Menopause support has rapidly shifted from a taboo topic to a fast-growing area of interest in an employer’s benefits offering, driven by workforce demographics, productivity risk, and a wave of specialized digital health platforms.

Menopause impacts most women between the ages of 40 and 58. Symptoms may range from hot flashes, joint pain, headaches, and fatigue to anxiety, insomnia, brain fog, and memory lapses. Women facing these challenges make up a significant portion of the workforce, with women aged 45 to 64 accounting for approximately 17.5% of the workforce according to the Department of Labor. Women going through perimenopause or menopause often experience these symptoms without support options from their employer, leading to missed workdays and loss of productivity at what may be a pivotal time in a person’s career. Studies estimate that menopause-related symptoms cost employers billions annually due to lost productivity and absenteeism, with many employees reporting reduced performance or considering leaving the workforce altogether.¹ Recent analysis from Forbes further emphasizes that organizations supporting employees through menopause may see improved retention, engagement, productivity, and overall workforce wellbeing, reinforcing menopause support as both a health and business strategy.²

Support for women going through menopause may take several forms.

- Menopause Leave or Time Off Programs: Employers are beginning to explore and launch designated time off programs for employees needing time away from work due to symptoms related to menopause that may not be covered or recognized under other leave policies. Recent developments also highlight the growing momentum behind menopause workplace accommodations. For example, Hone Health recently launched its “Menopause Time Off (MTO)” initiative, advocating for menopause-inclusive leave policies and workplace flexibility.³

- Telehealth with Menopause-Trained Clinicians: In today’s healthcare landscape, many individuals face fragmented care across primary care, mental health, and OB-GYN providers. Traditional care models often lack specialized menopause training, leading to underdiagnosis or undertreatment. Telehealth programs may assist in bridging this gap by providing holistic care plans designed specifically for the individual. Employers can access menopause support either through standalone point solutions (e.g., Midi Health) or through enhancements within existing medical or telehealth offerings. It is important to note that some solutions may already be covered under current insurance plans. Telehealth does not need to focus only on establishing care plans. These services may also expand to prescription treatment, virtual physical therapy, mental health support, and additional specialized services.

- Inclusion of Hormone Therapy in Medical Plans: Menopause Hormone Therapy (MHT) can be a beneficial approach for treating common symptoms of menopause such as hot flashes and bone loss. Hormone therapy should be tailored to each individual’s needs. Insurance typically covers FDA-approved formulations, but the specifics of the plan will dictate how much an employee will pay and the exact requirements for coverage. Patient assistance programs may also help individuals cover the cost of non-covered services or prescriptions.

- Education, Community, and Peer Support: Additional support programs may also benefit women facing the challenges associated with menopause. While standalone programs are beginning to expand, support may already be available to employees through existing programs such as EAPs or mental health benefits. In addition, organizations such as the Menopause Education Center focus entirely on educating employers and their workforce and helping organizations build a workplace-friendly menopause strategy. Efforts should also focus on reducing stigma around menopause and training front-line managers on when to direct employees to designated resources.

As employers have invested heavily in fertility and family-building benefits, menopause is emerging as the next frontier in women’s health equity. While the adoption of menopause-focused benefits is still in its early stages, the expansion of these programs is expected to accelerate rapidly.

Employers evaluating menopause benefits should take several steps:

- Audit current benefit offerings (EAP, telehealth, medical coverage, leave programs)

- Identify gaps in clinical and emotional support

- Define a preferred strategy (enhance current offerings or implement a standalone solution)

- Pilot or phase implementation of the preferred solution

- Communicate resources clearly to employees

The first step should be to understand what benefits already exist that support women going through this period of life and communicate those benefits effectively to employees, underlining the employer’s commitment to a holistic benefits program. If additional support is needed, employers should evaluate their broader strategy and work to implement solutions in coordination with preferred partners.

Overall, employers should consider the real impact menopause may have on employees and business operations. Building upon existing benefits offerings can support attraction and retention efforts, strengthen equity and inclusion initiatives, and serve as an important component of a holistic employee benefits strategy.

1Department of Labor workforce demographic data and various studies on menopause-related productivity and absenteeism trends in the workplace.

2Michelle Travis, “The Business Case for Supporting Employees Through Menopause,” Forbes, June 4, 2024.

https://www.forbes.com/sites/michelletravis/2024/06/04/the-business-case-for-supporting-employees-through-menopause/

3Hone Health, “Hone Health Launches Menopause Time Off (MTO).”

https://honehealth.com/edge/hone-health-launches-menopause-time-off-mto/

Implications for Cost, Care Quality, and Employee Engagement

At-home diagnostic testing has shifted from a convenience to a standard part of healthcare delivery. Accelerated by COVID-19 and advances in digital health, home diagnostics now include infectious disease testing, chronic condition monitoring, cancer screening, fertility, and genetics. For employers and plan fiduciaries, the focus is no longer whether these tools will remain relevant, but how to use them effectively to improve outcomes, manage costs, and avoid overutilization.

Evidence shows that evidence-based home tests can increase preventive screening rates, improve chronic disease management, expand access to care, and reduce downstream medical costs. However, poorly managed use can lead to false positives, unnecessary follow-up care, employee anxiety, and increased spending.

This article examines where home diagnostics provide value, where caution is needed, and how employers, carriers, and TPAs should approach coverage and employee engagement.

The Current Landscape

Home diagnostics are not new. Pregnancy tests have been available since the late 1970s, but the COVID-19 pandemic normalized self-testing at scale. In early 2022, more than 40 million U.S. households used government-supplied at-home COVID-19 tests, with approximately one-third of households participating overall (CDC, 2023). Adoption was widespread, and access gaps narrowed across racial and ethnic groups.

Industry forecasts indicate continued growth. A 2025 global diagnostics survey found that more than 60% of experts expect 10% to 25% of diagnostic tests to be performed at home by 2035, with U.S. adoption expected to outpace Europe (Simon-Kucher, 2025). Growth is strongest in chronic disease monitoring, women’s health, infectious disease testing, and cardiovascular screening. Several categories of home diagnostics are already producing measurable results.

Cancer Screening

Mailed fecal immunochemical test (FIT) kits and FIT-DNA tests, such as Cologuard, improve screening adherence compared with office-based colonoscopy programs alone. A large Kaiser Permanente initiative that mailed annual FIT kits more than doubled screening rates, reduced colorectal cancer incidence by approximately 30%, and cut deaths by half while eliminating racial disparities in screening outcomes (Kaiser Permanente Division of Research, 2025). For employers, these outcomes may reduce catastrophic claims, support earlier intervention, and improve workforce health. Coverage of guideline-recommended home screening tests is considered high-value preventive care.

Infectious Disease Testing

At-home COVID-19 tests demonstrated the value of rapid, decentralized diagnostics. Similar models are now emerging for influenza, RSV, and combination respiratory panels. While home antigen tests are generally less sensitive than laboratory PCR testing, their speed and accessibility can improve real-world detection and support faster behavior changes, particularly when paired with telehealth follow-up.

Chronic Disease Monitoring

Home monitoring tools, including blood pressure monitors and continuous glucose monitors (CGMs), are associated with reductions in emergency visits, hospitalizations, and long-term complications for individuals managing hypertension and diabetes. These tools may be most effective for populations with low adherence to treatment plans or preventive care.

However, broad implementation across already compliant populations may increase plan costs without producing meaningful clinical improvement. Employers should evaluate where these tools are likely to generate measurable value rather than assuming universal deployment will reduce spending.

Direct-to-Consumer Genetic and Wellness Testing

Direct-to-consumer genetic tests and wellness panels present mixed value for employer-sponsored health plans. While FDA-authorized genetic health risk tests, including certain 23andMe reports, meet analytical standards, results are probabilistic rather than diagnostic and are often misunderstood without clinical guidance (FDA, 2017; Harvard Health, 2023).

False positives and ambiguous findings can increase employee anxiety and lead to unnecessary follow-up testing. Physicians have also raised concerns that repeated self-testing may contribute to a cycle of anxiety, confirmatory diagnostics, and low-value care (Becker’s Hospital Review, 2024). Without utilization controls and employee education, employer health plans may see higher laboratory and imaging costs rather than savings.

Employer Implications

Self-insured employers should view home diagnostic testing as one component of a broader population health and cost-management strategy. When implemented appropriately, these tools can support higher preventive screening rates, earlier disease detection, improved chronic disease management, and lower hospitalization and late-stage treatment costs.

The key is using employer-specific data to identify gaps in care within the covered population. When gaps exist, employers should encourage evidence-based screening tools that align with established clinical guidelines and produce measurable outcomes. High-value tests should be covered at low or no cost to members, with minimal barriers to follow-up care when additional screenings or diagnostics are required. Employers should also work with carriers, TPAs, and clinical partners to evaluate new opportunities regularly, as innovation in this space is advancing quickly and benefit strategies will need to adapt.

Home diagnostic testing should not be viewed as a fringe benefit or consumer trend. It is becoming part of the healthcare system. When integrated into a disciplined benefits strategy, these tools can improve employee experience and support long-term cost control. Without appropriate oversight, they can also increase unnecessary utilization and spending.

Sources:

– Centers for Disease Control and Prevention (CDC). Use of COVIDTests.gov At-Home Test Kits Among Adults, MMWR, 2023. https://www.cdc.gov/mmwr/volumes/72/wr/mm7201a4.htm

– Simon-Kucher. From Pandemic Spike to Permanent Shift: The Rise of At-Home Diagnostics, 2025. https://www.simon-kucher.com

– Kaiser Permanente Division of Research. Colorectal Cancer Screening Program Doubled Screening Rates and Halved Deaths, 2025. https://divisionofresearch.kaiserpermanente.org

– U.S. Food and Drug Administration (FDA). Information Regarding the OraQuick In-Home HIV Test.

https://www.fda.gov

– U.S. Food and Drug Administration (FDA). FDA Allows Marketing of First Direct-to-Consumer Genetic Health Risk Tests, 2017.

https://www.fda.gov/news-events/press-announcements/fda-allows-marketing-first-direct-consumer-tests-provide-genetic-risk-information-certain

– Wang et al. Trends in Continuous Glucose Monitor Use Among Adults With Diabetes, Journal of General Internal Medicine, 2024/2025.

– UW Medicine / JAMA Network Open. Steady Glucose Monitor Use Helps Blood Sugar Control, 2025.

https://newsroom.uw.edu

– Cappuccio et al. Blood Pressure Control by Home Monitoring: Meta-Analysis of Randomized Trials, BMJ.

https://www.bmj.com

– Harvard Health Publishing. At-Home Tests: Help or Hindrance?, 2023.

https://www.health.harvard.edu

– Becker’s Hospital Review. At-Home Tests Are Booming, but Physicians Have Concerns, 2024.

https://www.beckershospitalreview.com

– Deloitte Insights. The Diagnostics Industry of Tomorrow, 2023.

https://www2.deloitte.com/us/en/insights/industry/health-care/future-of-diagnostics.html

The Rise of Digital Payments

When a disability or paid leave claim is filed, it is rarely just an administrative transaction. It typically coincides with a moment of personal disruption, such as an illness, injury, parental bonding, caregiving event, or recovery period that temporarily removes an employee from work. In those moments, the timely delivery of income replacement benefits can be critical to financial stability, recovery, and trust in the system.

Expectations around how paid benefits are delivered are changing quickly. While job protection programs and unpaid leave often center on compliance and eligibility, income replacement programs introduce a different set of expectations. For disability insurance, paid family and medical leave, and other employer-sponsored wage replacement benefits, speed, certainty, and convenience are no longer viewed as enhancements. They are fundamental to the claimant experience.

As employees grow accustomed to real-time financial tools in their daily lives, traditional check-based processes and delayed disbursements can feel increasingly out of step with the purpose of paid leave and disability coverage. When benefits are intended to replace wages, delays can weaken the financial security these programs are designed to provide.

Digital disbursement options, such as direct bank transfers (ACH), push-to-card payments, and digital wallets, allow insurers to deliver funds within minutes. This shift reflects broader industry movement toward faster, more connected payment ecosystems.¹ This is not just about technical efficiency; it is about empathy. Research shows that 83 percent of consumers would consider switching carriers after a poor claims experience, reinforcing how central the payment moment has become to trust and retention.³

How it Impacts Employers

For employers, the modernization of claim payments is a critical component of workforce stability and administrative efficiency. When an employee is dealing with a claim, whether it is for workers’ compensation, disability, or personal property loss, their focus is split between recovery and financial obligations.

- Employee Financial Wellness: Delayed payments create unnecessary stress for employees. Faster access to funds allows them to settle medical bills or repair essential property sooner, helping them return to productive routines more quickly.

- Reduced HR Burden: Modern payment systems provide automated notifications and transparency. This significantly reduces the time HR and benefits teams spend acting as intermediaries or answering “Where is my check?” inquiries.

- Operational Resilience: During large-scale events or natural disasters, traditional mail can be disrupted for weeks. Digital payments ensure that benefits reach employees regardless of location or the state of local infrastructure.

What should Employers Do

Modernizing payment infrastructure should be viewed as an essential business strategy rather than a simple technology project. Broader financial system evolution is accelerating expectations for speed, connectivity, and flexibility across how money moves.²

To position your organization for success, consider the following steps:

- Adopt Digital Payment Technologies: Carriers should proactively embrace modern digital payment solutions—such as push‑to‑debit, real‑time payments (RTP), and other instant disbursement methods—by embedding these capabilities into their claims and payment workflows to improve speed, accuracy, and experience.

- Assess Carrier Payment Capabilities: When reviewing insurance partners, encourage employers to discuss and explore the payment capabilities currently available, including instant options such as push‑to‑debit or real‑time payments (RTP), in addition to standard ACH.

- Ensure Integration Readiness: Employers should confirm their HR and payroll systems can readily integrate with carrier claims and payment platforms—such as supporting API connectivity or standardized data feeds—so they can seamlessly receive claim and payment information once carriers deploy modern digital payment solutions.

- Educate Claimants Early: Set expectations by highlighting available digital payment options during claim intake and, where possible, in advance of filing a claim. Encouraging employees to select payment preferences early helps ensure timely, smooth delivery once benefits are approved.

- Prioritize Advanced Security: All stakeholders should work with IT and compliance teams to ensure platforms are protected by state‑of‑the‑art cybersecurity controls—such as strong encryption, multi‑factor authentication, and continuous monitoring—to safeguard employee financial data.

At its core, a claim is not just a reimbursement event. It is a test of how well an organization supports someone during disruption, where speed, clarity, and ease can either stabilize or intensify the experience.

The market is moving clearly toward faster, more connected, and expectation-driven payment ecosystems, while tolerance for delays and friction continues to decline. What was once an administrative step has become a defining moment in the customer relationship.

As a result, employers and carriers that modernize disbursement capabilities are not just improving efficiency. They are aligning with where the industry is heading and meeting expectations that are quickly becoming standard. In this environment, fast, reliable access to funds is no longer a differentiator. It is a baseline expectation and a reflection of trust, responsiveness, and credibility.

1One Inc. 12 Insurance and Payments Trends Shaping 2025.

https://www.oneinc.com/resources/blog/12-insurance-and-payments-trends-shaping-2025

2PYMNTS. Banks Hire Chain Jugglers to Drive Cross-Chain Financial Services.

https://www.pymnts.com/blockchain/2026/banks-hire-chain-jugglers-to-drive-cross-chain-financial-services/

3InvoiceCloud. InvoiceCloud Research: 83% of Consumers Surveyed Would Switch Insurance Carriers After a Poor Claims Experience.

https://invoicecloud.net/press-room/invoicecloud-research-83-of-consumers-surveyed-would-switch-insurance-carriers-after-a-poor-claims-experience

Overview

The medical stop-loss market is experiencing significant upheaval as claim frequency and severity reach unprecedented levels. These developments have fundamentally altered the pricing landscape, with carriers adjusting their strategies in response to deteriorating loss ratios and mounting claim costs.

Rising Claims: Frequency and Severity

In 2025, claims well exceeded target loss ratios. The surge in stop-loss claims reflects broader trends in the healthcare market. Three primary factors are driving this increase: rising costs per medical service, higher incidence rates of severe diagnoses, and the introduction of expensive new treatments, drugs, and therapies. While these developments were anticipated given long-term healthcare cost trends, the magnitude and pace of change have exceeded many projections.

Cancer remains the dominant driver of stop-loss claims across the market, leading in both claimant count and total claim dollars. Cardiovascular conditions typically rank second, while newborn complications have emerged as a significant contributor, particularly for claims exceeding $1 million. Although cell and gene therapies have not yet been major contributors to historical claims, they represent a growing risk. The proliferation of these therapies is expected to further exacerbate both the frequency and severity of large claims in the coming years.

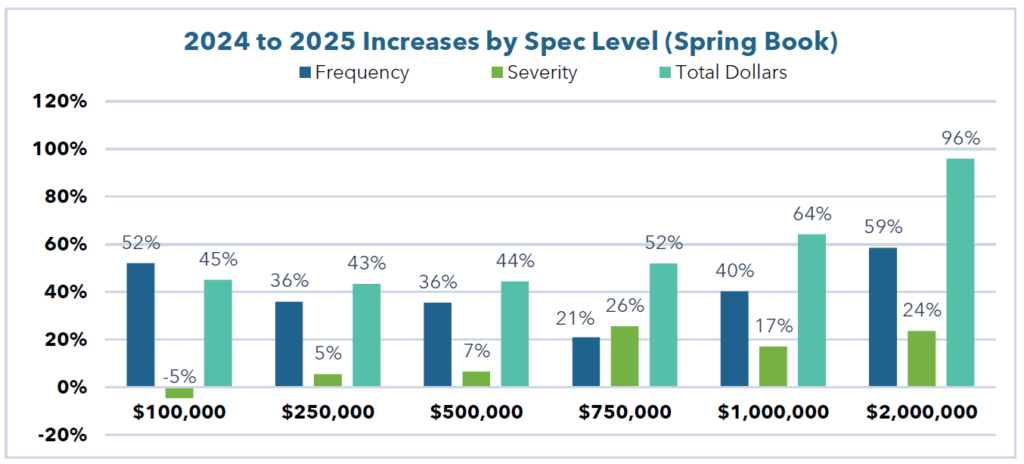

Reviewing data across our book of business and the broader industry reveals a significant acceleration in large-claim frequency across multiple threshold levels:

Claims exceeding $250,000 have grown substantially across the industry. Voya reported an 11% increase from 2023 to 20241. Spring’s internal data shows a more dramatic trajectory, with a 27% frequency increase from 2023 to 2024, followed by a 36% jump from 2024 to 2025 (a 72% cumulative increase from 2023 to 2025). In addition to increased frequency, severity rose by 21% on a per-claimant basis from 2023 to 2025, with total claim dollars for claims exceeding $250,000 increasing by 108% on a PEPM basis.

For claims above $500,000, the trend is equally concerning. TMHCC reported a 113% frequency increase from 2021 to 2024, including a 35% increase from 2023 to 2024 alone2. Internal data reflects a 95% increase in frequency from 2023 to 2025 (36% from 2024 to 2025), coupled with a 29% increase in per-claimant severity over the same period (7% from 2024 to 2025). As a result, total claim dollars exceeding $500,000 surged by 152% from 2023 to 2025 (44% from 2024 to 2025).

At the $750,000 threshold, Voya documented a 15% frequency increase from 2023 to 20241. Internal analysis shows a 21% frequency increase from 2024 to 2025, along with a 26% severity increase over the same period. Total claim dollars above $750,000 rose by 52% from 2024 to 2025. Comparing 2023 to 2025, frequency increased by 115%, per-claimant severity increased by 45%, and total claim dollars increased by 190%.

Million-dollar claims present perhaps the most striking picture. Sun Life reported a 61% increase in frequency from 2021 to 2024, including a 29% increase from 2023 to 20243. TMHCC reported a 113% frequency increase from 2021 to 2024, with a 35% rise from 2023 to 20242. QBE documented a 49% increase from 2021 to 2024 and a 32% increase from 2023 to 20244. From 2022 to 2025, Spring’s internal data shows a 131% increase in frequency. Total claim dollars exceeding $1 million have increased by over 200% from 2023 to 2025.

At the highest threshold of $2 million, TMHCC reported frequency increases of 105% from 2021 to 2024, 65% from 2022 to 2024, and 22% from 2023 to 20242. Internal data shows a 59% frequency increase from 2024 to 2025 and a 162% increase from 2022 to 2025. Total claim dollars on claims over $2M have increased 96% from 2024 to 2025.

Impact of Pharmacy Claims

Pharmacy claims have steadily increased as a percentage of total claims over the past several years, both for underlying medical claims and stop-loss claims. Across one client block, we have seen pharmacy’s share of claims for stop-loss claimants more than double from 2019 to 2025 (from under 15% of claims to 30%). This underscores the growing role of pharmacy costs not only in aggregate claim spend, but specifically among high-cost stop-loss claimants.

Carrier Loss Ratio Deterioration

The surge in claims has materially impacted carrier profitability. Many major carriers reported higher loss ratios in 2024 compared to 2023, including industry leaders such as Cigna and United5,6. Cigna explicitly identified stop-loss as the primary driver of its increased loss ratio, highlighting the outsized impact of this line of business6.

Market Hardening and Premium Increases

The combination of rising claims and deteriorating loss ratios has prompted a fundamental shift in carrier behavior. Double-digit premium increases have become commonplace and are directly attributable to the underlying claim trends. However, the current premium environment reflects more than actuarial updates to projected claims.

The market has entered a hardening phase as carriers shift their strategic focus from growth to profitability. This shift has reduced the competitive pressure that previously constrained premium increases. Carriers are demonstrating less willingness to aggressively price for new business, recognizing that underpricing in the current environment poses unacceptable financial risk.

In their 2025 survey, Aegis reported stop-loss premium increases of 9% to 11%, with long-term premium growth expected to range from 10% to 12%8. These figures likely understate future increases, as 2025 rates were developed using partial 2024 claims data. Continued deterioration in claim experience through 2025 is expected to drive further premium escalation in 2026 and 2027.

This dynamic has created a compounding effect on premiums. Rates are first increasing to reflect higher projected claims and then receiving additional upward pressure as carriers apply less aggressive pricing relative to those projections. The result is a premium environment shaped by both actuarial realities and a strategic recalibration of carrier risk appetite.

The Role of Captive Insurance Companies

Captive insurance companies help employers manage total cost of risk by retaining a portion of medical stop-loss risk in house, allowing organizations to capture risk margin that would otherwise go to the commercial carriers. This becomes increasingly valuable in a hardening market, where carriers embed greater margin into premium rates.

QBE reports increased interest in medical stop-loss captives and notes that captives have delivered great value to employers4. Stealth estimates that captives now represent 10% of the MSL market7. Across our own book of business, we have observed many clients achieve strong results through stop-loss captive structures.

Outlook

The convergence of accelerating claim frequency, rising severity, and market hardening suggests that the current premium environment is likely to persist in the near term. Absent a reversal in underlying healthcare cost trends or the introduction of effective cost-containment measures, employers and plan sponsors should expect continued upward pressure on stop-loss premiums.

The market appears to be in a transitional phase, with carriers recalibrating pricing models to reflect a new reality of elevated claim costs and reduced tolerance for underpricing risk.

1Voya. Stop Loss Paid Claims Analysis 2025. Available at: https://www.voya.com/voya-insights/stop-loss-paid-claims-analysis-2025

2TMHCC. 2025 Annual Report. Available at: https://www.tmhcc.com/en-us/-/media/project/tokio-marine/tmhcc-us/documents/2025-annual-report.pdf

3Sun Life. Medical Stop Loss Market Report. Available at: https://sunlife.showpad.com/share/O4RCCHRh9ke9xod6BdbOz

4QBE. 2025 Accident & Health Market Report. Available at: https://www.qbe.com/media/qbe/north-america/usa/files/accident-health/2025-ah-market-report.pdf

5Becker’s Payer Issues. Payers Ranked by 2024 Medical Loss Ratios. Available at: https://www.beckerspayer.com/payer/payers-ranked-by-2024-medical-loss-ratios/

6The Cigna Group. Fourth Quarter and Full Year 2024 Results. Available at: https://newsroom.thecignagroup.com/2025-01-30-The-Cigna-Group-Reports-Fourth-Quarter-and-Full-Year-2024-Results,-Establishes-2025-Outlook-and-Increases-Dividend

7Stealth Partner Group (Amwins). State of the Market 2025. Available at: https://www.amwins.com/docs/default-source/external-linked-documents/stealth-docs/stealth_sotm_2025.pdf

8Aegis. 2025 Medical Stop-Loss Premium Survey. Available at: https://www.aegisrisk.com/stop-loss-premium-survey

In a recent article published by Captive Intelligence, our SVP, Prabal Lakhanpal, and Senior Consulting Actuary, Nick Frongillo, explain how severe claim frequency and severity in Medical Stop Loss is impacting employers and strategies to respond to deteriorating loss ratios and mounting claim costs. You can find the full article here.

Choosing employee benefits can feel overwhelming. There are more options than ever, rising costs, and constant changes to laws and regulations. The challenge for employers is not offering everything, but rather offering benefits that actually support employees as their lives change, while still making sense for the organization.

Looking at benefits through a life-stage lens can help. Instead of grouping employees by age or job title, this approach focuses on what people need at different points in their lives. It also recognizes that employees don’t move through these stages neatly—someone might be growing their career while caring for a parent or starting a family all at the same time. Benefits should be flexible enough to keep up while balancing cost, compliance, and operational impact.

Early Career and Entry Level Employees

Employees early in their careers are often enrolling in benefits for the first time while also navigating work-life balance and the challenges of a new workplace. While nearly all employers offer health coverage, many younger employees do not fully understand how to use it or what it costs them.

At this stage, affordability and simplicity matter. Employees tend to value preventive care, mental health support, and basic financial tools that help with budgeting, emergency savings, and student loan repayment. Clear education is critical, as communicating benefits is often rated poorly by employees, which directly affects utilization.

Time off also plays an important role. Flexibility to manage personal needs helps early career employees build healthy work habits and reduces the risk of burnout or early turnover in an already competitive labor market.

Employees in the Family Building and Caregiving Stage

As employees progress in their careers, many begin juggling work with caregiving responsibilities. More than one in six U.S. workers provides unpaid care to a family member, and most caregivers report difficulty balancing those responsibilities with their jobs.1

Healthcare and leave benefits become especially important at this stage. Coverage often expands to include partners and dependents, along with increased use of maternity care, fertility services, pediatric care, and postpartum support. Leave programs are critical, and employers face the added challenge of ensuring employer-sponsored leave coordinates appropriately with federal, state, and local mandates.

Without adequate support, employees are more likely to reduce hours, postpone advancement, or leave the workforce altogether. Additional benefits such as dependent care, flexible scheduling, resource navigation, and financial planning support can help employees remain engaged and productive. Manager awareness is also key, since employees often turn to their direct manager first when life events arise.

Mid-Career Employees

Mid-career employees often hold deep institutional knowledge and occupy key leadership or technical roles. Losing them can be expensive, with turnover costs estimated at roughly one-third of an employee’s annual salary, factoring in hiring, training, and lost productivity.2

Benefits at this stage often center on balance and long-term health. Preventive care, screenings, condition management, and strong benefit navigation tools help employees manage growing responsibilities inside and outside of work. Time off remains important, whether for caregiving, family needs, or rest.

Retirement planning also becomes more significant. Access to education and financial guidance can help employees make informed decisions about both their careers and their future financial security.

Employees Entering Late Career and Retirement Planning State

As employees approach retirement, healthcare usage typically increases, and coverage becomes more important than cost alone. Strong provider networks and condition management are common priorities.

Most U.S. workers have access to employer-sponsored retirement plans, but participation often lags behind access, highlighting a need for better education and guidance.3 Financial counseling, retirement readiness programs, and phased retirement options can support smoother transitions while helping employers plan for workforce changes.

What Matters At Any Stage

Some benefits are important regardless of career stage. Flexible work arrangements, family care support, and professional development consistently rank among top workforce priorities.4 Technology also plays a major role: benefits that are difficult to understand or access are less likely to be used effectively.

Ongoing communication is essential. When education occurs only during open enrollment, employees are more likely to feel confused and make rushed decisions. Year-round education in multiple formats improves understanding and utilization.

Making Practical Decisions

Rising healthcare costs and benefit expenses require difficult decisions each year. While most employers view health benefits as a top priority, offering too many options can overwhelm employees and increase costs without improving outcomes.

A life-stage approach helps employers focus on what delivers the most value, regardless of where employees are in their careers. Investing in preventive care, wellness programs, financial education, comprehensive leave offerings, and clear communication can reduce long-term costs and turnover. At the same time, staying compliant remains essential as leave laws and healthcare requirements continue to change.

A benefits strategy built around real-life needs, not just demographics, is more sustainable and more impactful for both employees and employers.

1Caregiver Statistics: Work and Caregiving, Family Caregiver Alliance, https://www.caregiver.org/resource/caregiver-statistics-work-and-caregiving/

2Average Turnover Rate by Industry (2026 Update), Corporate Navigators, https://www.corporatenavigators.com/articles/recruiting-trends/average-turnover-rate-by-industry-in-2024/

3Worker Participation in Employer-Sponsored Pensions, https://www.congress.gov/crs-product/R43439

430+ Employee Benefits Statistics in the U.S. (2024/2025), https://high5test.com/employee-benefits-statistics/

To attract and retain top talent, employers continue to invest heavily in comprehensive employee benefits programs. While offering a wide range of health and well-being options is well-intentioned, an unintended consequence often emerges: choice overload. Employees may appreciate having options, but without the time, expertise, or clarity to evaluate them, navigating benefits can quickly become overwhelming.

This is where care steerage and smart navigation come into play. Together, these strategies are designed to simplify healthcare decision-making, improve the benefits experience, and help employees access high-quality, cost-effective care with greater confidence.

What Is Care Steerage?

Care steerage is a benefit design strategy that guides employees toward higher-quality, more cost-effective providers and care settings based on objective measures, such as quality outcomes, cost efficiency, and an individual’s specific healthcare needs.

Rather than leaving employees to navigate complex provider networks on their own, steerage uses data and structured pathways to support better decisions. At a high level, steerage typically falls into two categories.

Active Steerage

Active steerage involves real-time, personalized support. Employees may interact with nurse navigators, care concierges, or trained benefits coordinators who engage employees by phone, chat, or online portals. These experts help identify appropriate providers based on medical history, new diagnoses, upcoming procedures, and geographic preferences.

Passive Steerage

Passive steerage empowers employees with self-service tools, including online provider directories, mobile apps with cost and quality transparency, and provider and facility comparison tools. By making pricing and quality data more visible, employees are better equipped to make informed choices independently.

Why Steerage Matters

The primary goal of care steerage and smart navigation is to encourage quality-based and cost-conscious healthcare decisions that improve outcomes while reducing unnecessary spending. Many benefit plans reinforce these choices through design features such as tiered provider networks that highlight high-value options, lower copays or out-of-pocket costs for preferred providers, and incentives for using primary care or outpatient settings rather than higher-cost inpatient care.

For employees, this often translates into lower costs, better care experiences, and greater confidence in using their benefits.

Common Features of Smart Navigation Programs

Smart navigation complements care steerage by leveraging technology, often enhanced by AI, to make benefits easier to understand and use. Common design elements include:

- Personalized communications that deliver targeted guidance based on life events, care needs, or upcoming decisions.

- Digital decision-support tools, such as mobile apps and online platforms with cost calculators and provider comparison features tailored to individual and family needs.

- Value-based plan integration, where navigation tools are embedded within Tier 1 or value-based networks that reward employees for choosing high-quality, cost-effective care.

Benefits for Employees and Employers

When smart navigation and care steerage work in tandem, they deliver meaningful benefits for both employees and employers. For employees, these programs help reduce search fatigue and the frustration that often comes with trying to find the right healthcare resources. With access to expert guidance through personal concierge services and decision-support tools, employees are better equipped to make informed healthcare decisions and identify lower-cost providers that still deliver high-quality care.

For employers, this approach can drive stronger returns on investment, help control unnecessary and wasteful claims spending, improve overall benefits engagement, and positively impact employee recruitment and retention, ultimately contributing to a healthier and more satisfied workforce.

Sources:

– Wellness360 Blog, Benefits Navigation: Simplifying Healthcare with Technology, September 2025

– 10 Best Benefits Navigation Platforms for 2026, Recruiters Lineup, October 2025

– Best Employee Benefits Navigation Companies, CBINSIGHTS

What is Nurse Navigation?

A nurse navigator is a registered nurse who guides patients through the often complex healthcare system, coordinating care and serving as an advocate. Navigating healthcare independently can be overwhelming, time-consuming, and costly, particularly for employees managing chronic conditions, complex treatments, or new diagnoses.

Nurse navigation provides personalized, end-to-end support—from diagnosis and treatment planning to recovery—by unifying benefit utilization, provider coordination, and cost-efficient clinical care. This approach ensures employees receive the right care, at the right time, at the right place, while reducing confusion and delays.

Employer adoption is growing rapidly. Currently, 37% of self-insured employers implement a healthcare navigation solution, helping employees access the most appropriate care and resources. ¹

The Role of a Nurse Navigator

Nurse navigators offer a variety of services tailored to patient needs:

Education

- Helps employees understand diagnoses, treatment options, and benefits, bridging gaps in healthcare literacy.

Fast-Tracked Care

- Streamlines the care process by handling prior authorizations, scheduling appointments, coordinating labs and tests, and ensuring all prerequisites are met for timely care.

Advocacy

- Acts as the employee’s primary point of contact and advocate, providing guidance and support throughout the care journey.

Care Logistics

- Assists with travel arrangements (car services, hotels, flights), financial or insurance issues, and access to other support resources.

Emotional Support

- Provides empathy and guidance, offering a trusted relationship for patients and their families to navigate fears, questions, and concerns.

Why Nurse Navigation Matters

Healthcare is increasingly complex, and employees often face multiple challenges when trying to access care. Navigating between multiple providers, understanding specialty networks, and deciphering benefit structures can be confusing and time-consuming. Rising deductibles and out-of-pocket costs add financial stress, while care gaps, particularly for chronic or high-acuity conditions, can lead to delays, complications, and unnecessary expenses.

Nurse navigation addresses these challenges by providing personalized, proactive support throughout the healthcare journey. By coordinating care, assisting with benefit utilization, and guiding employees through complex treatment plans, nurse navigators reduce barriers and ensure employees receive the right care at the right time. Clinical evidence demonstrates the effectiveness of this approach. For example, patients with advanced pancreatic cancer who had access to a nurse navigator had a 104% higher probability of survival after one year compared to those without navigation support. ² Similarly, oncology patients using nurse navigation services reported an increase in satisfaction from 66.5% to 87.4% and a drop in no-show rates from 3.8% to 0.4%. ³

Beyond clinical outcomes, nurse navigation also improves employee engagement and benefits utilization. Employees are more likely to understand their coverage, attend necessary appointments, and make informed care decisions when they have a dedicated resource guiding them. This support not only improves health outcomes but also generates measurable value for employers through reduced unnecessary spending and higher ROI on benefits programs.

Different Models of Nurse Navigation

Employers have several options when implementing nurse navigation:

- Standalone point solution vendors – specialized navigation services that can be added to existing benefits.

- TPA-integrated navigation – larger third-party administrators offer nurse navigation as part of their platform, creating seamless integration with claims, wellness, and leave management.

- Hybrid approaches – combining internal case management with external navigation support to meet the needs of specific employee populations.

Choosing the right model depends on the population served, plan structure, and organizational goals.

How Nurse Navigation Supports Employers

Nurse navigation is more than a benefit perk; it is a strategic tool for addressing key employer challenges. By proactively coordinating care, nurse navigators help manage rising medical costs, increase engagement, and reduce fragmentation in the healthcare system. Employees experience better outcomes and higher satisfaction, while employers benefit from reduced unnecessary spending and improved ROI.

Employers considering nurse navigation should assess their current plan offerings, population needs, and integration options to ensure the solution complements their existing benefits ecosystem without disruption.

As the healthcare landscape becomes more complex, nurse navigation has emerged as an essential solution for modern employers. Providing employees with expert guidance, care coordination, and emotional support reduces barriers to care, improves outcomes, and increases engagement. Whether implemented as a standalone solution or integrated into existing plans, nurse navigation delivers measurable value for both employees and employers.

1State of Healthcare 2024, Employee Benefit News (EBN) National Employer Study, sponsored by Quantum Health, which found 37% of employers are offering healthcare navigation services to support employee access to care. https://www.businesswire.com/news/home/20240410953008

2Cruz, Z. (2025, September 15). Impact of nurse navigation on overall survival and timeliness to care in patients with pancreatic cancer in advanced stages. Journal of Oncology Navigation & Survivorship. https://www.jons-online.com/issues/2025/september-2025-vol-16-no-9/impact-of-nurse-navigation-on-overall-survival-and-timeliness-to-care-in-patients-with-pancreatic-cancer-in-advanced-stages

3Strengthening oncology patient navigation enhances outcomes and access to care. Oncology Nurse Advisor. (2025, May 13). https://www.oncologynurseadvisor.com/reports/strengthening-oncology-patient-navigation-enhances-outcomes-treatment/

When we think of travel, many of us envision picturesque beaches, historical sites, or national parks. For others, travel is driven by healthcare needs, often combining treatment with tourism activities or recovery time. This practice is commonly referred to as medical tourism.

The prevalence of medical tourism is difficult to quantify, but the American Association for Physician Leadership (AAPL) estimates that approximately 1.4 million Americans travel abroad each year for medical care. ¹ For employers, this does not indicate that their health plans are misaligned with benchmarks, nor is it something to control. However, it is a growing reality that benefits from education and proactive navigation. The opportunity is to frame your approach not as cost-cutting, but as an access and risk management consideration. Without thoughtful planning, organizations may face hidden costs, care gaps, and employee dissatisfaction, particularly when complications arise after an employee returns home and seeks care under an employer-sponsored plan.

Why Employees Seek Care Abroad

Employees travel internationally for medical care for a variety of reasons, most commonly for cost and availability. High deductibles, limited coverage, or lack of insurance may prompt individuals to seek care outside the United States. In some cases, international facilities incorporate procedures and recovery into destination-based settings, which may appeal to employees and dependents.

Procedures most often associated with healthcare tourism include cosmetic and reconstructive surgeries, bariatric surgery, fertility treatments, dental procedures, and alternative or experimental therapies.

| Healthcare Tourism vs. Medical Travel Many employers have embraced medical travel leveraging centers of excellence and bundled pricing for domestic medial travel programs. Healthcare tourism is the same fundamental concept but instead of increasing quality and decreasing variability, in many instances the exact opposite happens. Also, healthcare tourism is often initially at the employees’ expense making it difficult to manage in advance of complications. |

Risks for Employer-Sponsored Plans

Because most medical tourism occurs outside of employer-sponsored benefit plans, it typically involves no preauthorization, limited quality vetting, less structured follow-up care, and reduced cost predictability for unplanned complications. While participants generally assume these risks while abroad, employers often absorb downstream impacts once employees return home. These may include postoperative complications such as infections, additional surgeries, extended recovery periods, and related leaves of absence.

One of the most significant challenges is the lack of coordination with domestic providers, including limited sharing of medical records before and after procedures performed abroad. As Renée-Marie Stephano, JD, Chief Executive Officer of Global Healthcare Accreditation, explains,

“When patients arrange medical travel independently, without involving their primary care provider, physicians may be left out of the loop. That makes it difficult to review the treatment plan, ensure it aligns with the patient’s medical history, and properly manage follow-up care once the patient returns home.” ²

Establishing a Philosophy Around Medical Tourism

Rather than implementing rigid policies that aim to discourage or restrict international care, employers may benefit from establishing a philosophy, not a policy, regarding medical tourism. This approach focuses on governance, education, and equity rather than enforcement. Many organizations currently take a passive approach, addressing complications only after employees return home. While this requires minimal oversight, it can result in unintended inequities and inconsistent employee experiences.

In developing a philosophy, employers may consider factors such as equity and access, employee experience, cost transparency, and organizational risk tolerance. Often, the most effective approach involves modeling scenarios across health plans, disability programs, and time-off policies for employees seeking care domestically and internationally. Practical steps may include adding educational resources about risks, clarifying coverage expectations, planning for post-travel care coordination, and aligning leave and disability benefits with health benefits.

Looking Ahead

Medical tourism is expected to continue growing in the coming years. According to Forbes, the global medical tourism market is projected to grow at a compound annual growth rate of about 25.2% through 2030, reflecting rising demand as more individuals combine travel with healthcare services. ³ While medical tourism may not present immediate challenges today, establishing a clear foundation and philosophy now can help employers better manage risk as participation increases.

As with other benefits decisions, employers should apply the same attraction and retention principles when considering medical tourism. Rather than viewing it as a perk to promote, it should be treated as a plan governance consideration. While employers cannot prevent medical tourism, thoughtful planning can help reduce risk, manage complications, and support better outcomes for employees, dependents, and employer-sponsored plans.

1American Association for Physician Leadership (AAPL), medical tourism estimates

2Physician Leadership Journal, “Medical Tourism — Who, What, and Where,” Renée-Marie Stephano, JD

3Forbes, 5 Tips Business Leaders Can Learn From The Rise In Medical Tourism, noting that the global medical tourism market is expected to grow at a CAGR of 25.2% through 2030.