As seen in the New England Benefits Council (NEEBC) blog.

We are one year into eligible Massachusetts employees being able to apply for paid leave benefits under the Massachusetts Paid Family and Medical Leave (PFML) program. Although stats for the MA PFML Rookie Year have not been released yet, the first six months were telling:

- Over 53,000 applications, with 23% being denied

- 58% of applications were related to medical leave and the remaining for bonding, given that care for a family member with a serious illness was not yet a covered reason

- Only 18 applications for military exigency leave and 6 applications to care for a service member

- Employees aged 30-39 submitted the most applications (35%) and more than twice as many women applied for leave, compared to men

- Average weekly benefits were $705.98 for family leave and $699.00 for medical leave

- Turnaround times, once the Department of Family and Medical Leave (DFML) received all data including employer responses, took a median of 12 days to make a claim determination

- Average duration of leave was 53 days (57 days for medical leave and 51.5 days for family leave)

- Total benefits paid was equal to about $168 million (about $92 million for medical and $76 million for family leave)

While we await data for season of 2021, let’s dissect the highs and lows and see if MA PFML has a shot at Rookie of the Year!

Let’s start with the highs:

The plan appears to be running at a sustainable level with sufficient funding, indicated by a reduction in contribution rates, which is good for residents of the Commonwealth.

Employers were able to successfully create private plans without significant hurdles in the process, allowing MA firms to continue their history of rich benefit designs without negatively impacting corporate plans.

Massachusetts has been a strong example of early and broad education of the program. Individuals in the state were told about benefits that may be available to them in plenty of time before the program went live, giving them the opportunity to ask questions and better understand what their experience might be in the case they need leave. The state hosted various webinars to different audiences, providing real time information and continuous updates on the status of the program’s launch. The website houses a multitude of helpful information and is continually updated. For questions not answered in these channels, individuals may also call the DFML for benefit questions or the Department of Revenue (DOR) for questions concerning private plans or contributions, and the state is typically always able to answer even in-depth questions.

While the state has had multiple home runs implementing a PFML program, just like evaluating Rookies of the Year like Jonathan India and Kyle Lewis, we need to think of the swing-and-a-miss situations as well. The most significant strike for the MA PFML was their system:

- The system for PFML administration continues to lag with the most significant unexpected deficiency likely related to their inability to handle intermittent leaves which are the most challenging and frustrating for employers.

- Employer access was an obstacle, leaving employers without the ability to “monitor” claims or have insight into the status at a time when COVID claims and time away from work were skyrocketing.

- Another systematic issue was linking contribution with plans. Since contributions are due at the close of the quarter, claims could be reported prior to contributions being paid. Unfortunately, those triggered denials as employers struggled to notify the state, register and swap from private plans to the state plan. Employees were given conflicting information as employers tried to resolve this gap in “coverage.”

Just like anyone’s first year in the pros, our first year with MA PFML threw us curveballs we did not expect, and as a result, we have learned some important lessons. The ever-evolving landscape of PFML laws has put pressure on employers with employees across the country, as they try to meet employee needs while balancing corporate responsibilities and equity. As we all become more seasoned players in this complex game of leave, Spring has outlined some best practices for employers handling PFML:

- State plans should act as guidance for internal company policies. Mimicking a state plan could be restrictive as new programs emerge and existing programs evolve.

- Have a clear understanding of the definition of eligible employees under each statutory and/or federal law. Someone considered an employee in Massachusetts may not be considered an employee in Connecticut (e.g., 1099 contractors).

- All leave policies should be run concurrently, to the extent possible. The Federal Family and Medical Leave Act (FMLA) will generally run concurrently with MA PFML and other PFML laws when an employee meets the eligibility conditions of both plans.

- Private plans offer the most flexibility with plan provisions and aligning leave with other corporate leaves, however state plans seem to be simpler administratively. Carefully weighing these pros and cons is key to developing an adaptive leave program.

The replay we are watching the most, however, is that COVID-19 significantly increased the complexity of such a program. The need for leave has been exacerbated. Difficulty hiring employees has affected employers who must keep up productivity while more employees are away from their jobs, and the state had to administer a new leave program under less-than-ideal conditions. In addition, the tremendous growth of remote work has made it difficult for employers to determine where an employee may be eligible for leave.

Overall, workforces are evolving and regulations at the local, state and federal level need to be continually monitored. As we see benefits become available under new programs, such as CT PFML, and other states pass bills to develop PFML programs, such as New Hampshire and Maine, employers will need to assess their strategies and evolve accordingly.

As seen in the Captive Review Group Captive Report, September 2021.

With the rapid spread of the Delta variant, the Covid-19 pandemic continues to leave employers with a series of unpredictable risks directly related to the pandemic. Among these risks is the potential higher cost of healthcare benefits offered to employees, a factor which must be built into any long-term risk management or cost-containment strategy. Covid-19’s impact on healthcare costs Based on tracking data across multiple employers, the future impact of Covid-19 on high cost claims will directly impact health insurance. Key factors include:

Direct costs related to Covid-19

Costs associated with testing, treatment and vaccines remain a primary source of plan costs. The most direct impact on captives is the high cost treatment tied to severe hospitalizations, particularly due to potent strains of Covid-19 like the Delta variant. There may also be ongoing health needs for members who recover from Covid-19 or are long-haulers.

Deferral of care

Plan members have chosen to defer elective treatments. While some of this care was eventually incurred over the course of the last year, many plan members continue to hold back on care, whether because of discomfort in a hospital setting or difficulty in finding care due to bandwidth issues. This influences future costs, particularly with unpredictable costly surgeries.

Missed preventative care

Client data across industries also showed a significant reduction in preventative care visits, and lower test numbers in areas such as labs, CT scans and MRIs. As a result, many employers are concerned because if certain health issues are not identified and treated early, the severity of the case and corresponding cost of care may be higher down the road.

Behavioral health

Covid-19 propelled behavioral health issues into crisis levels. While it may seem indirectly related to broader healthcare, consider this: the national Alliance on Mental Illness reports that cardiometabolic disease rates are twice as high in adults with serious mental illness, and that depression and anxiety disorders cost the global economy $1 trillion annually in lost productivity. We are sure to see the repercussions of this in claims costs to come.

Health insurer risk premium margins built into insurance pricing have been increasing in light of all this uncertainty, as well as broader trends such increased prevalence of high cost specialty drugs and increasing hospital costs. In fact, the most prevalent specialty medications are increasing in price at 10%-15% annually, further contributing to unpredictability of future claims.

Employer Considerations

During the pandemic, employers have needed to confront their organizational philosophy on the employee value proposition and balancing the investment in employee benefits with the impact on the company’s stakeholders. The impact of Covid-19 has made employers more acutely aware of the need for sufficient healthcare coverage for employees and their families.

In order to provide attractive benefits in an environment of rising costs and volatility, employers must rethink the programs they offer and how they are funded. Many organizations have also revisited benefit program governance structures, how decisions are made, and how programs are monitored.

Perhaps your remote workforce has different needs than they did in 2019, or the pandemic has triggered new problem areas that can be addressed through wellness solutions or advocacy tools.

No matter your path, employers seeking to ensure that they offer comprehensive healthcare benefits to employees at an affordable cost need to consider the financial management benefit of potential long-term cost savings and mitigation of volatility associated with captive structures.

Captive Arrangements for Employee Benefits

As employers look at the impact of the pandemic, organizational planning requires balancing the increasing cost of healthcare with the risk associated with solutions that reduce the total cost of the program. At its simplest form, health insurance can be expensive if a fully insured program is purchased, as organizations pay a risk margin, often 20% to 40%, for transfer of the risk to an insurer. Small to mid-sized organizations typically mitigate this cost by self-insuring a portion of their healthcare risk with medical stop-loss to cover higher cost claims. However, the higher risk premiums required by health insurance, including stop-loss insurance, lead to steep healthcare plan costs and/or, in some cases, being forced to take on higher-than-optimal risk.

A captive arrangement is a strategic way for employers to benefit from self-insurance while creating a sustainable solution to partner with commercial markets. Captives provide substantial competitive advantages over traditional self-insurance, such as:

Reduced total cost of insurance

Insurance carriers develop premiums by heavily weighing on industry averages, state rates and, to some degree, on an employer’s individual loss experience. This may lead to pricing that may not accurately reflect an organization’s actual loss experience. Insurance carriers usually price to include substantial overheads, including risk and profit margins. A captive provides employers an opportunity to recapture premiums from the commercial market and build a sustainable long-term model for their insurance needs.

Insulation from market fluctuations

Conventional commercial insurance is vulnerable to market fluctuations. This has never been more evident than today, with hard insurance markets and premiums that are increasing substantially with almost no change in coverage level. As a member in a captive program, employers are less susceptible to unpredictable rising costs imposed by conventional insurers every renewal season, as a balanced funding approach can smooth the cyclical volatility of the commercial insurance markets.

Protection from cashflow volatility

Leveraging a captive to fund medical stop loss can lower the cashflow volatility often faced by self-insured programs on a monthly basis. Having a captive cover claims at a substantially lower stop-loss level allows employers to smooth out plan funding and mitigate cashflow risk to the company.

For employers that may not have their own captive or the resources to form one, there are a variety of group captive solutions in the medical stop-loss space. These solutions are turnkey in nature and simple to implement. Most well-structured group captive programs aim for a seamless transition for employers where there is almost no disruption. In other words, from an employee’s perspective, the claims process is entirely the same. With group captives in particular, all the mechanical aspects are handled by the group captive management team, with minimal effort required for an employer.

There are several group captive arrangements that employers can tap into. In selecting the most appropriate arrangement, you need to consider factors such as the upfront cost of the program, the extent to which customization will be available, the flexibility you will have for your organization within the group captive model, and how renewals will work.

Looking Beyond the Pandemic

As we look forward beyond the pandemic, employers should consider ongoing healthcare program effectiveness. Healthcare costs will continue to increase and become a larger portion of organizational budgets, but it is not too late to start leveraging innovative solutions to mitigate these costs. You can proactively adjust your tactics today and be better prepared for tomorrow, and with a captive you are truly in the driver’s seat.

Brokers have had to tread carefully when discussing mask and vaccine mandates with their clients. Here is our perspective, via BenefitsPRO.

As seen in Captive International

As the dust begins to settle on the COVID-19 pandemic, forward-thinking organizations are focused on programs that provide competitive benefits as they look to lure new workers and retain existing employees. They recognize that employee benefits give them flexibility to deal with the changing employee landscape, from a demographic and geographic perspective, as well as improving employee wellness, maximizing their savings and increasing employee engagement in the modern era.

COVID-19 impacted insurance coverages and industries differently, but a picture is emerging of what the employee benefits landscape will look like post-pandemic

Prabal Lakhanpal of Spring Consulting

A holistic approach

Historically, employers were largely focused on ensuring they had adequate insurance coverage on a line-by-line basis, and these coverages often operated in silos. Today, more organizations are breaking down those silos and developing a view that is holistic, looking across the board to create an employee benefits program that emphasizes employee wellbeing and population health management.

Employee wellness is primarily the idea of not just providing employees with appropriate health, life and disability benefits, but also ensuring that employees have assistance regarding their overall wellbeing, including physical, financial, behavioral, social and intellectual health. Organizations increasingly understand how the individual components of their benefits programs are inter-related, and that evaluating and managing these relationships adds value to their employees.

A captive is an effective mechanism for achieving an integrated program. In an integrated captive program it is easy to bring together all the lines and ensure that the appropriate resources are being used to plug any gaps in the benefits portfolio. Most of our clients using this approach have been able to leverage the savings from the captive program to provide the additional coverages at almost no or nominal cost.

In addition, the transparency and clear line of sight into claims activity and utilization rates help employers plan for program changes, make decisions and adjust to changing employee needs sooner than they would be able to without a captive. Organizations that already had benefits in their captive when COVID-19 hit fared much better than those without one, as they were able to adapt quickly to make changes to their benefits that accounted for the unusual circumstances.

For example, we helped a large global employer leverage its captive to provide extended benefits for employees it was forced to furlough when the pandemic struck. Its carrier would allow for continued benefits for only three to six months, but by using the captive to take on the risk, the organization was able to keep benefits for furloughed employees for 12 months at no additional cost. This move went a long way to improve employee retention and morale.

Medical stop-loss

If we think about the range of employee benefits in the US, medical stop-loss is perhaps the one that has changed the most and attracted the most interest in the last few years. It is typically not an Employee Retirement Income Security Act (ERISA) benefit so Department of Labor (DOL) processes don’t apply.

There are two driving forces behind this interest. First, healthcare costs continue to skyrocket, causing employers to look at alternative ways to bend the healthcare cost. Medical stop-loss in a captive is a smart, cost-conscious response to these market conditions.

The second factor is that for a long-time medical stop-loss has largely been considered a first-party risk. Over time, law firms and accounting firms have gradually started to categorize it as a potential third-party risk.

This transition to medical stop-loss being a third-party risk is gaining substantial traction and impacting the way programs may be structured to achieve insurance tax treatment. This concept needs to be individually assessed at the employer level, considering the circumstances of the organization. We highly recommend working with a captive attorney or tax advisor to ensure compliance.

Life and disability

Life and disability are other lines that have changed significantly in recent years. Typically, any coverage subject to ERISA needs to go through a DOL exemption process in order to be placed in a captive. Life and disability are usually subject to ERISA. Historically, the DOL had an expedited process, which allowed employers to submit an application for approval to add benefits to a captive.

In late 2018, the DOL paused this process in order to rethink and better understand how employers are using these benefit lines in a captive. They have since conducted an analysis and created a more streamlined exemption process for which we are already seeing applications flow through the DOL.

As we look to the future, I believe this will encourage more employers to think about life and disability as potential coverages for captives. These coverages not only help employers achieve best-in-class benefits provision, they also support captive insurance structure from a diversification point of view.

Another growing area of interest is the self-insuring of employer-paid disability coverages. This is an extremely useful solution for organizations and is quick to implement, but the feasibility of this needs to be evaluated on an individual employer basis.

Voluntary benefits

While not new, voluntary benefits continue to pick up steam in the market. This trend correlates in part to my first point about a holistic approach, as voluntary benefits can offer a range of different protections that are not part of a traditional benefits package. In this way, employers and employees can address a larger spectrum of health and wellbeing concerns such as vision, financial wellness, or accident insurance, thus creating a more comprehensive program.

Voluntary benefits are an important tool to have as employers fight against rising healthcare costs, as they are a low-to-no-cost mechanism to support employees in managing those increasing costs.

Last, as most voluntary benefits are underwritten at extremely low loss ratios, insurance carriers make a substantial profit from a voluntary benefit that is fully-insured. By utilizing a captive (self-insured structure) for voluntary benefits, the employer can further reduce benefits costs for its employees. It’s a classic win-win.

Conclusion

The “new normal”, whether it feels normal or not, is not on the horizon, but at your doorstep. Cutting-edge businesses are taking a modern approach to address the challenging market conditions while still providing competitive benefits, retaining and attracting talent, and being risk-smart and mindful of their bottom lines.

Thinking holistically and reframing your strategy around medical stop-loss, life and disability, and voluntary benefits are just a few of the ways you can use your captive to stay ahead.

Our Managing Partner, Karin Landry was in a Q&A with Financer Worldwide, in which she discussed some of the leading healthcare risks and what changes we can expect to see in the insurance market. Check out the full discussion here.

Dazed & Confused

Think about your last visit to the doctor. Did you know what questions to ask? Did you leave with a clear picture of the next steps or alternative options? Did you know the cost of your appointment and treatment path before starting it, or what would be covered by your health insurance? If you answered “no” to any of these questions, you are certainly not alone.

Bend Financial[i] recently conducted a survey that showed that only 29% of people were completely confident in their ability to navigate the healthcare system, whereas 56% were entirely confused when it comes to health insurance. Unfortunately, an alarming subset of consumers opt to avoid healthcare completely, too defeated by the complexity.

Beyond health insurance, employees must navigate the suite of benefits offered to them by their employer. While these are meant to provide support, they can cause more confusion when employees are looking for assistance. Employers must consider how introducing a new program or benefit will fit into their overall strategy and integrate the resources, without adding to the complexity employees face.

[i] https://www.bendhsa.com/newsroom/more-than-half-of-americans-confused-by-health-insurance-including-hsas

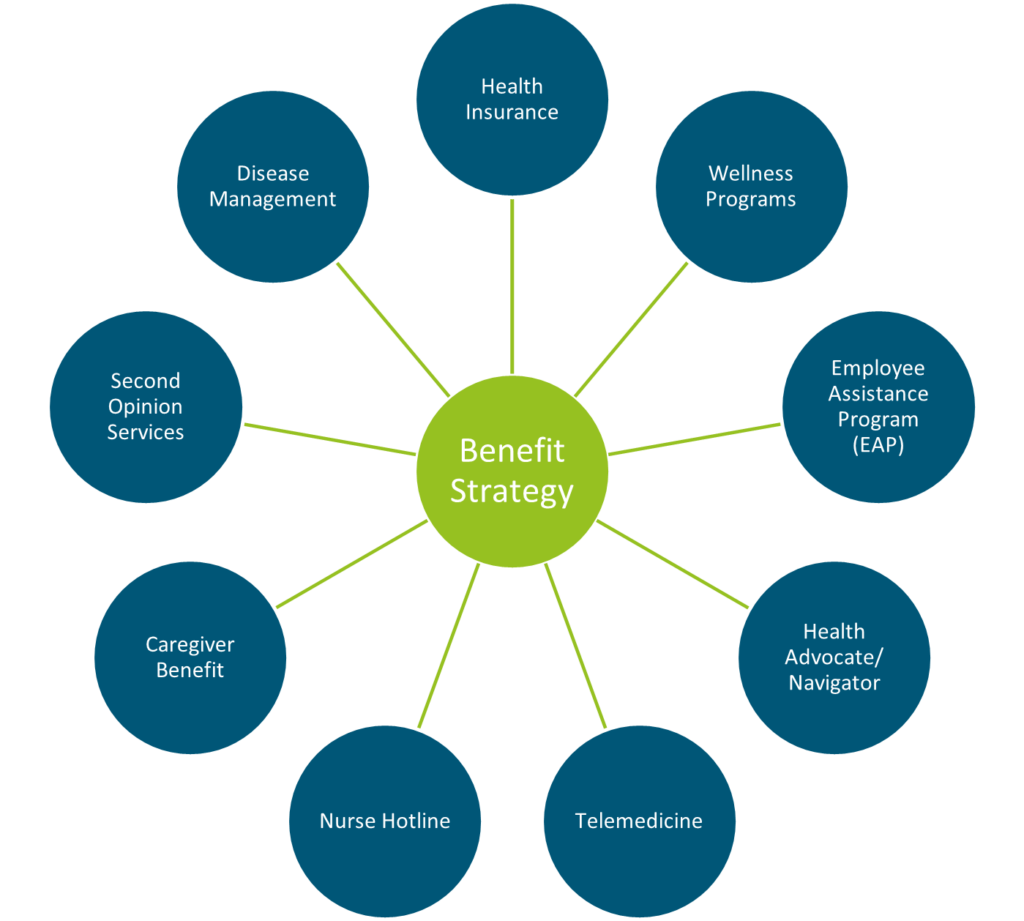

Breaking Through the Fog

Advocacy tools have popped up as a response to the confusing environment. These tools offer a wide variety of clinical, educational and administrative resources, such as:

- Helping members understand test results or treatment plans

- Advocating for members with complicated conditions and managing their care

- Coordinating care at inpatient facilities

- Identifying top providers

- Arranging second opinions

- Providing information about alternative prescription options

- Assisting employers to understand health risks through biometrics, claims and other data

- Developing customized Employee Assistance Programs (EAPs) or other life coaching services

- Reviewing medical bills and allowing for transparency of costs

- Facilitating prescription drug delivery

- Assisting with wellness goals

- Accessing telemedicine

- Booking appointments and sending reminders

- Optimizing HSA, FSA and HRA accounts

- Integrating with other vendors offered by the employer

The landscape for these platforms is robust and ever-changing. The spectrum of vendors include those that offer:

1. Holistic approach

Major players may provide all of the above features on a one-stop shop model for employees.

2. Preventive approach

Some vendors focus on prevention of common conditions, encouraging employees to get annual eye exams, diabetes screenings, cancer screenings, medication adherence, and more.

3. Targeted approach

This last category of vendors specialize in support for employees with common chronic conditions including diabetes, hypertension and high cholesterol. While likely not the most costly conditions, the potential for savings and member support is significant when factoring in the volume at play. These vendors aim for condition management by giving members the tools to monitor and manage their conditions better on their own, hopefully necessitating less emergency care in the future.

Comparatively, other tools focus only on the highest cost conditions and members, such as cancer diagnoses. Offering a specialized tool for members going through this difficult time enables them to procure the best and most cost-effective care, while also giving them access to resources related to nutrition, mental health, and more. While available on a standalone basis, advocacy solutions may also be accessible to employers through their insurance carriers, Third-Party Administrators (TPAs), or Employee Assistance Programs (EAPs). Programs embedded with a carrier or TPA tend to focus on overall health management programs, disease management and wellness, as well as resolving billing issues and comparing costs of providers. A commonality across platforms is the prioritization of the consumer experience – offering easy, self-service access in mobile apps or online portals. Members typically have a single point of contact at the advocacy company, so they know who to call and do not have to navigate being transferred or having an unfamiliar staff member pick up their case. Overall, for employees, health advocacy platforms may:

- Help them get the most out of their insurance plans and programs

- Cut through the clutter of healthcare

- Promote health and productivity

- Increase preventive behavior

For employers, health advocacy tools can:

- Cause an uptick in employee engagement and satisfaction

- Increase health plan utilization.

- Yield savings in healthcare costs by allowing employers to better understand cost drivers,

- Facilitate the creation of more informed preventative and wellness programs and ultimately lead to a healthier population

Advocacy Adoption: Is It Right For You?

Ultimately, it is up to the employer to determine what programs would best support their employees. Based on the 2020 Integrated Disability Management (IDM) Employer Survey conducted by Spring Consulting Group, 61% of employers offer a health advocacy solution today, compared to only 41% in 2018. Determining which model and which vendor to select can be difficult as there are many players in the market. In assessing whether an advocacy tool would be a good fit for your organization, any decision around advocacy solutions should be tied to program objectives.

- Are you primarily concerned with cost savings?

Health advocacy solutions can provide cost savings to employers or health plans, as they direct employees to access only necessary healthcare services, perhaps at a lower cost facility than they otherwise would have used. A tool like this should, in theory, help avoid bigger, high-cost problems down the road by assisting the employee with addressing issues early. Certain vendors may even offer a cost savings guarantee. However, it will take time to see a possible Return on Investment (ROI). On the flip side, an advocacy solution can encourage greater utilization, such as for behavioral health services. While a higher utilization rate may mean increased claims, giving employees tools to access the services they need can lead to less emergent or high-cost care down the road. As such, you should determine if you are looking for immediate or long-term results.

- Are you looking for higher engagement in your health and benefits plans?

There is a lot of logic behind the argument that an advocacy tool will increase engagement. However, if an employer has had trouble engaging employees in the past, such as in wellness challenges, incentives, education, etc., nothing is guaranteed. Vendors claim that anywhere from 30% to 80% of employees will participate in their program, but this is highly variable based on different aspects of the program and the employer, such as program features or employer incentives.

- Are you focused on population health management?

By equipping members with the necessary tools to make health care decisions based on value and outcomes, better outcomes are achieved. The plan data will guide your decision related to population health management. For example if you are struggling with diabetes specifically, you may want to consider a targeted point solution focused on diabetes management before committing to a more comprehensive program that tends to be more expensive.

- Are you hoping to improve the employee experience?

With an advocacy tool, members have support to mitigate confusion around healthcare services, surprise billing, complex diagnoses…but it only works if members leverage the support. Programs should be communicated often and where possible linked to activity within the plan. We always recommend eliciting employee feedback before launching a program such as this, to ensure you are solving for problems that really exist for employees, instead of problems you think exist for employees. Sometimes our clients even roll out a smaller pilot program as a test before implementing the wider solution for the whole organization.

Most organizations will have a few different goals at play, which are not limited to those listed above, but typically there is a hierarchy to consider. Working with a trusted advisor can help to understand key differences and ensure programs are designed to work for the employer and their employees. At Spring, we routinely help employers vet solutions to find the one that is optimal for their goals and population.

Conclusion

Overall, health advocacy tools have risen in popularity for a reason. They address critical problems in our healthcare system – confusion, expenses, access, lack of trust – and serve as a different avenue for employers to limit the rising costs associated with healthcare. Advocacy helps ensure employees are understanding the care they receive and have greater visibility into actual costs. While results will vary by platform and organization, vendors are confident in their results; they report significantly lower healthcare trend for clients, compared to previous years when there was no advocacy program in place. With an ever-changing landscape, it is possible that health advocacy programs can bridge the gap between consumers and care, but only time will tell if they can make a long-term impact on the market.

Our Senior Vice President, Teri Weber spoke in a panel discussion hosted by the Boston Business Journal. She discussed the importance of mental health resources during the pandemic. Check out the article here.

Our Senior Vice President, Teri Weber published an article in the Boston Business Journal explaining how organizations can better support employees who also act as caregivers. Check out the full article here.

Employees bring their whole selves to work each day which allows for the highly efficient, effective, and creative workforce we enjoy. As Human Resource professionals we appreciate the diversity of our workforce and continue to adjust within our employee benefit programs to meet the changing needs of our employees and their families. Top employers know that thinking more strategically about caregiving will help them fight for top talent and provide the corporate culture employees are seeking especially in this more complicated caregiving landscape brought on by COVID-19.

The concept of caregiving is not new but as our workforce evolves it is becoming more critical to consider caregiving as an area of opportunity within employee benefits. This shift, further amplified by the pandemic, highlights a cavern between top tier employers who appreciate the multitude of responsibilities employees must navigate versus those that hire people despite them.

The Rosalynn Carter Institute for Caregiving recently released Caregivers in Crisis: Caregiving in the Time of COVID-19. This thoughtful piece attaches hard data to the burden we have all experienced over the last 6 weeks. The data indicates that 83% of caregivers have increased stress since the start of the pandemic, and 42% have indicated that the number of other caregivers available to help them has declined. Caregivers themselves – in addition to those requiring care – are experiencing an increased burden from isolation, stress, financial concerns, and general instability.

Employers that are new to the concept can consider caregiving solutions as a continuum or suite of solutions; not a one size fits all approach or something that has to be implemented all at one time. A core offering typically includes:

- Educational resources

- Advocacy support

- Self-service tools

Enhancements allow for 24/7 live support and paid time off when necessary to address caregiving emergencies.

Defining Caregivers

AARP estimates that each year approximately 40 million American adults provide support to others with basic functions (i.e. activities of daily living). Many of those, including 75% of millennial caregivers are working.

For millennials in particular the stress of caregiving can be more challenging since they are typically providing care for more hours in a week, making less money and having less support from other family members (i.e. reduced family size). Also of note, millennials are the most diverse caregiving community to date (i.e., racially, ethnically and more likely to identify as LGBTQ+) which can be important to consider related to diversity and inclusion.

It is important to think broadly about caregiving solutions. In addition to introducing separate solutions, it is equally important to shift our mindset and expand common employer benefits that could be leveraged for extended family members (i.e. second opinions, medical guidance with challenging health diagnoses, etc.). The term caregiving must also extend beyond elder care of medical conditions but include children struggling with online school or developmental disabilities or Medicare eligibility and financial planning when moving into retirement. The goal of caregiving solutions is to support your employees as both caregivers and those needing care.

We have all heard the announcement on the airplane about putting on your own mask before helping others; employer sponsored caregiving is building on that logic and allowing your employees to more efficiently:

- Find educational information related to their caregiving needs

- Direct employees toward potential solutions

- Provide tools to support decision making

- Pair employees with short-term and long-term caregiving solutions

Caregiving support as an employee benefit is still in its infancy. Unfortunately, many employers do not realize the need, the impact on employee performance and the demand that exists at the employee level. A 2019 Harvard Business School Study, The Caring Company, indicates that while only 24% of employers surveyed believed employee caregiving influenced their employees’ performance at work, 80% of employees surveyed admitted that caregiving had an effect on their productivity. In addition, 32% of employees surveyed indicated that they left a job because of their caregiving responsibilities.

Employers who take a proactive position on caregiving support – along with the tools needed for successful roll out and measurement – will see a direct impact on attraction, retention, productivity, and corporate morale.

If your organization is interested in exploring caregiving support as an employee benefit, or is ready to identify partners for a best practice roll out, please reach out to our team.