugs, keeping in mind that spending on obesity-related conditions result in approximately a 12% increase in total healthcare costs2. Wegovy (semaglutide) has an average price of approximately $1,349 a month, or more than $15,000 annually. That is more than double what the Institute for Clinical and Economic Review (ICER)3, a private entity that provides an independent source of evidence review and creates cost-analysis reports, recommends, instead stating that Wegovy should be priced somewhere around $7,500–$9,800 per year to fall into the cost-effective threshold.

We worked with edHEALTH and its PBM partners to fully understand their weight loss medication utilization management and monitoring parameters. As a member consortium, edHEALTH is committed to providing their member institutions with the information needed to assist them in determining the best cost-management strategies. Therefore, a key part of our evaluation was to prioritize the education of staff and faculty on the protocols and side effects of these medications to potentially narrow the interest to those highly motivated groups. There is no one size fits all solution, but there are specific points of consideration and educational resources that can help organizations of any kind address this topic with stakeholders.

Additional recommendations included:

- Ensuring plan participants understand that treatment should extend beyond the medication

- A comprehensive approach is critical and ideally includes behavior-management coaching, nutrition support, an exercise plan, and accountability check-ins.

- Non-medication initiatives might include fitness reimbursements, nutrition programs like WW (formerly Weight Watchers), and/or employee walking challenges. Incentives should be woven into these programs.

- Reauthorization requirements with the PBM should be in place (approximately every 6 months) to confirm patients are receiving the expected positive response to therapy related to goals.

For example, edHEALTH hosts an annual walking challenge between member schools, with prizes and check-ins along the way. The healthy competition creates a simple yet effective way to get employees moving more than they might otherwise, and a tactic like this pairs nicely with an overarching weight loss strategy.

Considerations for Employers

Ultimately the choice to cover these medications is an organizational decision, but it’s critical to have all the information necessary to make this decision, starting with a robust view of your population demographics. With high rates of obesity for most health plan sponsors, a prudent and thoughtful approach to expanding weight-loss coverage will be required. Attempts like this to tackle the obesity epidemic could produce long-term savings with lower overall healthcare costs, prevention of progression of existing diseases, and most importantly a better quality of life and employee experience.

No matter your decision on offerings, the more you can offer through communications and education will help your plan participants make informed decisions and understand their role in achieving and keeping weight off. To realize tangible results, all parties must be committed.

Our clinical pharmacist and benefits consulting team is here to help you assess weight loss as a component of your benefits strategy, including not only weight loss drugs but also wellbeing initiatives and data analytics for monitoring success. Get in touch for assistance in navigating this nuanced and rapidly evolving area.

1 https://www.nbcnews.com/health/health-news/happens-stop-taking-wegovy-ozempic-many-people-regain-weight-rcna66282

2 https://www.hsph.harvard.edu/obesity-prevention-source/obesity-consequences/economic/

3 https://icer.org/news-insights/press-releases/icer-publishes-evidence-report-on-treatments-for-obesity-management/

As pharmacy and prescription drugs continue to drive healthcare costs for employers. Many are reevaluating their Pharmacy Benefit Manager (PBM) arrangement to ensure transparency, strategic alignment, and fair pricing. Click here to access our Q&A and generate your PBM Report Card.

A summary of our webinar with the Northeast HR Association (NEHRA)

When it comes to health and productivity programs, the past several years have been a time for Benefits and HR professionals to test out a range of initiatives in response to pandemic and post-pandemic challenges, priorities, and employee expectations. Now, however, the market is in a different place and it is time to assess the impact of recent program offerings; does the reward outweigh the risk?

The Big Picture

Today’s economy is creating urgency around making sure benefits programs are properly managed. High inflation rates touch everything; the impact doesn’t stop at the grocery store or the gas pump, it extends to already high healthcare costs. In addition to the economic reality, we have seen an increase in healthcare utilization coming from new treatments and technologies available, further increasing costs. Relatively low unemployment may have shifted attraction and retention goals for some organizations, but a rise in layoffs is having tangible effects on the labor market at large which trickles down to employer strategies. It’s not just employers facing challenges, though, as healthcare services have become unaffordable for many and consumers/employees are also feeling the cost burden.

As a starting point, take a look at your data to answer questions like:

- What does your population look like in terms of demographics and health trends?

- What are your employees selecting for benefits?

- What is driving your costs?

- How might you segment your population?

- Are you accounting for future population shifts and resulting needs (e.g., company growth)?

You should then be able to assess whether or not your benefits align with your population as well as your corporate objectives. When determining true return on investment (ROI), it’s important to consider both human and financial perspectives.

Now that we have established a bird’s eye view of the risk versus reward equation, let’s drill down into key plan components that factor in.

1. Risk Management

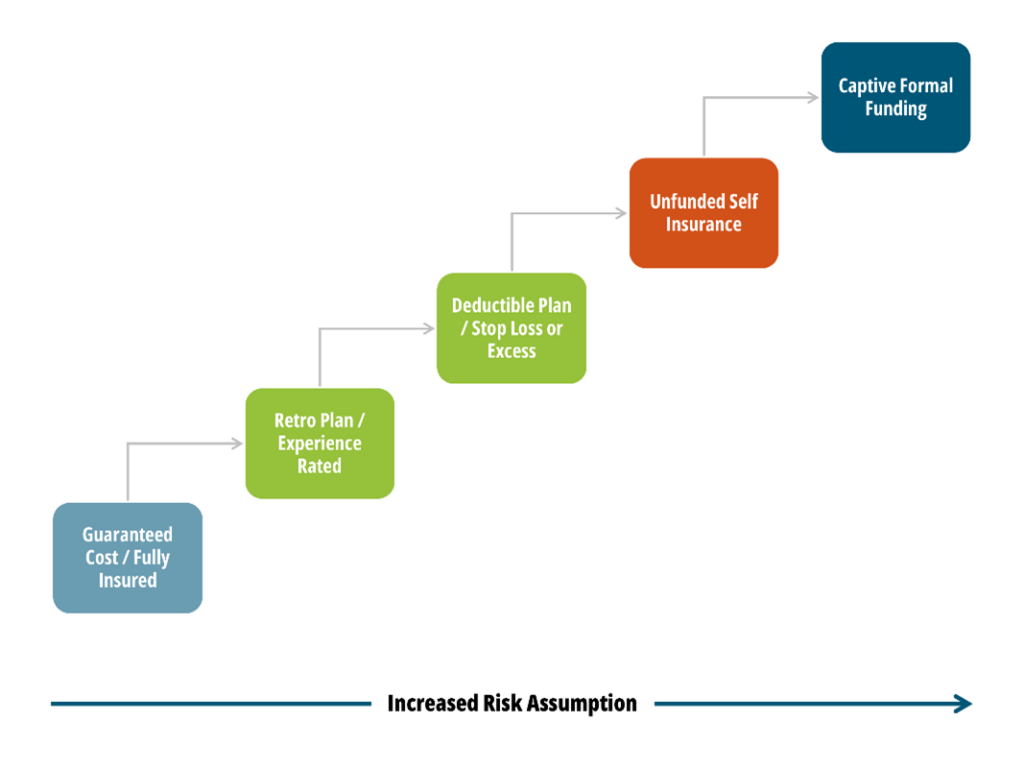

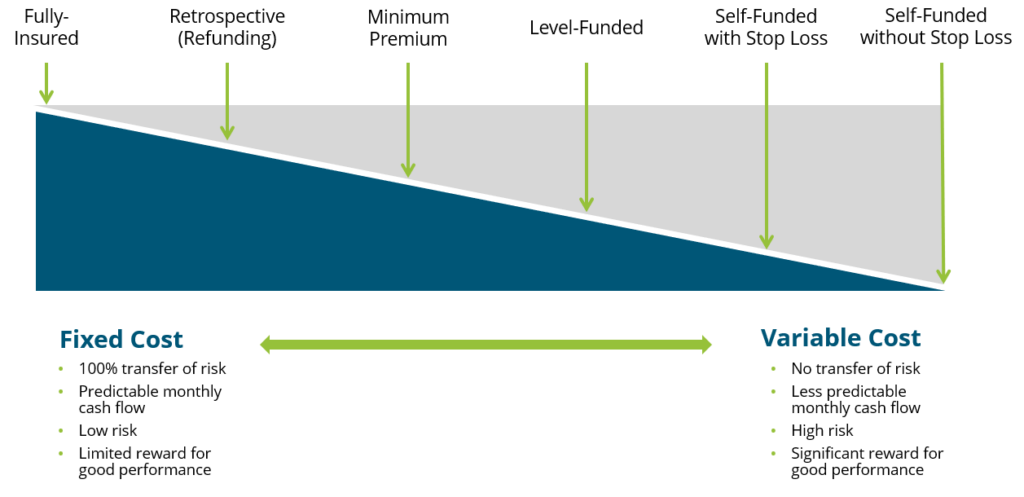

There are a range of risks to consider within your benefits strategy. There is the risk of buying insurance, and the allocation of funds. There is the risk to your employees of undertaking a high cost treatment, if necessary, which may not be feasible for lower wage workers.

When it comes to benefits funding, the following graphic illustrates the spectrum of options available, where the risk taken by the employer increases as you move toward the right.

While a fully insured plan largely frees the organization of risk, there is typically a lot of overhead and administrative costs involved and less governance when it comes to claims management. Overall, though, we encourage our clients to consider this spectrum and determine where they fit in related to risk appetite, budget and resources, specific health trend, and more.

2. Financial Management

Related but separate from risk management comes the financial management of your benefits program(s). There are three key activities that fall within this bucket:

- Program Strategy

- Account for long-term costs and variability

- Cost Projections and Rate Setting

- Provide budget updates

- Adjust for economic changes

- Includes premium equivalent rate projections and employee contribution rate setting

- Plan Governance

- Establish framework

- Ensure sufficient reporting and monitoring cadence

- Account for actual versus expected, large claims reporting, key cost drivers, retiree medical valuations, etc.

The insights gleaned from the financial management arm should be embedded into your overall benefits and risk management strategy, rather than live in a silo.

3. Pharmacy

Pharmacy has been top of mind for employers, understandably so given the rapid rise in prescription drug costs, which now constitute anywhere from 20-25% of total healthcare spend in the U.S. Specialty medications account for 50% or more of pharmacy spend even though only about 2% of the population is using them. Brand and generic drug costs are also rising at rates we have not seen in the past, perhaps in correlation with inflation. Suffice it to say, employers are struggling to mitigate their own costs as well as the costs for their employees. So, what can be done?

Within the pharmacy benefits landscape, two areas have been getting a lot of attention: weight loss drugs and biosimilars.

Weight Loss Drugs

Chances are you’ve heard about a new wave of “Hollywood diet” drugs. There has been an enormous amount of marketing going on around these new weight loss drugs, especially in the realm of social media and influencers. All of the buzz has also gotten the attention of employers, who are asking us questions surrounding coverage, costs, and pros and cons.

To provide some background, of the four weight loss drugs taking center stage, only two have indications for weight loss, while the other two are being used off-label. Weight loss drugs are not new, but these varieties are showing results we haven’t seen before, and their arrival on the market is timely, as about 42% of the population is either overweight or obese.

From a health and productivity standpoint, we know that obesity increases a person’s risk of developing a chronic condition, which leads to higher healthcare costs. But we also know that there are financial and non-financial reasons to foster a happy and healthy workforce. Can and should weight loss drugs be an answer for employers?

These new drugs are retailing for about $1,300 a month, so we need to consider annual costs and the longevity of how long an employee will need to stay on the medication. For employers considering them to their plan, we recommend it being one piece of a comprehensive strategy that also includes wellness initiatives and/or a commitment from those prescribed the drug. In addition, you must build strong monitoring protocols to judge effectiveness and impact on overall plan costs and utilization.

The inclusion of weight loss drug coverage in a health plan will make sense for some employer groups, and not others. We recently talked with an employer client who saw enough value in even a 10% reduction in body weight to convince them to cover the drug. However, any decisions need to be based, once again, off of population data and corporate objectives. This is a new and evolving sector, so your strategy should remain fluid as we see developments.

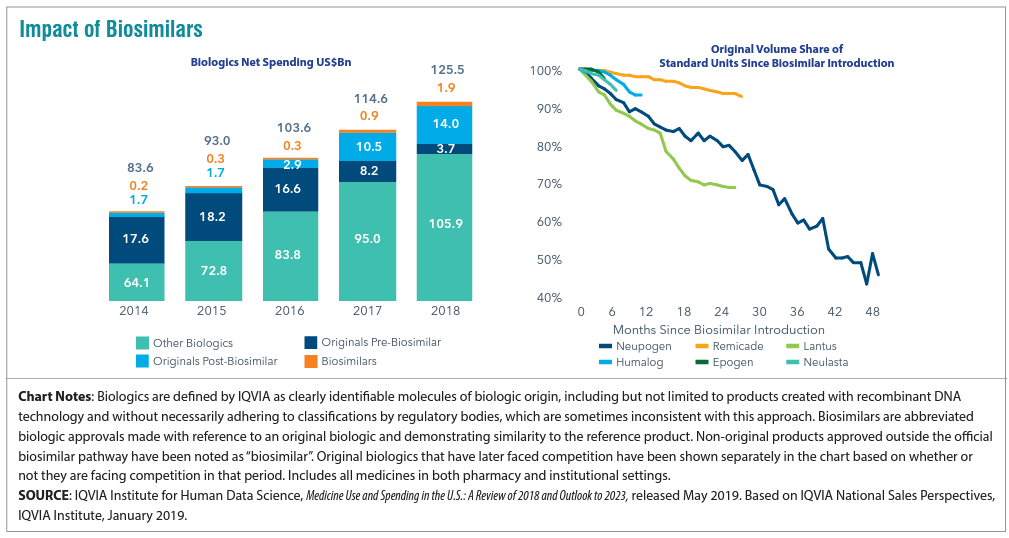

Biosimilars

Biosimilars are non-generic alternatives to those specialized medications that are very targeted in how they work and on what conditions they combat. There has been a lot of anticipation surrounding biosimilars as a solution to the specialty drug cost crisis. At the beginning of the year, a biosimilar of Humira, the number one drug dispensed in the U.S. which is used to treat inflammatory conditions, entered the market as the first biosimilar. While there has been some impact, to date it has not been the silver bullet we were hoping for. We can see below that biosimilar adoption rates are all over the map depending upon the condition for which it’s being utilized.

For employers, what’s important is vigilance in understanding where your Pharmacy Benefit manager (PBM) has positioned biosimilars as far as coverage is concerned. We have found that PBMs are placing biosimilars typically at the same parity with the reference, or brand name product. In this case both Humira and its biosimilar would be considered tier 3 medications, which does not yield the anticipated savings. Why is this? Well, there may be additional rebates available to employers and health plans if they continue to use the reference product.

This is a complicated space that continues to change at a rapid pace. Overall, though, if biosimilars are working the way we want them to, we need to figure out a way for all stakeholders to embrace them as a lower cost alternative instead of being locked into brand name drug prices. In some cases, the drugs are life-changing, so we do want to cover them but in a more sustainable way. We work with clients to ensure they are informed of and ready for these advancements and nuances.

4. Targeted Point Solutions

The term “point solutions” now represents a large umbrella of tools, however it typically references programs that target specific diagnoses such as diabetes, oncology, and hypertension. In recent years there has been significantly more interest in point solutions from our employer clients, and, especially with multiple solutions running at a time, these can be a slow leak on spend. Now is a good time to take a step back to answer that risk versus reward question for point solutions.

The best place to start in assessing point solutions whose reward outweighs the risk is data analytics. Try to use any data you are getting from your health plan, internal teams, or the industry to benchmark your spend. In areas where your spend is high relative to benchmarks, do a deep dive for potential solutions that can help. Some pitfalls in this area include:

- The more point solutions you implement, the harder they become to monitor and manage

- Point solutions embedded in your health plan may seem like a no-brainer, but they usually yield very low take-up rates

- Overlap between different point solutions/benefits programs can cause confusion for all stakeholders

- Focusing purely on dollar ROI may not be the play; listen to your gut about what is right for your workforce and understand the qualitative advantages around camaraderie and culture to be gained

5. Absence Management

Absence management is highly correlated with your health plan performance, since the vast majority of your high cost claims will also include a leave of absence, so there are both plan costs and productivity rates at play here.

Making absence programs more challenging is the volume of stakeholders involved and laws with which you need to comply (as seen below).

Further, when we talk about absence management, we account for a wide range of benefits including short- and long-term disability, statutory disability, workers’ compensation, FMLA, ADA state paid family and medical leave (PFML), and others.

With absence, different than with medical plans, your company’s managers and supervisors are directly involved when it comes to plan design, governance, staff training, etc., so it is an area where you typically need to look inward to drive change.

When it comes to the risk/reward balance of an absence management program, employers can make sure corporate programs are set up the way they want, for example, promoting the right attraction and retention strategy. Remember that the more generous your programs are, the more they will cost and the higher the risk you take on. If shifting some responsibility to an outsourced partner, be sure you still have monitoring protocols in place.

Closing Thoughts

Across these five areas and more, we encourage you to get familiar with your organization’s plan and demographic data. Depending on your size, the level and depth of data available might be different, but there is always some data available, such as industry standards and benchmarks. Whether you are focused on weight loss drug strategy, funding, or point solutions, you can take those data-driven insights and apply them across these four pillars to determine your best practice.

If you are having trouble getting started, or could use specific guidance surrounding the topics mentioned, please get in touch with our team.