As seen in Captive Insurance Company Reports (CICR)

For most companies today, its people are one of the largest investments its makes. COVID-19 accentuated this point and further showed us how the health of a company depends in large part on the health and wellbeing of its workforce. Providing competitive benefits is not just the right thing to do, but a sound business decision. Employee benefits usually account for one of the largest expense line items on an income statement for organizations. In a world where employee benefits consistently become both more important and more expensive, businesses of all types are looking for an affordable mechanism to finance these risks. One solution that has become central to discussions about employee benefits has been captive insurance.

To provide some background, a captive is an insurance or reinsurance company – which can help insure or reinsure the risks of its owners, the parent company (or companies).

Employee Benefits & Captives

Over the past decade as healthcare and benefit costs have been rising, captives have become the go-to solution for organizations looking to bend the healthcare cost curve as well as create a more efficient employee benefits program. More recently, however, organizations are recognizing the many qualitative advantages of a captive that can help attract and retain employees- a company’s most import asset. As we enter a new decade, these qualitative advantages or “soft costs” of human capital will drive the next iteration of captive insurance.

Traditionally, captives have been viewed as purely a funding mechanism for employee benefits that provides the following advantages:

- Improved cost savings

Cost savings can be yielded through: better control of premium costs, reduced frictional costs (commissions, taxes, insurer profit, administration), captured underwriting savings, earned investment returns, and improved cash flow for the parent organization.

- Improved risk management & increased control

- Enhanced reporting: Captive programs usually provide reporting in a more timely manner, allowing stakeholders to make decisions regarding potential plan design changes for the upcoming year.

- Centralized risk pool: From an organizational risk perspective, leveraging a captive allows risk managers to have a more complete understanding of the risks associated with the programs. Also, life and disability lines are usually considered to be third party risks and have a positive impact on the captive’s risk distribution.

- Non-correlated risk: Employee benefits usually add non-corelated risk for existing captive programs, thereby, reducing the risk exposure to the captive.

- Quantification of loss prevention programs and wellness initiatives: By utilizing a captive, the organization has the ability to implement data analytics programs that provide actionable insights on the effectiveness of existing programs and the current cost drivers.

- Design coverages and provisions for programs that are unique to the parent company: Every organization has a unique set of risks and captives can be used to fill in gaps in the existing benefit programs.

In our view, the next generation of captive insurance will have a sharper focus on the soft costs of human capital, such as:

- Intangible results

While employee benefits account for large costs for employers, they are running a significant risk by not providing the right benefits. By establishing a captive, employers can open doors to focus on human capital and the more qualitative aspects of a program. Further, a captive allows for customized benefits programs to meet the needs of your unique demographic. Employees a technology company will have different priorities and expectations than, for example, those that work in manufacturing. With a captive you can understand and meet those unique needs better than you could with a commercial carrier, in a cost-effective manner. This will go a long way with retention and engagement, and will make your employees feel their voices are heard.

Another intangible result of a captive program is the parent organization’s ability to capture enhanced data analytics. This data comes in months sooner than it would with a commercial carrier, meaning you can analyze your programs and make real-time decisions to yield better claims results. For example, if you know one of your biggest population health issues is diabetes, you can establish programs to address diabetes before your renewal is up. With commercial carriers, the information comes in too late to make changes for that plan year.

Which Benefits Can I Fund Through a Captive?

A wide range of employee benefits may be funded through a captive – the most common coverages are Medical, Life, Disability, Retiree Medical and Voluntary Benefits.

Captives can be used to fund Employee Retirement Income Security Act (ERISA), or non-ERISA benefits. ERISA benefits are primarily the benefit plans sponsored by and contributed to by employers. Life and Disability plans are usually ERISA in nature. These plans are subject to federal oversight, under the auspices of the Department of Labor (DOL) and require express approval from the DOL to fund them in a captive. Approval from the DOL is subject to meeting certain criteria – using an A rated fronting carrier, not paying any more than market rates for the coverages, no direct commissions as part of the contract, requirement for an indemnity contract, to name a few.

Medical stop-loss is usually not considered to be subject to ERISA and has become an extremely popular benefit to add to a captive. The reason for this has been two-fold. Firstly, the rising cost of catastrophic claims. Self-insured organizations are increasingly concerned about the financial impact of high-cost claims – unfortunately seeing $1M or $2M claims is becoming commonplace. One such large claim could have a material impact on the financial sustainability of the program. Second, the hardening insurance market is driving employers of all sizes towards a captive based stop-loss solution, as it reduces the opaqueness of the pricing process and helps employers get a much clearer understanding of their premiums and cost drivers. Usually a captive stop-loss program involves the employer creating an annual aggregate limit, and purchasing excess coverage from the commercial markets above the captive’s aggregate retention. Thereby, protecting the captive from most catastrophic claims.

Long-tail benefits such as group universal life insurance and long-term disability are ideal captive candidates. Benefits that pay out over multiple years (e.g. long-term disability and retiree medical), provide cash flow stability and loss predictability.

Using a captive for voluntary benefits has recently risen in popularity. This is a cost-efficient way of offering benefits that your employees can choose to participate in, or not. More and more employers are turning to this strategy as healthcare becomes more expensive, as a way to supplement benefits and lessen both their financial burden and the financial burden faced by their employees. One of the most attracting elements of writing voluntary benefits into your captive is that voluntary benefits typically have a very low loss ratio, which means they can generate a lot of savings within a captive. Those savings can then be leveraged to reduce premiums for employees or expand the coverage offered. An example of a prime voluntary benefit often offered in a captive structure is hospital indemnity, which can be critically helpful coverage, but one that is often otherwise too expensive to fund.

How it Works

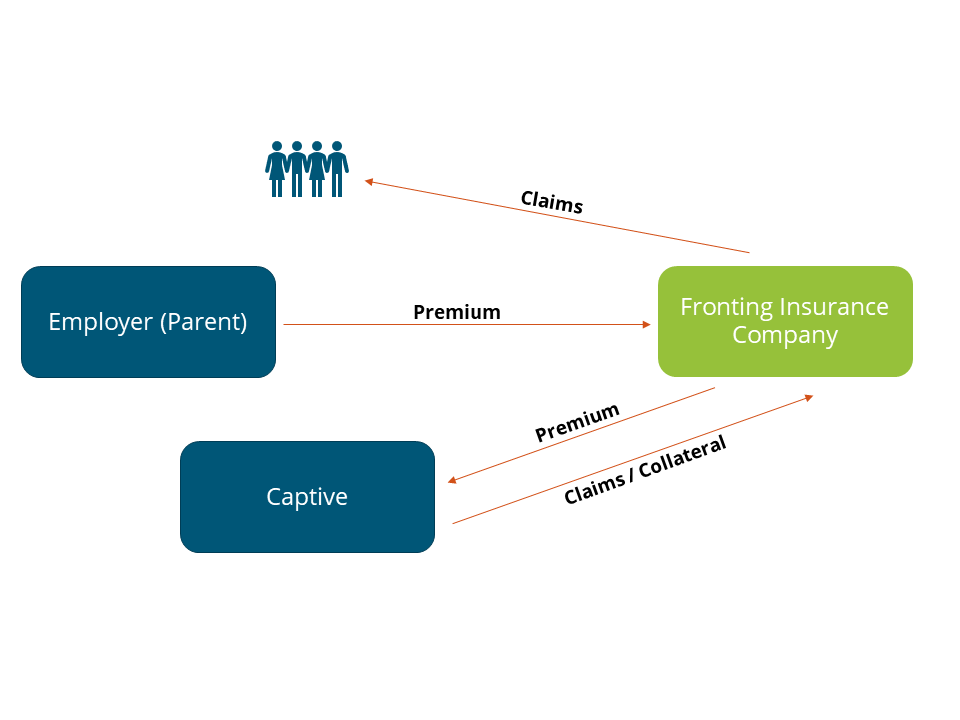

Unlike property and casualty lines of coverage, employee benefit lines have a unique value proposition. They allow organizations to recapture dollars that would have otherwise gone to an insurance carrier. Both life and disability coverages use a fronted carrier, i.e. a commercial carrier stands in front of the captive so that from an employee perspective there is no change in the way they interact with the insurance company. On the back end, the carrier cedes risk and premiums to the captive.

The following illustrates how a typical fronted captive program works.

Under such an arrangement the fronting insurer to continue to administer the program. The employer pays the fronting insurer an annual fee for its services, allowing the captive to retain underwriting profit (if any) from the program. Depending on the risk appetite of the organization and the results of the actuarial modeling – the employer may choose to buy reinsurance for the program.

In Closing

The typical steps involved in adding benefits to an existing captive or forming a new captive are a feasibility study which outlines qualitative and quantitative factors for consideration, such as potential savings, program structures, design alternatives, insurance considerations, and implementation requirements.

Today those in the insurance industry are facing difficult circumstances on a variety of fronts. The recent pandemic has led to hardening of markets. We are seeing substantial rate increases for clients. Captives offer a solution to mitigate these increasing costs in a sustainable manner. In addition, captives provide access to additional data and insights that can help organizations get a clearer understanding of claims drivers and therefore allow for implementation of solutions and tools that reduce claim costs. Further, captives provide organizations the ability to impact the soft costs of human capital by identifying and crafting unique solutions to meet their employees’ needs, more important now as the pandemic shed light on gaps in coverage many did not realize existed.

Captives are useful and versatile risk financing tools, especially for employee benefits. They provide significantly better cash management than can be provided through a trust and can produce impressive cost savings as compared to fully insured guaranteed cost plans.

We hope we’ve piqued your interest and we’re here for you. Over the next months, we will dive further into employee benefits captives to cover things like types of captives, moving to a self-insured program, medical stop-loss, feasibility studies, solutions for small and mid-sized businesses and more. We hope you’ll keep reading.

“Why do I need a broker?” This is a question that surprisingly gets asked more than you would expect. In today’s society of consumerism, the internet, and “do it yourself” mentality, tied with the desire to save money, this is a valid question. I would ask in turn – would you go to court without legal representation? Of course not. It makes financial sense to use a broker as in most cases, you do not get charged for their services. Typically, brokers are paid by the insurance carrier, the one that you jointly decide best meets your needs as an employer. More importantly, brokers protect your best interests as an objective third party. There is no specific financial incentive for brokers to decide on one insurance provider over another.

An insurance broker acts as an intermediary between you and your insurer, lessening the administrative burden for you and negating the need for you to weed through complex policy jargon. We bring over 200 years of training and experience and our insurance know-how, and our goal is to always find a policy that best suits your coverage needs at the best possible price. Brokers do the shopping and analysis on your behalf, saving you the time of plodding through quotes from various carriers and trying to determine the optimal solution. We provide impartial advice based on the client’s unique situation.

Some of the benefits of using an insurance broker are:

- We listen to understand what you are trying to accomplish

- We search the entire marketplace looking for the best coverage at the most affordable price

- Once we find the ideal coverage, we review and discuss the cost, coverages, and exclusions with you in simple language so there are no misunderstandings

- We walk you through the appropriate paperwork and submit it on your behalf to the insurance company

- Once we have approval, we continually assist and advise you throughout the year to ensure you are getting the most from your plan

- We assist with issues like billing and claims questions

- We have compliance experts who will deal with issues like healthcare reform, paid family and medical leave and COVID-19 regulations, ensuring your policies pivot as necessary

- Come renewal time, we are there to negotiate for you and handle much of the legwork involved

These are very important considerations for you to take into account when deciding if a broker is right for you. The alternative is to spend a lot of your own time educating yourself, taking away valuable time from your day job and family. Insurance brokers go through strict educational and licensing requirements and have significant knowledge in the industry. Our deep understanding of your local market and the players involved ultimately yield enhanced, cost-effective coverage for you.

All that said, it’s important to note that not all brokers are the same. Some have specialized services and products or are focused on specific markets. For example, there are brokers with expertise in the property and casualty or life insurance areas but that just dabble in health insurance. Today some payroll companies are even offering employee benefit services as well but again, their bread and butter is payroll, not benefits. To offer an analogy – you would not go to a foot doctor to address a heart condition, so make sure your broker’s core competencies are the ones you need.

In summary, your insurance needs are best met by a broker who works for you and not by an insurance company, who have their own interests to look out for. Brokers yield more choices, usually at a much lower cost to you and your business. Unless you happen to be an expert in insurance plans, why risk the headache and lose the resources needed to do it on your own? Further, a consultative broker like Spring will take the time to truly understand your business so we can constantly be on the lookout for new and innovative solutions that will align with your objectives.

People are typically the largest investment a company makes. Taking care of those people through employee benefits is a niche area of your business, and you need an insurance broker who has the training and expertise necessary in today’s complicated and competitive marketplace. Spring’s approach to brokerage is collaborative and strategic, but we ultimately remove the legwork for you and ensure you have the best plan options available.

In this Rockstars Rocking podcast episode our Senior Vice President, Teri Weber explains how to navigate employee leave through a strategic absence management plan.

Due to COVID-19 we are now experiencing uncharted territory as we approach open enrollment. Check out this article that spotlights some of what we can expect this open enrollment season.

2020 has been a roller coaster of a year so far, and many people are questioning what this means in the world of health insurance moving forward. Check out this recap from BenefitsPRO’s webinar that spotlights steps employers cant take to prepare for an especially daunting enrollment season.

Our Managing Partner and Senior Vice President, Karin Landry and Karen English share their thoughts on how to develop strategic employee benefits plans in an article on HR Tech Outlook. Check out the full piece here.

As the COVID-19 pandemic is affecting more and more organizations worldwide and shifting what employees are seeking in healthcare. Here are 7 predictions we can expect to see in healthcare as the pandemic continues, written by our Managing Partner, Karin Landry.

Check out this episode of Global Captive Podcast, where our Managing Partner, Karin Landry explains what employee benefits need Department of Labor (DoL) approval and what processes and timelines are involved.

As Seen in the Captive Review Group Captive Report

Medical stop-loss coverage protects self-insured groups from catastrophic medical claims. Medical stop-loss has long been used as risk management tool by small- and medium-sized organizations to limit their exposure to medical claims above their desired retention levels. This strategy has been used by single parent programs as well as group captive programs.

The reason this strategy has been more popular in the mid-market is because of two primary reasons. First, businesses have wanted to insulate themselves from catastrophic claims risk, as one large claim could have a material impact on the financial sustainability of the program. Second, the relatively small size of the groups means greater variability from an actuarial perspective. In comparison, large companies have stronger balance sheets allowing them to take on a more aggressive risk management strategy and reduce third party spend with insurers.

As I write this in April of 2020, there are a myriad of unprecedented challenges facing both small and large employers and medical stop-loss can help mitigate some of these concerns. Recently, we have seen a shift in the market where large employers are increasingly becoming interested in reviewing the possibility of leveraging a captive to provide medical stop-loss coverage. I anticipate this trend to continue. Below are four points as to why.

As we stare towards the possibility of a recession and reduced economic output, poor investment income will have an adverse impact on insurance company financials.

Prabal Lakhanpal

- Hardening markets

This past renewal season, we saw that markets are starting to harden, and given the current Covid-19 pandemic and the financial and economic climate, this is bound to continue. A variety of factors have contributed to this including regulatory changes (ACA and healthcare reform) and many recent natural disasters (Hurricane Harvey, California wildfires, etc.). Insurers for a large part of the past decade have benefitted from the favorable financial markets world over, thereby reducing their need to increase rates to continue to make their target earnings per share (EPS).

As we stare towards the possibility of a recession and reduced economic output, poor investment income will have an adverse impact on insurance company financials. Further, as markets tighten, access to inexpensive cash is becoming harder. Since most insurance companies are public, the increased pressure to keep their share prices buoyant is going to result in them wanting to beat their expected EPS – which requires higher profit margins. Finally, as reserves balances diminish due to market conditions, principles of conservatism are going to require them to shore up financials, and the easiest way to do this is by increasing premiums.

These factors coupled with the ongoing pandemic, which will likely result in an increase in aggregate claims, led me to believe hardening insurance markets are upon us. This is likely to result in an increase to reinsurance costs for employers who are currently self-insured. A well-structured medical stop-loss solution can help employers navigate these market conditions by providing them greater control over the program and creating an alternate avenue for reinsurance.

Hardening markets make captives more favorable, as they allow for customized coverage otherwise unavailable in the commercial market. Employers currently using captives have been provided an opportunity to leverage the captive program to fund for Covid-19-related expenses. For non-captive employers, this impact is felt directly on their financial statements.

- Cashflow volatility due to higher claims costs

Claims costs have been increasing at an aggressive pace. The US has long been criticized for poor population health management, with rising chronic conditions like diabetes that are expensive to treat. In addition, the pricey cost of medication has made extremely high cost claims a reality of healthcare. Claims in excess of $1m are becoming commonplace. For large employers, who are traditionally self-insured, such claims cause volatility from a cashflow perspective, making it harder for finance teams to budget and build expected proformas. Using a medical stop-loss program eliminates this volatility as claims above the self-insured retention level are funded in the captive, creating a level funded premium plan.

- Upwards healthcare trend

According to studies by PwC, while medical cost trend has been flat for a couple years, it is expected to increase from 5.7% to 6% in 2020. This rise in healthcare costs is attributable to an increase in the utilization rates. Medical trend increases are outpacing those of inflation, which was 2.07% in 2018 and 1.55% in 2019.

As a result, employers have had to leverage solutions such as high deductible health plans and other forms of cost sharing to bend the healthcare cost curve. The crux of the issue is that now organizations are having to combat both rising medical trends as well as increasing claims costs, while still needing to retain talent and provide competitive benefits.

A well-crafted medical stop-loss solution can help ease the burden for employers and provide them a sustainable way to bend the healthcare cost curve. Development of a formal reserve mechanism is an efficient way for employers to set aside dollars to mitigate large cost increases in the future. While an employer cannot control what happens in the insurance and healthcare markets, they can make the decision to put themselves in a position to be able to navigate the landscape more efficiently. We are seeing an increasing number of CFOs drive conversations around better managing employee benefits spend as it is becoming one of the largest expense items for organizations.

- Control

By writing stop-loss into a captive, an employer can leverage captive savings to focus on initiatives most useful for its employee demographic. We have seen employers use the captive savings for wellbeing initiatives as well as cost control programs focused on disease management for conditions like diabetes or musculoskeletal problems. This kind of structure can then be tied with programs dedicated to population health management, wellness and health advocacy for a robust, employee-first package aimed at gradually reducing claims costs.

Using a captive provides employers access to data in a timely manner, allowing them to better analyze and review drivers of claims, in turn providing them an opportunity to implement measures that would focus on addressing those drivers. While this is possible without a captive, we have seen employers are more engaged when using a captive — meaning they are more likely to create a structured approach to claims and cost management leveraging the captive. In my view, this is because of lack of funds for such initiatives and the lack of a structured risk framework in some cases. Using a captive to underwrite medical stop-loss addresses both of these aspects.

Transparency is one of the core benefits of a captive. Once organizations begin to use a captive funding solution for its medical spend, they usually begin to expand their horizons for other cost reduction initiatives. One such initiative has been carving out drugs (Rx). Using a pharmacy benefit management (PBM) solution can generate additional savings ranging between 15% to 30% of Rx spend. These savings are in addition to those that an employer may recognize by restructuring their funding approach. Further, these savings have a multi layered benefit, reducing the overall medical trend and generating additional reserves for the program to offset possible cost increases in the future.

In general, large employers are more accustomed to customization and retaining control, so a captive program for medical stop-loss aligns with their needs and enhances their ability to control their healthcare programs. Better data analytics and understanding of claims also provides employers the ability to be more reactive and make necessary changes quickly, in a much more agile setup. A captive provides monthly and quarterly reports which are usually much more detailed and timelier than those provided by a commercial insurer. Finally, adding additional risk to the captive also helps the risk managers develop a more comprehensive understanding of enterprise risk at large.

Conclusion

Medical stop-loss coverage in a captive continues to be a prudent business strategy for companies of all types and sizes. It creates multi-layered protection. Large employers are beginning to realize the attractiveness of such a program, whose advantages have been especially highlighted lately due to market and global economic shifts and conditions.