As point solutions for health and benefits continue to pop up, it’s sometimes hard to understand what solution(s) might be most valuable for your workforce. Our “Point Solutions Spotlight” series is meant to hone in on one area of point solutions at a time, so you can make an informed decision. As January is Glaucoma Awareness Month, we thought this month we would spotlight a large potential risk factor for glaucoma: diabetes. A diabetes diagnosis doubles your risk for developing glaucoma1, among other vision impairments.

Executive Summary

Diabetes is one of the most common chronic health conditions in the US; in 2020 it was estimated that 34.2 million adults in the US were diagnosed with diabetes (roughly 11% of the population)2. This number is inflated even further when considering those who are undiagnosed or have prediabetes; in fact, the CDC believes one in three Americans will develop some form of diabetes in their lifetime3. Diabetes is caused by both genetic and lifestyle factors, some of which include weight, diet, and physical activity.

Employees diagnosed with diabetes often see their condition affect their work life, in the form of both productivity and absence, because some of the most common symptoms include urinating often, extreme fatigue and a constant feeling of thirst and hunger (even while eating). According to the American Diabetes Association (ADA) individuals diagnosed with diabetes spend on average $16,752 per year on medical expenses, $9,601 of which is attributed to diabetes (2.3 times more than spending by those without diabetes).

What is the impact on healthcare spending?

Diabetes is the most expensive chronic condition in the US, with an estimated $1 in every $4 of healthcare spending going towards diabetes-related care. Other top healthcare cost drivers include heart disease, cancer and musculoskeletal (MSK) conditions. In 2017, diabetes healthcare costs were $327 billion, with $237 billion accounting for medical costs and $90 billion in reduced productivity costs4.

According to the ADA, most diabetes medical spending goes towards:

- Hospital inpatient care (30% of the total medical cost)

- Prescription medications [including insulin] (30%)

- Anti-diabetic agents and diabetes supplies (15%)

- Physician office visits (13%)

The ADA also found diabetes leads to many indirect costs (often at the helm of employers):

- Increased absences ($3.3 billion)

- Reduced productivity while at work ($26.9 billion) for the employed population

- Reduced productivity for those not in the labor force ($2.3 billion)

- Inability to work because of disease-related disability ($37.5 billion)

- Lost productive capacity due to early mortality ($19.9 billion)

Our client, edHEALTH, is a consortium of 25 educational institutions that came together with the goal of reducing health and benefits costs for their employees while enhancing offerings at the same time. They consistently review the data, including diabetes, to find ways to help bring the costs down for their member-owner schools.

What solutions exist?

As diabetes has been the top chronic illness in the U.S. for some time, the distribution of costs for care (mostly towards inpatient care and prescription medications) have not changed drastically over time. As inflation continues to increase and many organizations are seeing healthcare costs rise, savvy employers are moving towards alternative models for addressing diabetes.

Employers who see a substantial impact of diabetes costs on their claims, may want to consider alternative treatment or lifestyle benefit offerings. Some of the top alternative solutions include:

- Diabetes Prevention Programs (DPPs)

- Diabetes management point solutions programs, some of which provide:

- Education of risks and potential treatments associated with diabetes

- Glucose testing/monitoring supplies and insulin pumps

- Apps that track blood sugar levels, weight, calories, and other metrics

- Digital platforms to connect employees directly with doctors

- One-to-one coaching

- Meal planning/nutrition goals

- Mental health resources

- Inpatient care coordination

- Health and wellness programs/initiatives

- Gym memberships

- Weight-loss programs

- Providing healthy food options (in the cafeteria, kitchen, vending machines, etc.)

- Mental health benefits

- Financial benefits

- To help control diabetes costs for employees

As an important note, employers may ask employees about health information following a job offer regarding diabetes, including how long said employee has had diabetes, if they need any work accommodations and if they need assistance during a low blood sugar episode. However, under The Americans with Disabilities Act (ADA), employers cannot discriminate against qualified individuals with diabetes. If your organization is seeing high diabetes healthcare costs, we suggest you revisit your healthcare plan(s) and/or adopt one or more of the alternative solutions above.

What should I do as an employer interested in a diabetes management program?

Employers must first understand the costs and trends associated with diabetes within their population/workforce. If diabetes is driving costs (medical, pharmacy and productivity), employers should consider alternative programs that align with their specific problem area(s). Identifying these patterns is key to understanding the need for tailored approaches such as preventative programs or introducing health and well-being benefits.

From there, market research will be necessary to understand pricing and select a vendor with the best program for your population. Spring’s consultants are here to help with market research, claims and data analysis, and/or a Request for Proposal (RFP) process so that you find a solution that best meets your organizational needs.

1https://www.smarteyecare.nyc/blog/the-link-between-diabetes-and-glaucoma

2https://www.singlecare.com/blog/news/diabetes-statistics/

3https://bit.ly/CDCchronicdisease

4https://diabetesjournals.org/care/article/41/5/917/36518/Economic-Costs-of-Diabetes-in-the-U-S-in-2017

When Congress passed the Consolidated Appropriations Act of 2021, this omnibus appropriations bill included the No Surprises Act (NSA). In 2022, much of the NSA focused on implementing consumer protections surrounding surprise medical bills after receiving emergency medical care. This was a big win for patients who were inadvertently receiving out-of-network care and billed non-negotiated rates in emergency situations where in-network providers and hospitals were leveraging out-of-network services and balance billing patients. The NSA specifically targeted air ambulance services and identified certain non-emergency services where notice and consent requirements must be satisfied for balance billing.

Two components of the NSA received much less fanfare and were not implemented on the original timeline. This includes: (1) requirements for providers to make good faith estimates (GFE) of charges for services within three hours (if immediate) or three days (if scheduled) and (2) the requirements around Advanced Explanation of Benefits (AEOB). The Department of Health and Human Services (HHS) delayed enforcement of these requirements for insured individuals, originally slated for plan years beginning on or after January 2022, given the lack of infrastructure for providers to transmit the necessary data on the GFE, which also directly impacted the ability to supply AEOBs.

The Centers for Medicare and Medicaid Services (CMS) and HHS asked for public comment related to the GFE and AEOB requirements. Comments were due November 15, 2022, and we expect clarifications or revisions to the regulations based on the feedback received. Implementation of the GFE and AEOB will demonstrate the fragmented health care structure that currently exists and that health plans, including self-insured plans, need to carefully monitor the impact.

GFE will impact every provider. Small, independent practices will likely experience the biggest disruption, which may translate into further consolidation. In addition, most services require coordination between multiple providers and ambiguity exists around ownership of those GFEs.

Although GFEs are a provider responsibility, health plans – including self-insured employer plans – are not immune to these pending guidelines. Compliant AEOBs must be supplied by health plans and one component is information related to the GFE. Therefore, information not only needs to be shared from providers to patients, but also from providers to health plans, so that it can be included in the AEOB.

In short, the No Surprises Act will likely be full of surprises in 2023 as CMS and HHS begin to address the following questions:

- How will data be exchanged (i.e., FHIR-based API or other means)?

- Is electronic notification sufficient, or will hard copy documents be required?

- How much time will be given for compliance (i.e., system updates, IT development, testing, printing, production, etc.)?

- Will any self-service options exist

As additional guidance is released and these questions are answered, we look forward to sharing our thoughts and recommendations in accordance. In the meantime, please reach out with questions related to the No Surprises Act, AEOB Compliance, or anything related.

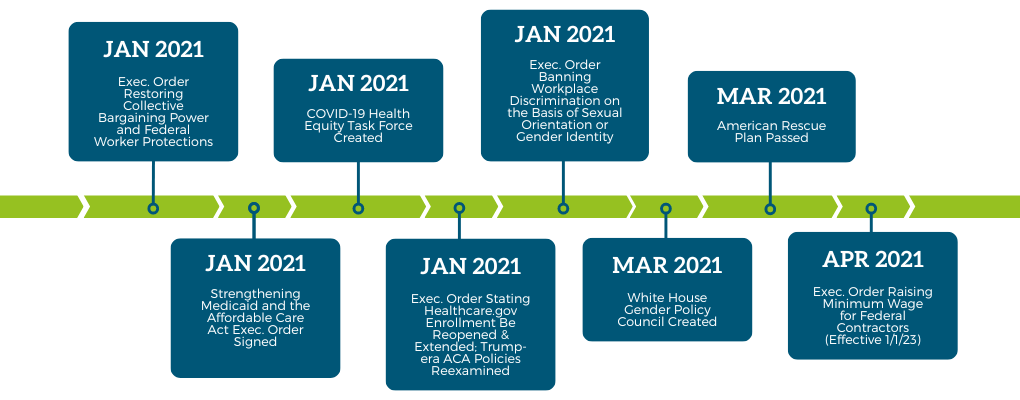

As we close in on the midway point of President Biden’s term, it is a good time to reflect on policy changes to date, as well as expected shifts in the near future related to employee benefits.

Ooh, We’re Halfway There: Key Changes From Biden’s Presidency So Far

With a focus on healthcare and employee benefits, here are some key Presidential activities that have occurred during the last two years (please note, this is not an exhaustive list).

Let’s dive a little deeper into some of these:

- The Strengthening Medicaid and the Affordable Care Act resulted in a special enrollment period for those impacted by the pandemic to allow additional opportunities for individuals to obtain health insurance.

- The American Rescue Plan was a COVID-19 stimulus package that included funding for:

- Vaccine distribution and testing

- Direct payments to eligible Americans

- Support for unemployment

- An expansion of the child tax credit

- Budget allocated toward schools and higher education for the purposes of reopening

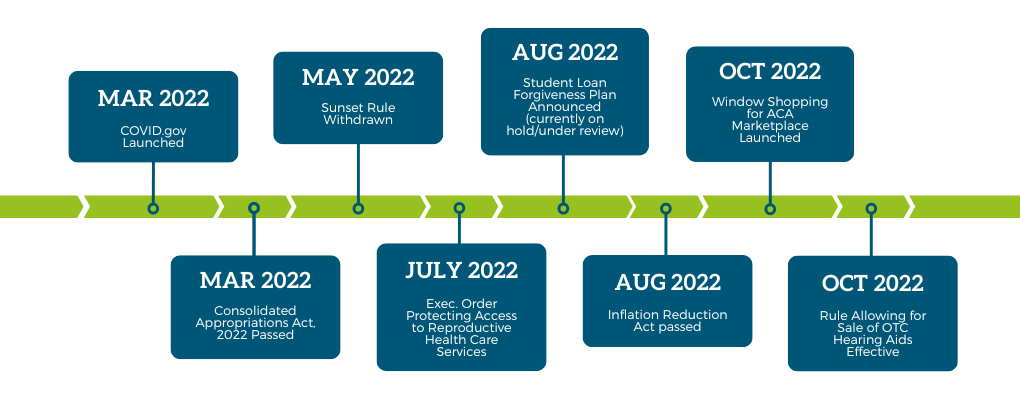

- The Consolidated Appropriations Act (CAA), 2022, has many provisions, among which include a safe harbor allowing high deductible health plans (HDHPs) to cover medical and behavioral health services before meeting the deductible. This safe harbor ended on December 31, 2022. Another component of the CAA 2022 is the Prescription Drug and Health Care Spending rule, which requires that health insurance carriers in group and individual markets report information on prescription drug and health care expenses to various federal governmental departments. This will be turned into a biannual report summarizing prescription drug price trends with the end goal of increased transparency.

- In response to the Supreme Court’s overruling of Roe vs. Wade, the Protecting Access to Reproductive Health Care Services executive order directed the Department of Health and Human Services (HHS) to expand access to medication, abortion, and emergency contraception, as well as to establish an interagency task force on reproductive health care access, among other provisions. However, laws around abortion still largely remain in the hands of state governments.

- The withdrawal of the Sunset Rule means that the HHS regulations will not automatically expire after ten years if not assessed based on the criteria in the Regulatory Flexibility Act of 1980.

- As a means to reduce the deficit, the Inflation Reduction Act is aimed at cutting healthcare costs, including prescription drugs, clean energy initiatives, and introducing a new tax on the wealthy.

- With the new ACA marketplace, consumers can preview their healthcare coverage options to understand what the costs will be and what savings might be available in advance of open enrollment.

Looking ahead, we can’t be sure what President Biden will prioritize during the second half of his term, but in the healthcare sphere we are likely to see a renewal of healthcare extenders, a debate around the topic of healthcare sector consolidation, substance abuse solutions, and strategies for managing the healthcare labor shortage. The COVID-19 Public Health Emergency (PHE) may or may not end in January 2023, which would impact Medicaid, as well as support programs and flexibilities offered, such as those related to telehealth.

A Split Congress

With a Republican-led House of Representatives and a majority Democratic Senate, we may be facing some standoffs at the federal level in the years to come. However, like Biden’s infrastructure law, there are some bipartisan issues that may see movement. Policies around paid leave, including sick leave, healthcare technology, and pharmacy costs may have enough support from both sides of the aisle to see progress.

Stateside

November’s midterm elections had many of us holding our breath, with several tight races in a divisive environment. The overturning of Roe vs. Wade meant many states had abortion-related questions on the ballot, with California, Michigan and Vermont passing measures that would protect abortion access and Kentucky failing to pass a law that would outright deny the right to an abortion. Health plans and employers alike have had to reassess their coverage related to these changes and consider new components, such as travel costs.

In other state election results, interesting activity was not in short supply. South Dakota approved a constitutional amendment that will extend Medicaid eligibility under the ACA to those with income below 138% of the federal poverty level., which is $26,500 for a household of four. This will take effect on July 1, 2023. Arizona passed an initiative that will limit interest rates to 3% for debt resulting from healthcare services, a cap that previously fell at 10%. Maryland voted to form a workgroup to advise on a subsidy program to support small businesses and is exploring a single-payer commission platform. Massachusetts also voted in favor of looking into a single-payer system and a public option, as well as a pilot program expanding eligibility for the Massachusetts health insurance subsidy program, and became the first state to regulate dental insurance. Meanwhile, newly elected Governor Lombardo of Nevada may be seeking to disrupt the 2021 bill calling for a public option for individual and small group markets.

At Spring, we take an objective stance on employee benefits and health plan design, always looking out for the best interests of our clients. Federal political stalemate aside, we do think changes in employee benefits will keep coming, and it’s best to be as proactive as possible. We will continue to keep you updated on changes in the employee benefits and healthcare spheres, if you have questions about recent legislature or need compliance guidance, please get in touch.

On National Pharmacist Day, our Assistant Vice President of Pharmacy, Jennifer Perlitch, a clinical pharmacist, is offering her view and surprising facts about the pharmacy industry today, as well as how she’s helping Spring’s clients combat the difficult climate.

The fact that pharmacy costs continue to skyrocket is not groundbreaking news. But what many people aren’t aware of is the “why” behind the increases. Several factors influence the price of a prescription drug such as the drug’s uniqueness and effectiveness and how much, if any, competition exists in the market. Unfortunately, there are times when drug prices increase significantly without important new clinical evidence. Regardless of why, as these prices continue to increase, it creates a significant burden on patients who need to pay deductibles or coinsurance.

So, what’s going on behind the scenes? Pharmacy is just one piece of the healthcare puzzle, and we know overall healthcare costs are also on the rise. There are five key reasons why healthcare costs are rising1:

- Aging population: The Baby Boomers, one of America’s largest adult generations, is approaching retirement age. As such, they are leveraging the system more, as seniors have the most need for prescription medication and other health services and are now or will soon stop contributing to the workforce.

- Chronic disease prevalence

- Rising drug prices

- Healthcare service costs, such as expensive procedures and physician salaries, are one component of the system that’s trending upwards

- Administrative costs, such as financial transactions and patient services, account for between 15%-25% of total healthcare expenditures2

When it comes to pharmacy specifically, there are two of these areas that I want to dive further into.

Chronic Disease Prevalence

Six out of every 10 adults in the United States have a chronic disease or condition, according to the Centers for Disease Control and Prevention (CDC). The most common chronic conditions in the U.S. include:

- Heart disease

- Stroke

- Cancer

- Diabetes

- Chronic kidney disease

- Chronic obstructive pulmonary disease (COPD)

Chronic conditions often require long-term medical attention and prescription drugs which often delay disease progression and improve or preserve quality of life. Some conditions may limit daily living activities, which could warrant use of home health care or other support services. The challenges of living with chronic illness also may increase the likelihood of suffering from anxiety, depression, and other mood disorders.

All these factors make caring for chronic disease patients more complex and resource intensive. There is a strong relationship between healthcare costs and chronic diseases in the United States. According to a report from the American Action Forum, the U.S. spends about $3.7 trillion each year for the treatment of chronic health conditions and the resulting loss of economic productivity.

In addition, the COVID-19 pandemic has caused some chronic disease patients to delay or avoid essential care. This means that chronic disease patients are spending less on healthcare services in the short term, but this will likely have damaging health and financial effects in the long term. When chronic disease patients delay care, they risk suffering from potentially life-threatening complications as a result. The long-term management of these complications will likely contribute to rising national health expenditures and consumer costs.

Rising Drug Prices

According to the Organization for Economic Cooperation and Development (OECD), the average American spent about $1,226 on prescription drugs in 2019 (the most recent year with internationally comparable data). This per capita cost is significantly higher than other developed countries. These costs will likely continue to increase, as the Centers for Medicare & Medicaid Services (CMS) estimates that prescription drug spending in the U.S. will grow by 6.1 percent each year through 2027.

The spending growth is due in part to a continuing emphasis on specialty medications and precision medicine. Specialty drugs are high-cost prescription medications used to treat complex conditions such as autoimmune diseases, chronic conditions, and cancers. Some therapies utilize genetic data to deliver a highly targeted, personalized treatment. The complex nature of these drugs makes them very costly to develop and distribute.

Drug pricing strategies also contribute to rising healthcare costs. Drug manufacturers establish a list price based on their product’s estimated value, and manufacturers can raise this list price as they see fit. In the U.S., there are few regulations to prevent manufacturers from inflating drug prices. There is no federal oversight; the federal government does not regulate drug pricing. It does however encourage the development of generic drugs through an abbreviated approval process to help improve access and affordability, but this often takes years.

Private Health Insurance and Out-of-Pocket Costs

Private health insurance spending growth accelerated slightly to 4.5 percent in 2018, from 4.2 percent in 2017. This trend is the net effect of faster spending growth in many services such as physician and clinical services and prescription drugs, which were only partly offset by slower projected growth in the net cost of private health insurance spending. In 2019, private health insurance spending growth slowed to 3.3 percent, which, in part, reflects the estimated impact of the effective repeal of the individual mandate within the Affordable Care Act (ACA). Over the latter period of the projection, 2020-27, private health insurance spending is projected to grow by 5.1 percent per year on average (or 1.8 percentage points more rapidly on average than in 2019) resulting mainly from the lagged response to higher projected income growth, especially in 2020-22.

Out-of-pocket (OOP) spending growth is projected to have grown faster at 3.6 percent in 2018, from 2.6 percent in 2017, due to faster income growth, as well as higher average deductibles for private health insurance enrollees with employer sponsored insurance. During 2020-27, out of pocket spending growth is projected to accelerate to an average annual rate of 5.0 percent, which is a similar rate as private health insurance during this period. During this timeframe, somewhat faster growth was projected for 2022, a year in which OOP spending was anticipated to grow 5.4 percent related to the excise tax on high-cost insurance plans3.

How can the Spring Consulting Team help?

As an employer you want the best for your employees and their families. Ensuring your pharmacy benefits meet their needs and supports their well-being is a critical component of your benefits package.

Evaluating your current pharmacy benefit offerings is an excellent place to start!

Here is an overview of our Pharmacy Benefits Consulting Services:

Evaluate current Pharmacy Benefit Management (PBM) Services

– Conduct annual/semi-annual reviews of PBM services, contract compliance, and performance guarantees and provide recommendations/assist in developing a plan to rectify any deficiencies.

– Perform follow-up activities as necessary to ensure contract compliance, efficient program management and responsive account management

– Review and evaluate utilization and any other key reports to assess trends/areas for opportunity

New PBM Implementation Services

– Facilitate implementation of the new PBM services including transition of benefit design, formulary, eligibility and pre-existing prior authorization approvals to new PBM

Pharmacy Benefit Consulting Services

– Review pharmacy benefit packages options and assist in selecting best option for your business needs

– Evaluate and recommend options for managing specialty pharmacy products

– Analyze the performance of the retail, mail order, and specialty pharmacy benefit option and make recommendations to improve the management of the drug cost trends

– Review and evaluate clinical and other optional programs and provide recommendations

– Meet with key stakeholders semi-annually (or quarterly) to review drug plan performance and identify recommended changes going forward.

Account Management Services

– Manage the ongoing relationship and communications with the PBM regarding specific eligibility and benefit updates

– Represent and advocate for business needs with the PBM when needed

– Participate in all PBM and client meetings related to pharmacy benefit and mail order services

Given the perfect storm outlined above, now is a great time to reassess all your benefits programs, but especially those related to pharmacy; please get in touch if you would like to optimize in this area.

1 https://www.definitivehc.com/blog/5-reasons-why-healthcare-costs-are-rising

2 https://jamanetwork.com/journals/jama/fullarticle/2785479

3 https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/Downloads/ForecastSummary.pdf

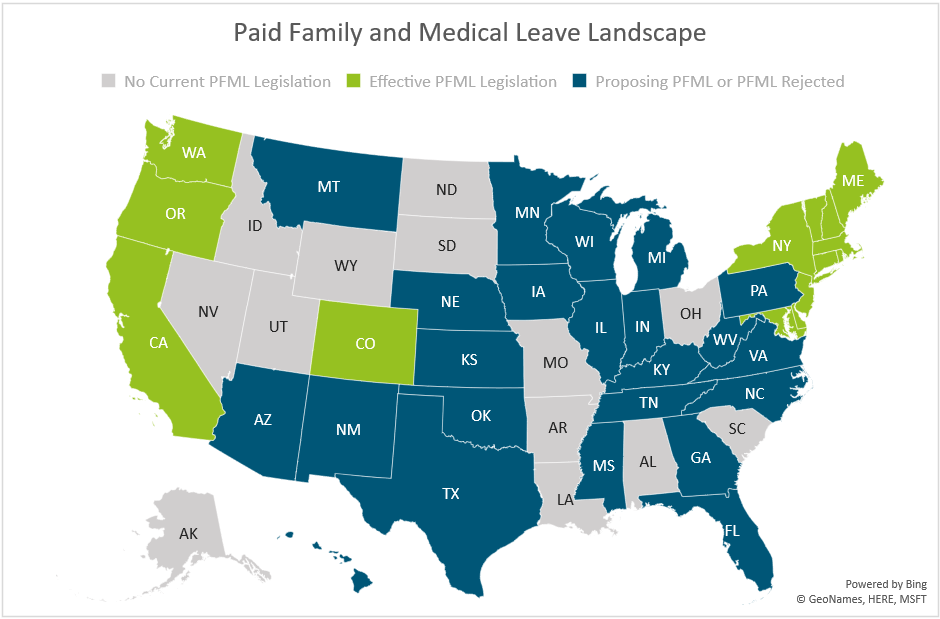

Paid Family and Medical Leave continues to be a confusing point for employers, compounded by new legislation being proposed at a seemingly constant pace. As leaders in the disability and absence management space, we are dedicated to staying on top of updates around PFML, among other areas. After a busy year in that regard, with another on the horizon, we wanted to share this brief overview.

In 2022, there was more movement towards state PFML laws being passed after decreased activity in previous years, largely due to the COVID-19 pandemic. For example:

- Delaware and Maryland both passed laws establishing PFML programs

- Virginia established insurance rules, allowing carriers in the state to provide insured PFML plans to clients

- Colorado and Oregon began collecting contributions on 1/1 and have been working to ensure they are prepared to do so, while establishing other rules for the effective administration of PFML

- New Hampshire worked to develop their voluntary PFML program selecting MetLife as its insurance partner and began coverage on 1/1/2023

- Vermont selected The Hartford as its insurance partner for its voluntary PFML program

- Maine made strides in developing the structure of their state mandated PFML program

In 2023, we expect continued activity. Pennsylvania and Michigan have outstanding proposals for PFML, which will likely be decided upon in 2023, one way or another. Additional states may also put forward proposals in upcoming legislative sessions.

In addition, and as seen in the updates below, states with existing legislation continue to make adjustments to their PFML programs. Adjustments to contributions and benefits are typically expected, most commonly, but not always, at the end of the calendar year.

The map below shows a summary of states with existing PFML legislation and programs in place, those who have proposed legislation without it being passed, and those that have not had any activity related to PFML in recent years.

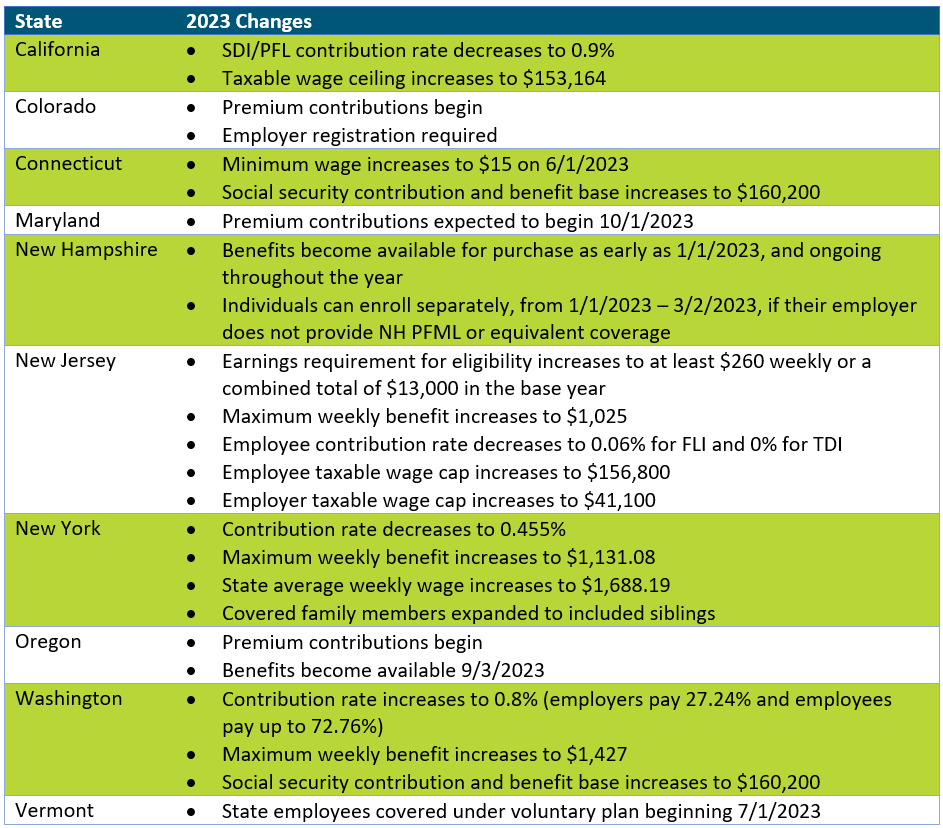

Massachusetts

In 2023, Massachusetts will be updating maximum benefit amounts and reducing total contributions.

The maximum weekly benefit is increasing to $1,129.82, effective 1/1/2023. This is an increase of about $45 from the 2022 weekly maximum. For any employees who may have leave that runs from 2022 into 2023, the weekly benefit that was determined when leave was approved will continue. The new maximum will not be applied until there is a new MA PFML leave application.

Contributions, however, will be reduced in 2023. The total contribution is decreasing from 0.68% to 0.63%, for employers with 25 or more covered individuals. The medical leave contribution will be 0.52%, with employers funding 0.312% and employees responsible for up to 0.208%. The family leave contribution will be 0.11%, with employers able to collect the total contribution from employees. Employers with less than 25 employees are not required to submit the employer portion of premium.

Other State Updates

Other states have made updates to their programs effective January 1, 2023, unless otherwise noted below. Some states may make changes off calendar year (e.g., District of Columbia, Rhode Island), which are not included if they have not yet been released.

Recommended Approach

Employers should review their PFML plans, policies, and processes to confirm they are in line with any legislative changes. To do so, the following checklist can be followed:

– Update employee notices and benefit documentation, as appropriate

While formal notices may not always be required, especially if contributions are decreasing, communicating updates to employees is recommended, especially if the change will impact their pay. Most states provide sample notices that can be customized to fit an employer’s needs. Keep in mind that there may be timing requirements in place (e.g., 30 days in advance).

– Confirm employee count to determine if any changes to contributions are required

Some states require contributions from both employers and employees however do not require employer contributions from “small” employers. This definition of small varies by state (e.g., less than 25, less than 50 employees). Confirming the total number of employees will verify the contributions being remitted to the state are accurate.

– Review private plan strategies based on previous year experience and changes to contributions

Whether or not a private plan is an ideal method for an employer to provide PFML to employees may vary from year to year. This can largely be based on the cost of a private plan versus going with the state plan, but the employee experience also plays a major role. From a cost perspective, a private plan, in most states, will be based on that employer’s leave experience. If an employer has high PFML incidence rates, insurance carriers or TPAs may charge more than is required to be paid under the state plan. From an employee experience perspective, having to file PFML claims to the state and what are often concurrent disability, FMLA or other leave claims to the employer or its vendor partner, can be confusing and require more effort for both employees and employers. While the driving factors will vary by employer, both cost and employee experience should be considered.

– Renew private plans as appropriate

When a private plan is in operation, states may require these be renewed at certain intervals. Massachusetts, for instance, requires this annually, while Connecticut only requires it every three years, unless a material change to the plan is made. Employers should review the timing of their private plan approval and guarantee it is up to date.

If you need assistance ensuring PFML compliance or assessing the optimal plan set up for your organization, Spring’s consultants are happy to help.

After a two-year hiatus, it was great being able to attend The Cayman Captive Forum in person this year. As the Cayman Islands is the second largest captive domicile, and the first for healthcare captives1; it is the perfect location to share leading trends in the captive world, and the warm temperatures and tropical views made it all the more enjoyable. If you weren’t able to attend or could use a refresher after returning to the “real world,” this quick recap might be of interest. Below are some of the buzziest topics at this year’s conference.

1) Tax Updates

On large attraction to captive insurance (and certain domiciles) relates to tax advantages. It’s complicated, though. Some of the tax-focused sessions presented at the conference were:

– Mike Domanski, a lawyer from Honigman LLP, discussed offshore federal tax considerations and U.S. tax reporting requirements in his session titled “Captive Insurance: Basic Tax Fundamentals.”

– In a session titled “The State of Tax: What You Need to Know,” experts discussed U.S. federal tax updates and how taxes will be affected by the Inflation Reduction Act and updates to Section 831(b).

– The penultimate presentation titled, “U.S. Tax Update” tackled IRS and compliance updates in the U.S. on both the federal and state levels.

2) Cyber Risks

Since the start of the pandemic, employers had to adjust to remote and hybrid workplace policies. This transition forced employers and employees to rely more on digital tools to conduct day-to-day operations and made organizations more susceptible to breaches. This is not the first year that cyber took the spotlight, but there were some great discussions around risk in this area, including:

– A session titled “Placing Cyber Liability in Your Captive” reviewed current trends in cyber treats and how insuring cyber in a captive can prevent devastating losses.

– Risk and Cybersecurity experts from the Cleveland Clinic explained why the healthcare industry commonly falls victim to cyber attacks and outlined steps to take to protect patient and caregiver privacy in their session, “Current & Future Cyber Risks In Healthcare: ‘Will you still love me, tomorrow?’”

3) Healthcare-Specific Coverages

In recent years, we have been seeing an increasing number of healthcare organizations leverage their captive to bring new and industry-specific lines. At this year’s Cayman Captive Forum we learned about how captives can be used for the following emerging and alternative risks:

a) Medical Malpractice/Medical Errors

As the Cayman Islands is the most popular captive domicile amongst healthcare organizations, there was a large focus on healthcare-specific risks. There was a particular emphasis on how healthcare employers can reduce and prepare for potential medical malpractice/errors as noted in the following sessions:

– Presenters from the “Criminalizing the Clinical Defendant: Straight from the Headlines” session facilitated a mock deposition to address common medical malpractice trends and how they should be addressed.

– A session titled “Can your Captive Eradicate the Impact of Covid on its Medical Malpractice Program? Will It Ever End?” reviewed how medical malpractice can impact claims and legal outcomes.

– Dr. Dan Shapiro Ph.D., explained his experiences with burnout in the healthcare industry and steps employers can take to support healthcare workers in his presentation “Labor Shortages, Employee Burnout & Medical Errors: Working Together to Improve Results.”

b) Workplace Safety & Patient Care

Workplace safety is another non-traditional captive line (outside of employee benefits and Property and Casualty [P&C]) gaining traction. Healthcare organizations and, more specifically, healthcare workers and patients are prone to violence and discrimination more so than staff in other industries.

– In the session “Workplace Violence in Healthcare,” Trinity Health’s Diane Moritz explained initiatives their captive board are taking to prevent workplace violence injuries and support victims of patient violence.

– Children’s National Hospital’s Chief Diversity Officer, Denice Cora-Bramble discussed biases in data reporting for diverse patients, and experiences minority patients face when seeking health services in the session, “DEI Impact on Quality and Safety of Care.”

– I was joined by lawyer, Michael Domanski in a pre-recorded session titled “Using a Captive to Fund Long-Term Care,” during which we reviewed the current LTC market and different captive models (both taxable and tax-exempt) that can cover long-term care policies.

As we transition into a new era of captive insurance, this year’s Cayman Captive Forum acted as a perfect vehicle for addressing current and future themes in the industry. It was a strong end (almost) to an exciting year and we look forward to next year’s conference to continue these and other important discussions. Our team was fortunate to be part of the action in the Cayman Islands this year and is here to answer any questions you may have related to an existing or new captive program. Check out our captive expertise here and let’s chat!

1 https://caymanintinsurance.ky/about/

As the Cayman Captive Forum starts just this week. We are proud to announce Spring and our consultants have been recognized for multiple awards from Captive International’s Cayman Awards 2022. We look forward to continuing to do excellent captive work in all domiciles, including but not limited to the Cayman Islands.

Spring has been awarded for:

Background

On election day, Massachusetts voters were asked to approve or reject four ballot questions when casting their votes for Governor and Attorney General. The 2nd ballot question focused on regulating Dental Insurance, which if passed would “require that a dental insurance carrier meet an annual aggregate medical loss ratio for its covered dental benefit plans of 83 percent1” In layman’s terms, this means dental insurers will have to spend at least 83% of premiums on patient care instead of administrative costs, salaries, profits, overhead, etc. The legislation mandates that if an insurance carrier does not meet that 83% minimum requirement, they will have to issue rebates to their customers. It further allows state regulators to veto unprecedented hikes in premiums and requires that carriers are more transparent with their spending allocation.

Prior to election day, Massachusetts did not have a fixed ratio when it came to dental insurance and will soon be the first state in the nation to have a fixed dental insurance ratio. Although MA requires reporting from dental plans, there were no regulations on premiums. The proposed law sets up a protocol similar to what the Affordable Care Act (ACA) requires of health insurers, where in Massachusetts health insurance carriers must spend at least 85%-88% of premiums on care.

Over 70% of voters voted in favor of regulating dental insurance, the most one-sided response of all four ballot questions. Although at face value regulating dental insurance may seem beneficial for patients, the impacts are not cut-and-dry, and the legislation may affect multiple parties, from consumers to carriers and dentists and practice owners.

Leading up to election day, general reactions about the legislation from dental insurance carriers were negative, while it was supported by most dental practitioners. In fact, the ballot initiative was brought to fruition, in large part, due to an Orthodontist in Somerville. As we can see from the polling results, the general population, or consumers/patients, were also in favor of question #2 passing.

Potential Impacts

For patients: On the intangible side for patients/consumers, the law would provide some peace of mind that the money they pay for their dental insurance was going, in large part, to their care. There is also an indirect advantage to increased transparency, mitigating the typical confusion that surrounds insurance plans and payments. More tangibly, the change could mean that insurers are willing to cover more procedures as a means to hit their minimum requirement (good), however that could result in dental practitioners charging more (not so good).

For employers: We anticipate that the new law will give employers who sponsor a dental insurance benefit plan more control over pricing and protection against unreasonable rate increases. Since many businesses do not offer a dental plan, or offer it on a voluntary basis, the effects should be relatively small. On the other hand, if the law were to create a change in the number of carriers in the marketplace, this could have an impact on plan and network options and negotiating power.

For dental practitioners: With the change, one perspective is that dental practitioners will be able to better focus on the best care for each patient. They may also see an increase in business and revenue if insurers are allocating more dollars towards care and procedures.

For dental insurance carriers: Dental insurers largely opposed question #2 for obvious reasons, such as restrictions on how much they can charge and additional requirements they need to adhere to, but also for less obvious reasons. For example, some carriers argue that the law will require them to make up for profit loss by raising premiums, warning that they could increase by as much as 38% in the state2. They have reason to believe this law will lead to less competition in the dental insurer marketplace, which typically does not benefit the consumer.

Conclusion

Having worked with Massachusetts employers of all sizes on their benefits, including but not limited to dental insurance, as well as interfacing with insurance carriers, being the broker representative for a large percentage of dental offices in the state and working with MDS, we are looking at this update from all angles. Our expertise and decades of experience in this industry enables us to make the following conjectures about passing of ballot question #2:

- Dental insurance premiums may rise, but at a minimal rate

- We ultimately believe this is a step in the right direction as an advocate both for our employer clients and their employees, and that transparency is a positive attribute largely missing from the healthcare experience today

- Immediate impacts will also be minimal, but we may see some of the other factors mentioned above play out over the next few years

If you have specific questions about how the new law might impact your dental plan(s) or practices, please get in touch. In the meantime, you might be interested in watching our recent webinar, “Why Long COVID Needs Short-Term Attention” as you develop your 2023 benefits strategies.

1https://www.sec.state.ma.us/ele/ele22/information-for-voters-22/quest_2.htm

2https://www.wbur.org/news/2022/10/18/massachusetts-ballot-question-2-explainer

It is estimated that ~44 million Americans are experiencing long COVID symptoms. During a recent Spring webinar, our SVP, Teri Weber was joined by a pulmonologist and a representative from Goodpath to review common long COVID symptoms and how it is impacting productivity and claims. You can access the webinar here.