Background

According to Pharmacy Times, between July 2021 and July 2022, more than 1,200 medications had a price increase that surpassed the inflation rate during that time of 8.5%, with the average increase across these drugs coming to a staggering 31.6%. Overall prescription drug spending is projected to rise at an average annual rate of 6.1% through 2027.

Why are we seeing this uptick? An aging population, healthcare services costs, and administrative costs (e.g., financial transactions and patient services) are likely partly to blame. There are a range of strategies and tactics to help combat rising pharmacy costs within your benefits program, but it is important to understand what is driving these costs both globally and specifically within your organization. There is much talk about the skyrocketing costs of specialty medications. Specialty medications are now responsible for over 50% of total pharmacy costs, yet only about 2% of the population is using them.1 Unfortunately, a significant portion of pharmacy spend is going towards innovative and/or targeted therapies that treat rare, complex, genetic or inherited diseases, and cancer – all of which are usually beyond our control.

Preventing the Preventable

On the other hand, however, there are several behaviors that have a strong influence on health outcomes: tobacco use, alcohol consumption, physical activity, and diet.6 A direct correlation between cigarette smoking and the risk of heart disease has been shown and it is in fact the single most important modifiable risk factor for heart disease. Cigarette smoking has also been linked to certain cancers, which is the second leading cause of death in the United States. In fact, 16 million Americans have at least one disease caused by smoking, costing over $240 billion in healthcare costs annually.1

Obesity has been linked to multiple chronic diseases including heart disease, diabetes, and musculoskeletal conditions impacting bone health. The Centers for Disease Control and Prevention (CDC) reports that obesity adds another $173 billion worth of burden on the healthcare system per year because of resulting complications. Several studies have documented the adverse cardiovascular health effects that plague overweight adults. This is partly because obesity adds increased demands on the heart to supply blood to the body. Excess body weight and obesity are linked with an increased risk of high blood pressure, diabetes, heart disease and stroke. Losing as little as 5 to 10 pounds can make a significant difference in your risks. Even if weight control has been a lifelong challenge, taking small steps today can go a long way.2

Diet and physical activity are behaviors that directly influence weight. However, they may also have direct effects on diseases.

- The brains of middle-aged adults may be aging prematurely if they have obesity or other factors linked to cardiovascular disease.

- Almost 25% of adults have metabolic syndrome, a set of factors that in combination significantly increase a person’s risk of heart disease, diabetes, stroke, and other illnesses. Research has shown that people who have two or more of these conditions have even higher risks of heart disease.

Wellness interventions provide an opportunity for us to have some control over the healthiness of our workforce. These interventions play an important role in moving the needle by working to solve for the root causes at play. Employers should be incentivized to implement these preventative programs not only because wellness programs are considered as “nice perks” that increase employee morale and productivity, but also and more importantly, they are tangible solutions that can reduce the burden of health and pharmacy costs. If less employees need prescription drugs in the first place, pharmacy spending could decrease dramatically. Seems easy, right?

Let’s Get Tangible: Wellness for Outcomes

The higher the risk factor prevalence within a population, the greater healthcare costs are likely to be, both within the pharmacy realm and overall. Therefore, wellness initiatives targeted towards combatting, reducing, or preventing these risk factors will have a more tangible impact on reducing costs and improving health outcomes.

A Targeted Approach

There are six key lifestyle behaviors that promote a long and heathy life3:

- Getting enough sleep

- Eating a healthy diet, full of fruits and vegetables, healthy fats, and reduced sodium

- Being physically active for at least 30 minutes a day

- Maintaining a healthy body weight

- Avoiding tobacco use and exposure

- Limiting alcohol consumption

The goal is to reduce the need for prescription medication by stopping problems before they even exist. In a study of 55,000 people, those who made healthy lifestyle choices such as avoiding smoking, eating healthy, and exercising lowered their heart disease risk by about 50%.4 In fact, unhealthy lifestyle behaviors such as those that oppose those listed above cause approximately 70-90% of chronic diseases, which yield up to 75% of total healthcare spend in the U.S.5 As such, when it comes to medical and pharmacy costs, the most successful wellness programs will be those aimed at those six pillars and affecting long-lasting behavioral changes.

Wellness Point Solutions

The good news is, the wellness industry awakened with this realization a decade or so ago, in the midst of out-of-control healthcare costs, and now there are a plethora of wellness companies and tools available for employers to leverage. In fact, in the U.S., the wellness industry represents $1.2 trillion in revenue6. Homing in on the six behaviors above, employers might consider the following*:

- Tools like Foodsmart and Noom are focused on forming healthy eating habits and ensuring a well-balanced diet.

- Pivot and Wellable are some of the tools available aimed at smoking cessation.

- Employers can take advantage of services like Vantage Fit and MoveSpring that help employees with fitness and movement goals.

- Drinkaware can assist employees in understanding and lessening alcohol consumption, while Virgin Pulse has a more overarching suite of wellbeing services.

- Mental health has been at the forefront of workplace wellness conversations for some time now, and tools like Headspace and Kona offer stress mitigation techniques and alert managers to burnout warning signs. A healthier mind leads to more and better sleep.

- Weight Watchers and incentaHEALTH are geared toward weight management.

A range of wellness point solutions are out there, and the all-encompassing ones will have tools pointed toward all six of our wellness pillars. Additionally, larger employers have started to introduce onsite health clinics and resources to make employee engagement in their health more convenient. Some incentivize through walking or step challenges. Health plans build in wellness incentives such as reimbursements for gym memberships. Whatever it looks like, introducing preventative measures that lessen the prevalence of disease and poor health outcomes; reduce the need for prescription drugs, lost work days, and absence from work; and improve mental health; can lessen overall healthcare costs and prove advantageous for your workforce.

Before you make any decisions around wellness solutions, be sure to understand what is driving your pharmacy spend within your own organization. We recommend working with a consultant or actuary to take an unbiased and robust view of your data. Better yet, consider taking the next step to…

Work With a Clinical Pharmacist

Even the best wellness programs cannot prevent or reverse existing and/or genetic health problems within a workforce population, and there are times when prescription medications are necessary. Typically, a clinical pharmacist is not part of your health benefits team, weighing in on strategy and dissecting the needs of your workforce population. I firmly believe this is both a gap and an opportunity.

An experienced clinical pharmacist can look at the full array of options available through a different lens, putting all the pieces together (medical, Rx, wellness, etc.) and provide targeted recommendations to improve outcomes while controlling costs.

Another important role of a clinical pharmacist is the ability to recognize signs of medication non-adherence, which can cause disease progression and adverse outcomes. If your organization is spending money on prescription drugs that are not being taken correctly and therefore cannot have the intended effect(s), a pharmacist can flag that up.

Get in Touch

When it comes to healthcare and pharmacy costs, many of the factors involved are out of our hands. However, we do have some power to affect change and take control through preventative, wellness, and innovative and targeted pharmacy solutions. Given the current climate, why wouldn’t we aim to do so?

If you need assistance assessing your current wellness programs, navigating the marketplace of vendor solutions, conducting a Request for Proposal (RFP), auditing your pharmacy benefits contract terms and utilization data, or are interested in leveraging a clinical pharmacist to yield customized and impactful results, our team would love to chat with you.

*Please note, Spring’s intent is neither to promote nor recommend any of these specific solutions, but rather to portray a snapshot of what is available in the market.

1https://www.wellsteps.com/blog/2020/01/02/benefits-of-wellness-lower-health-care-costs/

2https://www.stroke.org/en/about-stroke/stroke-risk-factors/risk-factors-under-your-control

3https://www.verywellhealth.com/lifestyle-factors-health-longevity-prevent-death-1132391

4https://www.health.harvard.edu/blog/lifestyle-changes-to-lower-heart-disease-risk-2019110218125#:~:text=The%20good%20news%20is%20that,disease%20risk%20by%20nearly%2050%25.

5https://www.wellsteps.com/blog/2020/01/02/benefits-of-wellness-lower-health-care-costs/

6https://www.zippia.com/advice/health-and-wellness-industry-statistics/#:~:text=Here%20are%20some%20statistics%20about,products%20is%20about%20%24168%20billion

Title:

Director of Client Services/Brokerage Practice Leader.

Joined Spring:

I joined Spring in 2015, before Spring was acquired by Alera Group.

Hometown:

I am a New Englander through and through! I was born and grew up in Boston and lived in Jamaica Plain and Roslindale.

At Work Responsibilities:

As Spring’s Brokerage Practice Leader, I work directly with employers and carriers to implement top-tier employee benefits programs for employers of all sizes. Some of most common areas include group health plans, dental, life insurance, disability, and FSAs, HRAs & HSAs.

Outside of Work Hobbies/Interests:

I love being outdoors (when the New England weather allows!). Some of my favorite things to do outside of the office are hiking, fishing, boating, and sports.

Fun Fact:

Many people don’t know this, but I was actually an extra in the movie, “Blown Away”.

Describe Spring in 3 Words:

It’s very tough simplifying my nearly decade at Spring into just 3 words. But I guess I’d have to go with professional, caring, and reliable.

Favorite Movie/TV Show:

I enjoy the classics, my favorite movies are To Kill a Mockingbird and Casablanca.

Do You Have Any Children?:

Yes, I have two children, Ryan and Kaleigh, they’re both in their 20s now.

Favorite Food:

Italian and Japanese!

Favorite Place Visited:

Although these two places are almost polar opposites, my favorites are Italy and Alaska.

Favorite Band:

I love my 80s music, so I’ll have to go with U2.

Bucket List:

I really want to visit the Pyramids in Egypt.

If You Won the Lottery, What Would You Do With the Money?:

I would start a scholarship program for disadvantaged children, to help give them a full ride through college.

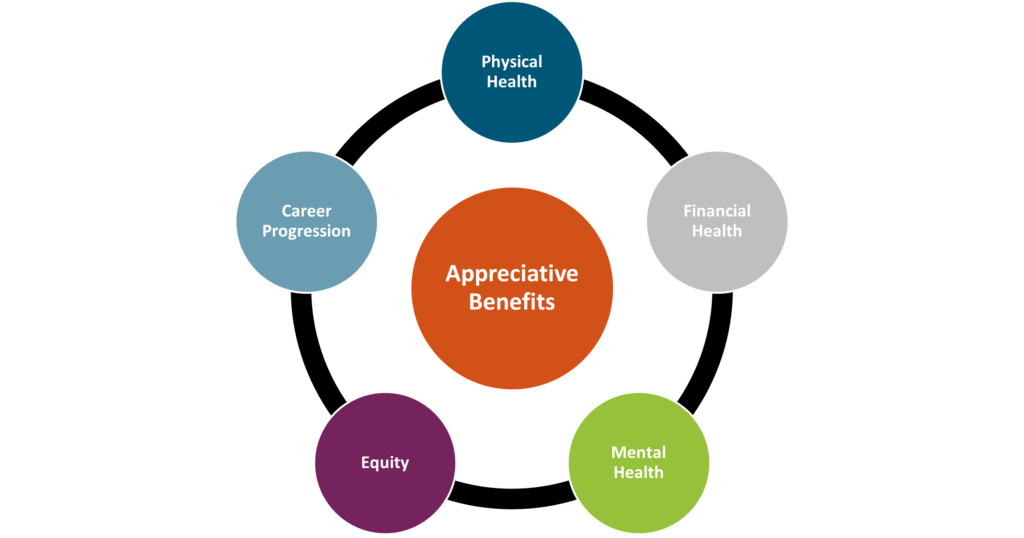

No matter the product or service you’re selling, or the impact your business makes in your community or the world at large, the consensus is that the most important asset an organization has is its people. Our HR and Benefits colleagues know very well that keeping employees happy and engaged (and keeping them in general) is not only makes for a positive atmosphere, but is also a strategic business move. So maybe you’re celebrating Employee Appreciation Day with a grateful shoutout, or a catered lunch, but don’t forget to look at the bigger picture of the precedent you’re setting – whether intentional or not – with your benefits programs.

Physical Health

Beyond the “it’s the right thing to do” mentality, benefits that support employees’ physical health are important for another reason: unhealthy employees will be far less productive, if present at all. Take a look at your health plans to ensure affordability, access, and breadth of care. Components like dental and vision insurance should also be considered here. Beyond health insurance, many companies offer supplementary tools or services that promote physical health such as fitness reimbursements, point solutions for things like diabetes management or musculoskeletal issues, health coaching services, walking challenges, and more.

Mental Health

Mental Health America reported that nearly 20% of Americans were experiencing a mental illness in 2022. The World Health Organization (WHO) states that depression and anxiety cost the global economy approximately $1 trillion every year. While employers cannot solve the mental health crisis, many believe that they do have a responsibility to provide related resources and prioritize employee mental health in some way. At Spring, we recommend tackling mental and behavioral health through the lens of its three most common barriers: cost, access, and stigma. Any programs offered should try and solve for these. For example, does your health plan cover mental health related appointments? In addition, there are a wide range of services available in this area. Some companies bring in yoga instructors on-site. Alera Group provides Spring Health at no cost to employees, which offers complimentary digital therapy sessions, coaching, and other tools. Apps like Calm and Headspace provide guided meditation and anxiety management practices. Paid time off for mental health or built-in “breaks” during the workday, such as designated times when meetings are prohibited, can also help. Simple tactics like demonstrating openness to discussing mental health in the workplace can go a long way to lessen any stigma.

Financial Health

Especially in today’s economy, employees need help saving for retirement, investing wisely, and being financially informed and educated. We also know that financial stress can be related to mental health, so by focusing on financial health you can impact multiple components of employee engagement. At a basic level, leading employers offer a 401(K) or similar retirement savings plan, with an employer match. As a next level, tax-friendly benefits like Health Savings Accounts (HSAs) can be helpful, and there has been a lot of buzz around student debt repayment programs which employers can choose to contribute to or just offer as a voluntary benefit. Other voluntary benefits like life insurance, identity theft protection and short- or long-term disability insurance can contribute to an employee’s financial wellness. Other perks might include financial counseling services and educational seminars.

Equity

Do your employees in different states have access to the same paid leave? To the same reproductive healthcare? To the same disability coverage? Do your executives and your more junior team members have the same benefits and incentives? Do your programs address a diverse range of needs, accounting for factors like location, race, gender, and age? Equitable benefits send the message of appreciation to all employees and instill the feeling of fairness and compassion.

Career Progression

Most employers take pride in hiring ambitious and hard-working employees. Don’t let your corporate structure or practices inhibit that ambition. Employees feel appreciated when they have a clear path for growth and opportunities to step up. From a benefits perspective, this might mean incorporating mentorship programs, education or certification programs, tuition reimbursement, or formal training programs.

Employees should feel appreciated on a regular basis, and not just on Employee Appreciation Day. By making sure you have these five pillars accounted for in your benefits program, you can create a positive culture of appreciation and satisfaction.

This year we had the pleasure of spending Valentine’s Day with some of healthcare’s sharpest minds within the Boston area at the Boston Business Journal’s “State of Healthcare” luncheon. Spring was excited to sponsor the event again as we take pride in both our Boston roots and in our commitment to advancing innovation in healthcare. As attendees enjoyed a delicious lunch, an impressive panel took the stage to share their different viewpoints on healthcare: Anne Klibanski, MD, President and CEO of Mass General Brigham (the Brigham); Lora Pellegrini, Esq., President and CEO of the Massachusetts Association of Health Plans (MAHP); Kevin Tabb, MD, President and CEO of Beth Israel Lahey Health; and Greg Wilmot, President and CEO of the East Boston Neighborhood Health Center.

After every conference or event, I like to take the time to reflect. Here are my five key forces impacting healthcare today, in Boston and beyond.

1. Capacity

Anne kicked things off by addressing a crisis in national healthcare: capacity, meaning there is not enough room to take in the patients who need the kind of care in which Massachusetts prides itself. In fact, every day over 200 patients within the system sit in the emergency room or elsewhere because there is no bed for them. This type of emergency capacity used to happen once every few months, but it is now the daily norm.

The problem is obvious. What is not so obvious is the solution. However, Anne provided the following insight: access is capacity. So, when we think long-term, we need to focus on efficiency and access in order to solve for capacity issues. The discussion called to mind the following questions:

– Are community hospitals being fully leveraged for the kind of care they are best suited for?

– What kind of care can be delivered virtually, and are we maximizing those capabilities? A recent development here is virtual urgent care.

– How can we increase hospital at home usage? The fact is that people prefer this method, and it increases care while decreasing costs.

– How can we increase our ability to treat patients in an outpatient or ambulatory setting? Massachusetts is near the bottom in the country when you look at the number of outpatient sites available. We need more sites, closer to home, with a lower cost model, so that we can save beds at highly specialized facilities like the Brigham for patients who need them most.

2. Affordability

Lora joined the stage to help uncover the factors behind the longstanding issue of affordability. At MAHP, they are focused on trying to make healthcare both simpler and more affordable. In Massachusetts, Lora said, we have the best data in the country regarding the drivers of healthcare costs, and that data identifies the two top drivers as unit price and pharmaceutical costs. Lora stressed the importance of the pharmaceutical and life sciences companies taking responsibility and being a part of the conversation around healthcare costs. While health plans traditionally take very little margin, and instead make most of their money from investment income, pharma on the other hand is taking in approximately a 30% profit for drugs that are sometimes federally funded. In this regard, more transparency around pricing and accountability is needed. Additionally, Lora highlighted the following affordability factors:

– Technology can and should be leveraged for things like prior authorization and streamlined credentialing. “There should be no paperwork,” said Lora. While you might be surprised that telehealth is not its own item on this list, the panelists pointed out that it is critically intertwined with affordability. Kevin pointed out that the big costs in healthcare are not individual visit payments, but rather frequent trips to the ER and people becoming sicker because they didn’t get care sooner. By marrying this goal of moving more people to outpatient or community health centers when appropriate with the access benefits of telehealth, we can make a difference in costs.

– Healthcare costs are prohibiting employers from offering other innovative benefits to employees. How can employers find a balance? For self-insured employers, which Lora says make up about 60% of the MA market, there is more of an ability to customize programs and invest in wellness initiatives and other perks. On the flip side, for fully-insured employers, especially small businesses, this is harder to do. What we see sometimes is when costs are added due to new legislation or another development, employers start considering a self-insured model, but when more parties leave the merged market, the older and sicker populations are left behind.

– The Massachusetts Health Policy Commission (HPC) is doing great work, but Lora says they hold too little authority, something that needs to change.

To expand upon this topic, Greg pointed out that the key to the cost problem was to increase access and utilization of primary care and preventative medicine, stressing that by improving health outcomes upstream, we can mitigate the downstream impacts on the rest and more expensive aspects of our health system. Community health systems like the East Boston Neighborhood Health Center plays a big role here.

3. Workforce

Kevin brought us up to speed on the core challenges in healthcare related to workforce, a topic which he emphasized is a widespread issue across industries and geographies. In healthcare, though, he explained that it is the top issue keeping executives up at night and described it as an “acute on chronic crisis.” Importantly, Kevin noted that the workforce crisis didn’t come to fruition overnight, and we won’t get out of it overnight either. We were at the edge of a precipice, and the pandemic tipped us over. At Beth Israel Lahey Health, they are focused on competitiveness of job offers, adaptation of roles and flexibility, and partnering to train up both within the community and within their system.

As Greg noted, healthcare workers have “been running a marathon at a sprinter’s pace.” He is focused on rebuilding the workforce, one that is reflective of the populations they serve and emphasized the need to focus on the next generation of talent.

On the topic of workforce, Anne added that it’s not just about salary. At the Brigham they are rethinking how to create a safe and healthy work environment. We have seen a rise in workplace violence in healthcare and beyond, so how do we better protect our staff? “We are what we tolerate,” remarked Anne, so we need to make sure we’re not tolerating behaviors and practices – both from staff and from patients and other constituents – that we shouldn’t. This brings us to our next point.

4. Equity

As Anne pointed out, allowing gender-based or racist remarks, or violent behavior prohibits the development of a safe and inclusive workplace. Greg brought a unique viewpoint to the conversation as his community health center serves a very diverse population. Smaller clinics and health centers are often over-looked, but as Greg noted, one in five MA residents are receiving care at a community health center. He stressed the need for a two-prong approach:

- What happens in the exam room, which at community health centers is largely primary care and preventative medicine.

- What happens outside the exam room. Here Greg noted the importance of social determinants of health such as behavioral health, housing stability, food insecurity, education disparities, language barriers, and technology. How do we bring these issues into governmental policy? How do we invest in communities of color to address things head-on instead of waiting until they fester into bigger problems? How do we ensure equitable opportunities in the job market?

Greg argued that only by focusing on these two health components in tandem will we make any difference in health equity, and healthcare at large.

When it comes to telehealth, a digital divide still exists related to broadband, Wi-Fi, devices, medical literacy, and age (there is a large gap in senior utilization of telehealth). This needs to be part of the equity equation too. Do we need fancy technology? Or, as Kevin pointed out, “almost everyone has a phone.” Could a phone call suffice in some cases?

Lastly, all panelists agreed that COVID-19 highlighted the inequities that had been there all along, creating an urgency around equity that we very much needed.

5. Unity

Greg left us with a powerful, albeit brief poem by Muhammad Ali to ponder: “Me, We.” His point was that while we all have a personal responsibility for affecting change, we also can’t achieve that change on our own. It takes a “me” and it takes a “we.” The consensus was that each stakeholder has a role – providers, insurers, pharmaceutical companies, the government, and so on. When these cogs in the wheel operate in silos, the wheel does not turn.

Anne remarked that when the pandemic hit, it created a galvanizing force that brought all types of parties, including so-called competitors, together for the common good. Now, the impacts of COVID-19 have faded, but the panelists pondered why we can’t use our broken system as the next galvanizing force to bring everyone to the table. Numbers 1-4 on this list cannot be addressed without prioritizing number 5. This will require more active listening and compromise.

Overall, the Boston Business Journal’s State of Healthcare luncheon provided a thought-provoking and multifaceted conversation that gave me much to think about. But as we move toward what is hopefully a brighter future for healthcare, I will leave you with one final thought from Greg Wilmot:

“If we were to rewrite our [healthcare] system, would we design it the same way? We have been writing the same story and changing the last chapter and expecting a different outcome. That doesn’t work. We need to go back and start at the beginning, and rewrite chapters 1-10.”

Greg Wilmot

Title:

Senior Vice President and Co-Founder.

Joined Spring:

I was one of the original founders of Spring (alongside Karin Landry) back in 2004, as a spin out from Watson Wyatt Insurance & Financial Services, Inc.

Hometown:

I was born and raised in Golden Valley, Minnesota (Minneapolis area), but went to college in Wisconsin.

At Work Responsibilities:

I lead our absence management team, and work with employers of all sizes and industries and leading insurance carriers and administrators in the space. I also head up our Spring’s market research surveys and benchmarking.

Outside of Work Hobbies/Interests:

Being outside, going for walks; spending time with family, and of course, watching my kids play basketball.

Fun Fact:

One thing many people don’t know about me is that I actually use to run track in high school and led the 4×100 relay.

Describe Spring in 3 Words:

Interesting work & caring culture, I guess that’s actually 5 but that’s how I would describe Spring. The people all care about each other and have each other’s backs and support each other. We have a motivated team that is eager to collaborate.

Do You Have Any Children?

Yes, I have two beautiful children, my daughter is 17 and my son is 15.

Favorite Place Visited:

Greece, by land and sea! It has to be my favorite because of the history, beautiful architecture and amazing weather!

If You Were a Superhero, Who Would You Be?:

It would be Elastigirl from The Incredibles because her arms are so long and she can hold everybody. She can take care of everything!

Last week we wrapped up Business Insurance’s 2023 World Captive Forum (WCF) in Miami, FL. This year’s conference brought together hundreds of stakeholders in the captive space to network and discuss leading trends in the industry. As a member of the advisory board, I’m glad the event was such a success; below are some of the topics I found most prevalent during this year’s conference.

1) Captive Updates

When it comes to captive regulations, we have seen many changes in just the last year. With the growth and development of different domiciles all around the world comes new regulations to which captive owners and employers must adhere. Below I have included a couple interesting sessions that explain how regulations surrounding captives have changed across the globe.

– Government insurance representatives from North Carolina, Vermont, Oklahoma, Bermuda and Michigan discussed trends, best practices and laws impacting the captive industry (and their respected domiciles).

– As Latin America has been growing their position in the captive space, a session featuring the Official Advisor for Latin American Affairs from the Government of Bermuda spoke about current LATAM trends and what we can expect to see from the region moving forward.

2) Cyber Captives

Although writing cyber liability coverage into a captive is not a new practice, it is still nowhere near as common as placing medical stop-loss or property & casualty lines into a captive. This year cyber coverage was a hot-button topic at the conference and will most likely continue to be, as cyber attacks continue to pose substantial risks.

– In a breakout session titled “Cyber Captives” a group of risk experts discussed current trends in cyber insurance and the limitations for captive coverage in cyber.

– In a session titled “Secrets Cyber Criminals Don’t Want the Insurance Industry to Know”, the CEO of BlackShield Cyber, Dioly Alexandre, explained how cybercrime has changed over time and what insurance companies need to do to keep up.

3) Healthcare & Captives

Whether an employer in the retail space is looking to use a captive to fund health benefits, or whether a hospital organization is leveraging a captive for its medical malpractice and other unique liabilities, captives and healthcare have always been closely intertwined. At WCF this year some highlights of this dynamic included:

– Spring’s Managing Partner, Karin Landry, presented on trends in medical stop-loss (MSL) and how this tactic can help employers proactively manage healthcare costs and lessen the impact of catastrophic claims. The discussion included a deep dive into what is driving upticks in healthcare costs; walk-throughs of case studies illustrating MSL advantages, including an overview of Canon USA’s captive story; and a detailed explanation of Medical Expense Cost Containment (MECC) and how it comes into play.

– The first session of the final day reviewed implications of medical malpractice coverage following the Supreme Court’s decision on abortion services and best practices for healthcare providers.

– In the session “Global Medical Claims Developments – Covid-19, Hyperinflation, Musculoskeletal and Mental Health,” the panelists discussed how captive managers should address specific medical conditions and unusual medical claim patterns.

4) The Future of Captives

Although nobody knows for certain the future of the captive industry, we are seeing various patterns that suggest we will see many changes to come. Aside from new domiciles and new types of coverages, we are also seeing different approaches when it comes to current captive practices.

– In a session on “Hybrid Captives,” I presented on innovations in the property & casualty market that allow captives to more meaningfully control property exposures and premiums.

– As a newer member to the World Captive Forum Advisory Board, I was joined by University of California’s Karen Hsi in a roundtable for younger professionals entering the industry, including a discussion of what the next generation of talent is looking for and how they can get themselves on a promising career trajectory.

– As diversity, equity, and inclusion (DE&I) is a current top priority for many companies, this session discussed how by reinvesting underwriting profits, captive programs can be used to finance DE&I strategies to meet the needs of a diverse workforce.

Getting a break from Boston winter was a plus, but the ability to reconnect with industry leaders and collaborate on strategies was the real draw. We are excited to see what the World Captive Forum holds in store for us next year and we will continue to keep you up-to-date with developments in the captive space.

the International Foundation of Employee Benefit Plans recently wrapped-up their 32nd Annual Health Benefits + Conference Expo (HBCE) in Clearwater Beach, Florida. The conference brought together healthcare and benefits professionals from a range of industries to discuss leading topics and share expectations for the future. Having heard such positive feedback about the event, Spring was glad to attend, exhibit, and speak at the conference. Below are some of our biggest takeaways.

1) Pharmacy Cost Containment

This year there was a lot of talk surrounding the price of prescription drugs and tactics employers can adopt to help control costs without cutting benefits. There are many factors influencing the high costs of pharmacy drugs, some of which include chronic disease prevalence, the aging population and the growing volume of specialty medications. Below are some of the top sessions focused on controlling Rx costs.

– Representatives from Express Scripts explained the upsides to working with a Pharmacy Benefit Manger (PBM) and how they can help address pharmacy policies in their session titled, “How to Work With Your Pharmacy Benefit Manager.”

– The CEO and Co-Founder of TruDataRx, Cataline Gorla, discussed how comparative effectiveness research (CER) is being used by other countries to decide which drugs work best for specific medical conditions, and how self-insured employers can save money with said data.

2) Addressing Chronic Conditions

According to the Center for Disease Control (CDC), 90% of the nation’s healthcare spending goes towards people with chronic and mental health conditions1. As chronic diseases are very common among the American workforce, employers have started implementing specific benefits and policies to address common conditions, such as diabetes and obesity. Some of the sessions around this topic that we found most interesting include:

– Speakers representing the Nashville Public School System explained how they were able to introduce free resources such as telenutrition and fitness center access to help combat obesity and other health disparities.

– Dr. Mudita Upadhyaya from St. Jude Children’s Research Hospital presented on prevention strategies to address mental health and obesity in a pre- and post-COVID world; and why a mixed approach may be best.

– The Diabetes Leadership Council’s CEO, George J. Huntley spoke on diabetes and chronic disease risk management strategies, including medicines and technology that can help patients manage and prevent the disease.

3) The Future of Healthcare & Benefits

In recent years we have seen a great shift in the healthcare and benefits industry; we saw a great increase in telehealth, mental health resources, new/alternative types of paid leave, including sick leave and more. As we transition to a post-COVID world, we expect the evolution to continue. Below are some of the top trends professionals believe we will face in the coming years.

– Our Senior Vice President, Teri Weber, presented on market forces employers can utilize to meet future absence management challenges. Her session listed techniques employers can adopt to improve day-to-day administration of disability, absence and accommodations.

– In a session titled “Innovative Health Care Models—The Future of Direct Primary Care,” the presenter explained how many employers are changing to value-driving healthcare models to boost access and reduce costs.

– A session titled “Breaking the PTO Mold, Without Breaking the Bank,” reviewed how typical Paid Time Off (PTO) programs can be altered to better support employees’ well-being and financial health.

– The final session of the conference spotlighted how the pandemic has led to an increase in personal, economic and other stressors and has had a drastic impact on mental health, substance misuse and addiction. Attendees were informed on how they can implement workplace solutions that address these issues as well as identify warning signs.

The warmer weather was certainly a bonus, but the insights we gleaned and connections we made were what will keep us coming back to the HBCE conference. We want to thank IFEBP and our fellow colleagues who took the time to share their experience, stop by our booth, and make the energy so positive.

1https://www.cdc.gov/chronicdisease/about/costs/index.htm

Our Senior Vice President, Prabal Lakhanpal wrote an article for the Boston Business Journal on how employers can continue to provide strong benefit packages during a time of high inflation. You can find the full article here.

As seen in the New England Employee Benefits Council (NEEBC)’s blog.

Last year around this time, I gave a year-one progress report on the Massachusetts Paid Family and Medical Leave (PFML) program, as it had finished its first year of paying out benefits to eligible workers. Since then, the MA PFML program has continued to mature and adjust according to experience, and, around New England, Connecticut has had PFML benefits available for one year, and there are related updates from Rhode Island, New Hampshire, Vermont and Maine to report.

Massachusetts: A Year in Review

In fiscal year 2022 (July 1, 2021 – June 30, 2022), the Massachusetts Department of Family and Medical Leave (DFML) experienced1:

– Over 112,500 applications, with 20% being denied

– 59% of applications were related to medical leave, 31% for bonding, and 10% to care for a family member

– Only 32 approved applications for military exigency leave and 7 approved applications to care for a service member

– Claimants aged 31-40 had the most approved claims (40%) and more than 1.5 times as many women had an approved leave (61% of claims), compared to men (35% of claims)

– Average weekly benefits were $793.55 for family leave and $754.84 for medical leave

– Turnaround times from the time the application was submitted to an initial decision was a median of 17 calendar days

– Average duration of leave was 12 weeks, assuming a 5-day work week

– Total benefits paid was equal to about $603 million (an increase of about 245% from FY21 which accounted for January 1, 2021-June 30, 2021)

In 2023, Massachusetts will be updating maximum benefit amounts and reducing total contributions.

– The maximum weekly benefit is increasing to $1,129.82, effective 1/1/2023. This is an increase of about $45 from the 2022 weekly maximum. For any employees who may have leave that runs from 2022 into 2023, the weekly benefit that was determined when leave was approved will continue. The new maximum will not be applied until there is a new MA PFML leave application.

– Contributions, however, will be reduced in 2023. The total contribution is decreasing from 0.68% to 0.63%, for employers with 25 or more covered individuals. The medical leave contribution will be 0.52%, with employers funding 0.312% and employees responsible for up to 0.208%. The family leave contribution will be 0.11%, with employers able to collect the total contribution from employees. Employers with less than 25 employees are not required to submit the employer portion of premium.

The financial earnings requirement was also updated in 2023. Employees must have earned at least $6,000 and 30 times the PFML benefit amount during the base period to be considered eligible for MA PFML.

Connecticut: First Year Activity

Connecticut has now had PFML benefits available for 1 year. During the first six months of the program2:

– Over 44,127 applications, with 40% being denied of those that received a decision

– 44% of approved applications were related to medical leave, 29% for bonding (own child and adoption/foster care), 18% for pregnancy/childbirth, and 9% to care for a family member

– Only 15 applications were approved for family violence, 12 for organ and bone marrow donation, and 2 for qualifying exigency

– Claimants aged 26-41 had the most filed claims (53%) and more than double the number of females applied for leave (28,814), compared to males (14,213)

– Average weekly benefits paid were $562.01

– Average approved duration of leave was 6.79 weeks

– Total benefits paid was equal to about $81 million

– Almost 137,000 businesses have registered with the CT Paid Leave Authority and claim applications have been received from every city and town in the state

Based on the experience in the state in 2022, Connecticut is not making any major changes to the program in 2023. However, the social security contribution and benefit base increased to $160,200 on January 1, 2023, and CT minimum wage increases to $15/hour on June 1, 2023, which will impact benefit and contribution amounts.

Please note that the program has some key differences when compared to MA PFML, such as the availability of leave for organ and bone marrow donation, as well as leave related to family violence. Differences in benefit amounts, leave duration, and eligibility conditions also make it difficult to directly compare CT and MA PFML experience.

Other New England Updates

Massachusetts and Connecticut are not the only New England states to be seeing PFML progress. Rhode Island has an established temporary disability insurance program (TDI), which was the first statutory disability program in the country, established in 1942. In 2014, they became the third state to offer family leave benefits through temporary caregiver insurance (TCI). In addition, the state does not allow private plans, making the model slightly different than other PFML programs in the region. On January 1, 2023, a few updates to TDI and TCI became effective. The state’s taxable wage base increased to $84,000, which will impact the contribution calculation. The benefit duration also increased to 6 weeks, from 5 weeks in 2022. Finally, the financial eligibility conditions claimants must meet increased so that employees must have paid at least $15,600 in the base period or meet the alternative conditions wherein they earned at least $2,600 in one of the base period quarters and base period taxable wages equal to at least $5,200.

A new outlier is New Hampshire’s first-in-the-nation, state-sponsored voluntary plan where NH employers and eligible NH workers can purchase a paid family and medical leave plan through the state’s insurance carrier. New Hampshire selected MetLife as its insurance partner and began paying benefits on January 1, 2023.

Similarly, Vermont spent 2022 developing a voluntary program to be administered by The Hartford, their selected insurance carrier. Beginning July 1, 2023, state employees will be covered under the program, with other private and public employers with 10 or more employees eligible for coverage in 2024, and small employers and individuals able to purchase coverage in 2025.

Maine also made strides in developing the structure of their state mandated PFML program. Maine created a commission to study PFML programs and to propose a PFML model for the state, which kicked off in May 2022. Policy recommendations are expected to be presented to the Legislature in 2023.

Are You Up to Speed?

As the PFML landscape continues to evolve at the local, state and federal leaves, policies need to be monitored on an ongoing basis. Employers should ensure they are compliant with the requirements of each individual leave program, as differences exist between all established paid family and medical leave policies. If any of your employees are impacted by a state PFML policy, organizations should review plans, policies, and processes to confirm they are in line with any legislative changes. To do so, the following checklist can be followed:

– Register in any new states where employees are located, if required

– Ensure contributions are being collected appropriately

– Update employee notices and benefit documentation, as appropriate

– Confirm employee count to determine if any changes to contributions are required

– Review private plan strategies based on previous year experience and changes to contributions

– Renew private plans as appropriate

– Validate company sponsored leave programs coordinate with PFML to the extent possible

If you need assistance ensuring PFML compliance or to assess the optimal plan set up for your organization, Spring’s consultants are happy to help www.springgroup.com