Paid Family and Medical Leave continues to be a confusing point for employers, compounded by new legislation being proposed at a seemingly constant pace. As leaders in the disability and absence management space, we are dedicated to staying on top of updates around PFML, among other areas. After a busy year in that regard, with another on the horizon, we wanted to share this brief overview.

In 2022, there was more movement towards state PFML laws being passed after decreased activity in previous years, largely due to the COVID-19 pandemic. For example:

- Delaware and Maryland both passed laws establishing PFML programs

- Virginia established insurance rules, allowing carriers in the state to provide insured PFML plans to clients

- Colorado and Oregon began collecting contributions on 1/1 and have been working to ensure they are prepared to do so, while establishing other rules for the effective administration of PFML

- New Hampshire worked to develop their voluntary PFML program selecting MetLife as its insurance partner and began coverage on 1/1/2023

- Vermont selected The Hartford as its insurance partner for its voluntary PFML program

- Maine made strides in developing the structure of their state mandated PFML program

In 2023, we expect continued activity. Pennsylvania and Michigan have outstanding proposals for PFML, which will likely be decided upon in 2023, one way or another. Additional states may also put forward proposals in upcoming legislative sessions.

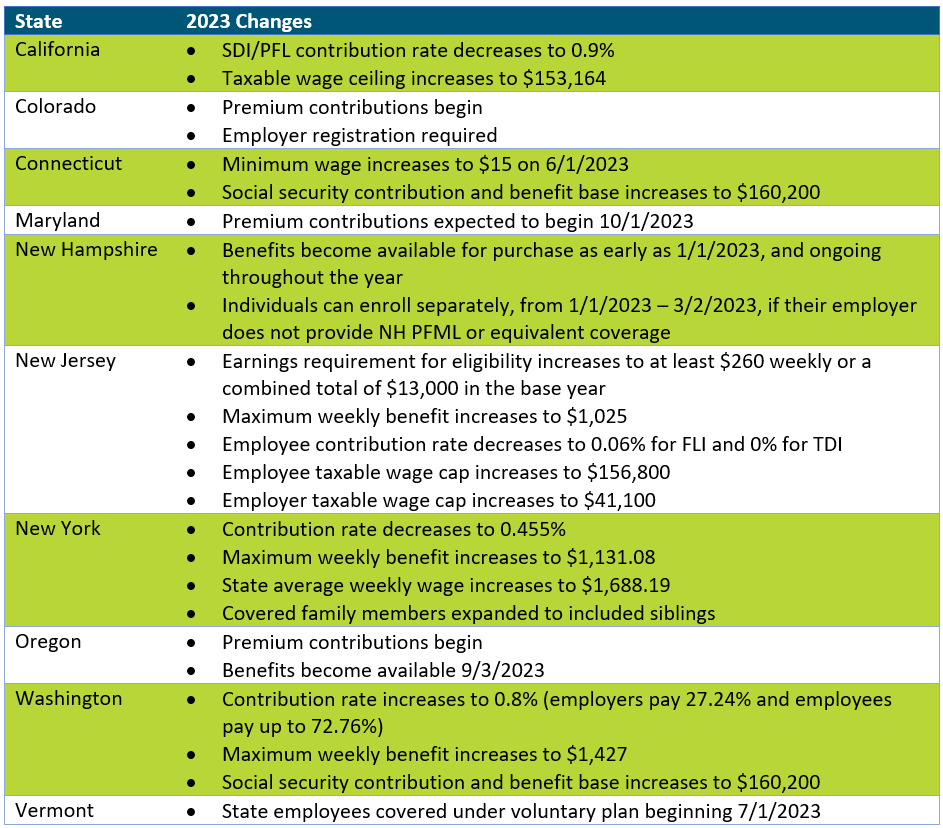

In addition, and as seen in the updates below, states with existing legislation continue to make adjustments to their PFML programs. Adjustments to contributions and benefits are typically expected, most commonly, but not always, at the end of the calendar year.

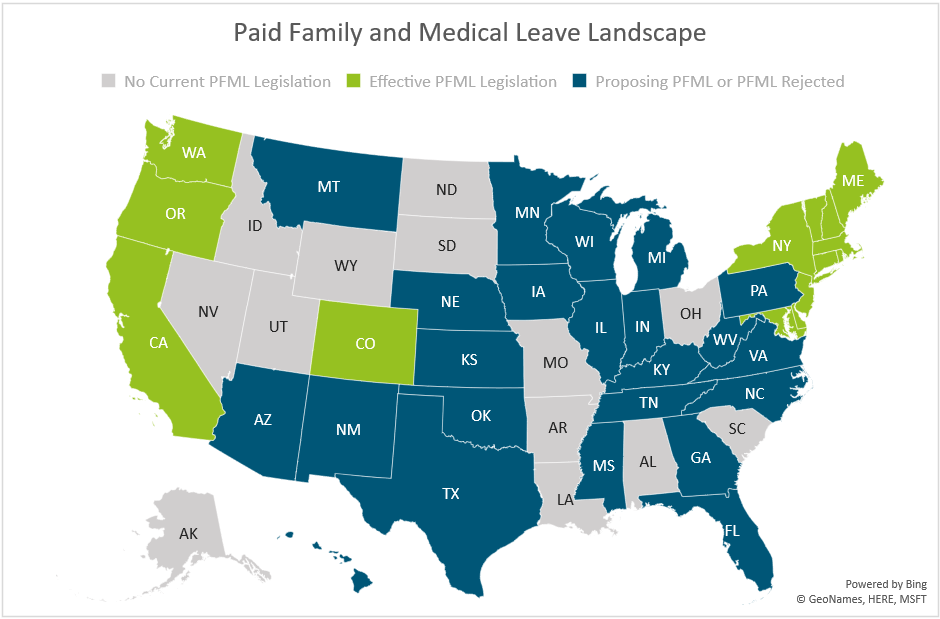

The map below shows a summary of states with existing PFML legislation and programs in place, those who have proposed legislation without it being passed, and those that have not had any activity related to PFML in recent years.

Massachusetts

In 2023, Massachusetts will be updating maximum benefit amounts and reducing total contributions.

The maximum weekly benefit is increasing to $1,129.82, effective 1/1/2023. This is an increase of about $45 from the 2022 weekly maximum. For any employees who may have leave that runs from 2022 into 2023, the weekly benefit that was determined when leave was approved will continue. The new maximum will not be applied until there is a new MA PFML leave application.

Contributions, however, will be reduced in 2023. The total contribution is decreasing from 0.68% to 0.63%, for employers with 25 or more covered individuals. The medical leave contribution will be 0.52%, with employers funding 0.312% and employees responsible for up to 0.208%. The family leave contribution will be 0.11%, with employers able to collect the total contribution from employees. Employers with less than 25 employees are not required to submit the employer portion of premium.

Other State Updates

Other states have made updates to their programs effective January 1, 2023, unless otherwise noted below. Some states may make changes off calendar year (e.g., District of Columbia, Rhode Island), which are not included if they have not yet been released.

Recommended Approach

Employers should review their PFML plans, policies, and processes to confirm they are in line with any legislative changes. To do so, the following checklist can be followed:

– Update employee notices and benefit documentation, as appropriate

While formal notices may not always be required, especially if contributions are decreasing, communicating updates to employees is recommended, especially if the change will impact their pay. Most states provide sample notices that can be customized to fit an employer’s needs. Keep in mind that there may be timing requirements in place (e.g., 30 days in advance).

– Confirm employee count to determine if any changes to contributions are required

Some states require contributions from both employers and employees however do not require employer contributions from “small” employers. This definition of small varies by state (e.g., less than 25, less than 50 employees). Confirming the total number of employees will verify the contributions being remitted to the state are accurate.

– Review private plan strategies based on previous year experience and changes to contributions

Whether or not a private plan is an ideal method for an employer to provide PFML to employees may vary from year to year. This can largely be based on the cost of a private plan versus going with the state plan, but the employee experience also plays a major role. From a cost perspective, a private plan, in most states, will be based on that employer’s leave experience. If an employer has high PFML incidence rates, insurance carriers or TPAs may charge more than is required to be paid under the state plan. From an employee experience perspective, having to file PFML claims to the state and what are often concurrent disability, FMLA or other leave claims to the employer or its vendor partner, can be confusing and require more effort for both employees and employers. While the driving factors will vary by employer, both cost and employee experience should be considered.

– Renew private plans as appropriate

When a private plan is in operation, states may require these be renewed at certain intervals. Massachusetts, for instance, requires this annually, while Connecticut only requires it every three years, unless a material change to the plan is made. Employers should review the timing of their private plan approval and guarantee it is up to date.

If you need assistance ensuring PFML compliance or assessing the optimal plan set up for your organization, Spring’s consultants are happy to help.

Background

On election day, Massachusetts voters were asked to approve or reject four ballot questions when casting their votes for Governor and Attorney General. The 2nd ballot question focused on regulating Dental Insurance, which if passed would “require that a dental insurance carrier meet an annual aggregate medical loss ratio for its covered dental benefit plans of 83 percent1” In layman’s terms, this means dental insurers will have to spend at least 83% of premiums on patient care instead of administrative costs, salaries, profits, overhead, etc. The legislation mandates that if an insurance carrier does not meet that 83% minimum requirement, they will have to issue rebates to their customers. It further allows state regulators to veto unprecedented hikes in premiums and requires that carriers are more transparent with their spending allocation.

Prior to election day, Massachusetts did not have a fixed ratio when it came to dental insurance and will soon be the first state in the nation to have a fixed dental insurance ratio. Although MA requires reporting from dental plans, there were no regulations on premiums. The proposed law sets up a protocol similar to what the Affordable Care Act (ACA) requires of health insurers, where in Massachusetts health insurance carriers must spend at least 85%-88% of premiums on care.

Over 70% of voters voted in favor of regulating dental insurance, the most one-sided response of all four ballot questions. Although at face value regulating dental insurance may seem beneficial for patients, the impacts are not cut-and-dry, and the legislation may affect multiple parties, from consumers to carriers and dentists and practice owners.

Leading up to election day, general reactions about the legislation from dental insurance carriers were negative, while it was supported by most dental practitioners. In fact, the ballot initiative was brought to fruition, in large part, due to an Orthodontist in Somerville. As we can see from the polling results, the general population, or consumers/patients, were also in favor of question #2 passing.

Potential Impacts

For patients: On the intangible side for patients/consumers, the law would provide some peace of mind that the money they pay for their dental insurance was going, in large part, to their care. There is also an indirect advantage to increased transparency, mitigating the typical confusion that surrounds insurance plans and payments. More tangibly, the change could mean that insurers are willing to cover more procedures as a means to hit their minimum requirement (good), however that could result in dental practitioners charging more (not so good).

For employers: We anticipate that the new law will give employers who sponsor a dental insurance benefit plan more control over pricing and protection against unreasonable rate increases. Since many businesses do not offer a dental plan, or offer it on a voluntary basis, the effects should be relatively small. On the other hand, if the law were to create a change in the number of carriers in the marketplace, this could have an impact on plan and network options and negotiating power.

For dental practitioners: With the change, one perspective is that dental practitioners will be able to better focus on the best care for each patient. They may also see an increase in business and revenue if insurers are allocating more dollars towards care and procedures.

For dental insurance carriers: Dental insurers largely opposed question #2 for obvious reasons, such as restrictions on how much they can charge and additional requirements they need to adhere to, but also for less obvious reasons. For example, some carriers argue that the law will require them to make up for profit loss by raising premiums, warning that they could increase by as much as 38% in the state2. They have reason to believe this law will lead to less competition in the dental insurer marketplace, which typically does not benefit the consumer.

Conclusion

Having worked with Massachusetts employers of all sizes on their benefits, including but not limited to dental insurance, as well as interfacing with insurance carriers, being the broker representative for a large percentage of dental offices in the state and working with MDS, we are looking at this update from all angles. Our expertise and decades of experience in this industry enables us to make the following conjectures about passing of ballot question #2:

- Dental insurance premiums may rise, but at a minimal rate

- We ultimately believe this is a step in the right direction as an advocate both for our employer clients and their employees, and that transparency is a positive attribute largely missing from the healthcare experience today

- Immediate impacts will also be minimal, but we may see some of the other factors mentioned above play out over the next few years

If you have specific questions about how the new law might impact your dental plan(s) or practices, please get in touch. In the meantime, you might be interested in watching our recent webinar, “Why Long COVID Needs Short-Term Attention” as you develop your 2023 benefits strategies.

1https://www.sec.state.ma.us/ele/ele22/information-for-voters-22/quest_2.htm

2https://www.wbur.org/news/2022/10/18/massachusetts-ballot-question-2-explainer

It is estimated that ~44 million Americans are experiencing long COVID symptoms. During a recent Spring webinar, our SVP, Teri Weber was joined by a pulmonologist and a representative from Goodpath to review common long COVID symptoms and how it is impacting productivity and claims. You can access the webinar here.

Our Actuarial Team teamed up with Alera Group experts on this COVID-19 and Mental Health Trends whitepaper which looks at the post-pandemic mental health landscape, including impacts on employees, children, plan costs, care gaps, and substance abuse.

In collaboration with Alera Group, our Actuarial Team helped create a whitepaper which provides guidance around eligibility, procedures, and plan costs for coverage of over-the counter COVID-19 tests within health plans, as mandated by President Biden. You can find the full whitepaper here.

Within the last couple of years, we have seen drastic shifts in the wants and needs of employees nationwide. The COVID era sparked and enhanced new practices and benefits that were not popular in the past, such as mental health resources for remote workers, utilizing tech in HR and addressing burnout. Now that COVID effects are less severe and we have returned to more normalcy in many ways, employers must grapple with remote, on-site, and hybrid work models while keeping their workforce happy and engaged. These trends were evident in this year’s Annual Conference hosted by the Northeast Human Resources Association (NEHRA). NEHRA is one of the leading organizations that brings together HR industry professionals to network and share best practices. This year’s conference took place in Newport, RI and Spring had the pleasure of attending and exhibiting.

Here are some of the areas most focused on this year:

1) Adapting to a Hybrid Workforce

Although hybrid and remote work may seem like the norm for many of us, employers are still struggling to keep their workforce connected and satisfied while retaining efficiency. During the peak of the pandemic, many organizations moved to fully remote and are now looking at whether they will require employees to be in the office full-time, part-time, or not at all. Below are some of the sessions that best tackled this issue.

– A session titled “Driving Career Development in a Hybrid World” explored how the adoption of technologies during the pandemic has led to an increase in professional career development tools, but on the other hand, has prevented many employees from showcasing their true talents.

– In the Closing Keynote Panel, three local HR executives from Mersana, Progress and Ocean State Job Lot explained how their organizations have maintained award-winning workplace cultures with a dispersed workforce.

2) Acquiring/Retaining (Next Gen) Talent

As baby boomers are exiting the workforce and Gen Zers are entering, it has caused a great shift in office culture and employee benefits. Gen Z grew up in a technological world with an emphasis on mental health, and often expect their organization to reflect the same standards. Here are a couple of noteworthy sessions related to attracting and retaining next gen talent:

– During “Bridging the Generational Gap through Wellness Initiatives,” a representative from the Town of Barrington, Rhode Island, described how their wellness initiatives have helped increase retention and alleviate burnout among cross-generational employees.

– Experts from Apprentice Learning and FHL Boston explained how organizations can introduce a workplace culture that attracts young people of color in their “Engage Your Employees to Build an Equitable Workforce for the Future” presentation.

3) Reinforcing Employee Wellness

At previous NEHRA conferences and other industry-related events we have seen a giant emphasis on mental health. This year the topic of mental health resources has taken a back seat and many industry leaders chose to focus on the related subject of employee wellness practices instead, spotlighting the importance of…

a) Creating a Culture

Creating a workplace culture with employees of different ages, experiences, locations, and expectations can be a daunting task as an employer. Below are a few of the sessions that provided insights on how to best establish an inclusive company culture.

– National Behavior Health Leader, Dr. Joel Axler discussed signs and symptoms of someone struggling with mental health challenges employers should look out for during his session “Empathy in the Workplace.”

– Roman Music Therapy Services, Meredith Pizzi spotlighted unique ways HR teams can generate workplace cultures that reflect the company’s vision while also inspiring employees.

b) Just Add Joy!

Creating a workplace culture with employees of different ages, experiences, locations, and expectations can be a daunting task as an employer. Below are a few of the sessions that provided insights on how to best establish an inclusive company culture.

– In the Keynote Presentation titled “Create a Workplace People Love – Just add Joy!” the Co-Founder of Menlo Innovations, Rich Sheridan, suggested organizations move away from outdated corporate traditions and adopt new approaches based on what employees want.

– In the breakout session, “What is Stealing Your Joy? Simple Steps to Bring it Back,” attendees had the chance to openly discuss what obstacles are weighing them down at work and possible solutions.

All in all, the conference was a great success and provided an excellent atmosphere for networking and discussing industry trends. Every year I feel like I’m seeing more young talent, which gives me a good feeling about the future of our industry. I am already excited to see what next year’s conference brings!

Spring has been selected to help the Maryland Department of Labor (MDL) more effectively implement and administer the Family and Medical Leave Insurance (FAMLI) Program. Check out the press release here.

Our Senior Vice President, Teri Weber published an article explaining how employers can better gauge the efficiency of their leave management programs and highlight areas for process improvement using the secret shopper model. Check out the full article published by the Disability Management Employer Coalition (DMEC) here.

Pharmacy Benefit Managers (PBMs) serve as intermediaries between insurance companies, pharmacies, and drug manufacturers. Large PBMs are often accredited with securing lower drug costs through volume discounts and aggressive negotiations with manufacturers, which has the potential to make prescription medication more affordable. Unfortunately, many large PBMs lack the transparency that would be required to validate their impact on the cost of prescriptions.

As employers work to find optimal partners, it is important to understand the primary PBM models available in the market and how they align with each employer’s corporate culture. Each model has its own set of pros and cons, so there is not one optimal solution. The key when evaluating is to understand the strengths and weaknesses of the model you are leveraging so you continue to move toward the best approach for your organization and employees. At a high level there are three types of PBM pricing models:

- Traditional Pricing

- Pass Through Pricing

- Hybrid

Traditional Pricing

In Traditional Pricing, also known as spread pricing, PBMs are reimbursed at a higher rate by health plans and self-insured employers than what they are paying manufacturers and pharmacies for the drug. The PBM keeps the difference to offset their administrative costs as well as profit margins. This model is sometimes referred to as spread pricing, which is leveraged by most of the largest PBMs in the market. The model has been highly scrutinized as very little financial data is available and contractual gag clauses often leave insurers and employers with little knowledge of the actual price of the drug. In addition, some prescriptions also have a rebate payment made but only aggregate information is shared, making it impossible for health plans and employers to understand the true cost. With that said, given the buying power of these large PBMs, even with increased spread, employers may still save money within a traditional pricing model.

Pass-Through Transparent Pricing

The Pass-Through Transparent model operates based on the actual costs of the drugs. Clients are billed the amount the PBM is paying the manufacturer and/or pharmacy. All Rx rebates and discounts are passed onto the client. The PBM is compensated not through traditional/spread pricing but through an administrative charge, typically at the prescription level. Although this model seems more economical, PBMs leveraging a pass-through model may not always have the buying power of the traditional pricing PBMs and therefore savings may or may not be realized by health plans or self-insured employers. It is often hard to quantify savings in advance since pharmacy utilization under traditional pricing PBMs are steering utilization to those prescriptions that have the most margin for the PBM in the form of discounts and rebates.

Hybrid

The Hybrid model is a mix between the Traditional Pricing and Pass-Through Transparent models. In this model, rebates and discounts are typically passed to client(s), but it may or may not be in full. Some hybrid models indicate all received rebates are passed back to clients but may have an intermediary that receives some spread that is not disclosed and not considered a rebate. In short, hybrid PBMs have diverse disclosure practices. At a quick glance it may seem more transparent, but it’s difficult to validate.

Solving for the Transparency Issue

With the lack of transparency, some policies at the state and federal level aim to decrease the complexity. For example, most states with transparency laws require reporting from manufacturers when wholesale cost is increased above a certain threshold. The first drug transparency law was passed in 2016 in Vermont, but now over 20 states (including CA, CT, ME, MN, NV, NH, ND, OR, TX, UT, VA, WA, WV) have implemented their own requirements. Maine has one of the more robust approaches, collecting and analyzing the data with the goal of identifying each supply chain’s average net, allowing the public and policymakers to follow the money through the supply chain[1].

The Consolidated Appropriations Act also has requirements for pharmacy reporting that will require PBMs to report on some data that is rarely shared, including but not limited to rebates by drug for the top 25 prescriptions. In some instances, PBMs will share that data with health plans and self-insured employers; in other instances, they will file directly with Centers for Medicare & Medicaid Services (CMS) without employers understanding those plan details.

More recently, on May 24, 2022, the Pharmacy Benefit Manager Transparency Act of 2022 was introduced. Sponsored by Senator Chuck Grassley (IA) and Senator Maria Cantwell (WA), this bill will empower the Federal Trade Commission (FTC) to increase drug pricing transparency and hold PBMs accountable for unfair practices that increase cost. It also will require PBMs to report to the FTC the amount of money they make through spread pricing and pharmacy fees[2].

While we wait to see if the Pharmacy Benefit Manager Transparency Act is passed, other solutions are available. There are companies that are striving to help clients save money when it comes to prescription drug costs. They often run analyses on current employer prescription drug costs to determine how much they could save if they moved away from traditional PBM models.

At edHEALTH, we work hard with our member-owner schools to bend the trend in healthcare costs. Pharmacy continues to be an expensive cost-driver, at a national level, and something we’re addressing head-on. We continuously look for opportunities to bend the trend in healthcare costs, including exploring all options to reduce prescription drug costs.

Tracy Hassett, President and CEO of edHEALTH

When our client, edHEALTH, carved-out prescription drug benefits, the goal was to provide additional savings and transparency to its members. edHEALTH continues to work with their vendors and evaluate various options so that they can offer additional transparency and cost savings. To learn more about potential solutions, talk to your current advisor or reach out to Spring Consulting Group.

[1] https://www.nashp.org/drug-price-transparency-laws-position-states-to-impact-drug-prices/

[2] https://www.natlawreview.com/article/pbms-continue-to-draw-federal-scrutiny-pbm-transparency-act-2022#:~:text=The%20Pharmacy%20Benefit%20Manager%20(PBM,and%20state%20attorneys%20general%20in