Our Chief Property & Casualty Actuary, Peter Johnson, is breaking down the most pressing topics in the captive insurance industry. Stay in the loop here.

A recap of a presentation by Peter Johnson of Spring, Deyna Feng of Cummins, and Melissa Updike of KMRRG at the VCIA 2021 annual conference.

Black Swan Events and Market Capacity

Over the last year and a half, the world as we know it has been flipped on its head. Not only did everyone’s day-to-day processes change completely, but the COVID-19 pandemic also stressed the insurance system significantly and resulted in a number of changes across various lines. “Black Swan” events are those that are unexpected, severe and affect a large number of companies and individuals which is exactly what happened with the COVID-19 pandemic. While the healthcare industry faced increasing premiums and alterations to mental health coverage, the property-casualty (P&C) market also was affected in an unpredictable way.

Rewinding back to prior to March 2020, the P&C market was experiencing an all-time high surplus, and was in a 10-year trend of suppressed rates. Therefore, when the “Black Swan” event of a pandemic hit, insurance companies were forced to significantly reduce capacity to mitigate social inflation and high-cost claim issues. In some cases this drop down insured limits by 75 percent or more of their prior year policy limits. This was evident particularly for cyber liability and umbrella coverage. Additionally, rates across lines were seeing double and triple previous years’ numbers.

On the other hand, some P&C lines actually saw improvement in their combined ratio during 2020. This means that where some lines saw increases in cost, other lines saw a drop in utilization, which “evened out” the overall market. This improvement can be seen in commercial and personal lines auto lines over the last year. The auto industry saw a dramatic downturn in utilization due to reoccurring “Stay at Home” executive orders hindering travel as well as other related changes to the industry.

Needless to say, this all yielded a difficult environment for employees and employers. In order to appropriately mitigate these new or changed risks, companies have been turning to policy exclusions as well as captive financing to better protect themselves and their employees from high-cost claims.

Policy Exclusions and How They Impact Your Business

During the pandemic, no insurance company or insured was truly prepared for the changes that were to come, and many insureds were faced with unexpected coverage exclusions and were left with potentially catastrophic payments. Some examples of policy exclusions include pandemic situations, interrupted business, long-term care, and others. However, employers who had a captive insurance company set up were sometimes safeguarded from policy exclusions, and companies without a captive increasingly flocked to establish one.

To illustrate the advantages, one captive held their policy exclusions to the standard of COVID-19 claims and were able to mitigate those costs through their reinsurance retention. As another example, the Kentuckiana Medical Reciprocal Risk Retention Group (KMRRG), a captive, was able to flip their exclusion around long-term care, a move which, although it was only a small component of their business, significantly minimized costly losses. The framing of this exclusion allows employers to wrap reinsurance around this risk, specifically if they utilize a captive funding vehicle.

Captives offer more flexibility around policy language and terms, which can be adjusted according to the specific risks of the parent company. It is generally the responsibility of the brokers to let their insureds know which reinsurance renewals were at risk during the pandemic. Most commonly these lines were workers compensation, healthcare programs, and other P&C lines, which can be written into a captive or an RRG solution. Note RRG’s cannot write workers’ comp and can only insure liability lines.

Maximizing Captive/RRG Solutions

Captive insurance is not a new concept; however, it is often overlooked as a method for employers to protect themselves against risk. Captives not only better reflect underwriting records but also allow insureds to recoup investment incomes that would normally have been lost to insurance companies.

Captives support the parent company’s risk management overall and provide financial protection and long-term savings, both necessary for any business in ordinary and extraordinary times. Generally, our team sees that, for every $1 of premium that a client converts from a commercial reinsurer to a captive, 10 percent to 40 percent of long-term savings in the form of investment income and underwriting profits are yielded.

A captive can step in to help when commercial market rates are unreasonable, such as the 200 percent to 300 percent rate increases, we have seen recently, which of course are impossible for CFOs to plan for. This happened with many insureds’ umbrella coverage. Many companies over the last 20 months were forced to significantly lower their limits and increase their retention levels simultaneously. With changing premiums (mainly increasing) on top of this reduced market capacity, more and more often companies are utilizing captives to get control over these types of high costs and expand coverage.

Additional benefits of a captive or RRG solution include transparency and improved claims management. For example, if COVID-19 claims do develop, with a captive you can react with a very specific claims management strategy instead of relying on a commercial carrier to do so. This allows you to hand select your partners such as attorneys and other advisors. You can also be sure that your discovery responses are consistent. Additionally, group aggregates have hardened even more in the market which has forced captive managers to become more creative than before. An illustration of that creativity can be seen in the example below.

Hospital Professional Liability in a Captive: Many entities were trying to get their mitigation placed, and by increasing primary levels they were able to provide some protection and increase their claims control.

Bracing for the Future

In order to be properly prepared for the next “Black Swan” event, employers and employees should consider the major lessons learned from the past year:

Risk Diversification

This is not unique to a pandemic situation. When leveraging a captive, it is imperative to have a wide range of exposures. Our actuaries know that, in line with the law of large numbers, the more risks and more exposures, adverse financial outcomes become less likely and more manageable. Considering the correlation between the risks is equally critical as one risk could lead to a domino effect of triggering another high-cost risk. A general rule of thumb for captives is adding low correlating risk to a captive will lead to more stable year-to-year financial results.

Speed to Market

What is your process to quickly adapt to changing market conditions?

Analyze Current Structure

Can you withstand another “black swan” event? What are the coverage improvements that can be made internally?

Financials

What is your cots of risk and risk tolerance? Do you need an improved insurance/reinsurance strategy?

Supply Chain

Has an appropriate strategy been considered?

Other

Do you have uninsured/underinsured risks? Is there sufficient market capacity for your exposure?

If there is a positive we can take from COVID-19, it should be that we learned important lessons and won’t be as blind sighted in the future. Looking ahead, companies should ascertain whether they have the right tools in place to better manage risk and financial losses. In addition to the risk structures and their advantages outlined above, considering cross exposures and diversified risks is the best and easiest way for companies to protect themselves and their employees in the event of another “Black Swan” event. Lastly, having an aggregate view of risks across the organization often leads to creating the most efficient and cost effective risk funding programs.

As seen in the Captive Review Group Captive Report, September 2021.

With the rapid spread of the Delta variant, the Covid-19 pandemic continues to leave employers with a series of unpredictable risks directly related to the pandemic. Among these risks is the potential higher cost of healthcare benefits offered to employees, a factor which must be built into any long-term risk management or cost-containment strategy. Covid-19’s impact on healthcare costs Based on tracking data across multiple employers, the future impact of Covid-19 on high cost claims will directly impact health insurance. Key factors include:

Direct costs related to Covid-19

Costs associated with testing, treatment and vaccines remain a primary source of plan costs. The most direct impact on captives is the high cost treatment tied to severe hospitalizations, particularly due to potent strains of Covid-19 like the Delta variant. There may also be ongoing health needs for members who recover from Covid-19 or are long-haulers.

Deferral of care

Plan members have chosen to defer elective treatments. While some of this care was eventually incurred over the course of the last year, many plan members continue to hold back on care, whether because of discomfort in a hospital setting or difficulty in finding care due to bandwidth issues. This influences future costs, particularly with unpredictable costly surgeries.

Missed preventative care

Client data across industries also showed a significant reduction in preventative care visits, and lower test numbers in areas such as labs, CT scans and MRIs. As a result, many employers are concerned because if certain health issues are not identified and treated early, the severity of the case and corresponding cost of care may be higher down the road.

Behavioral health

Covid-19 propelled behavioral health issues into crisis levels. While it may seem indirectly related to broader healthcare, consider this: the national Alliance on Mental Illness reports that cardiometabolic disease rates are twice as high in adults with serious mental illness, and that depression and anxiety disorders cost the global economy $1 trillion annually in lost productivity. We are sure to see the repercussions of this in claims costs to come.

Health insurer risk premium margins built into insurance pricing have been increasing in light of all this uncertainty, as well as broader trends such increased prevalence of high cost specialty drugs and increasing hospital costs. In fact, the most prevalent specialty medications are increasing in price at 10%-15% annually, further contributing to unpredictability of future claims.

Employer Considerations

During the pandemic, employers have needed to confront their organizational philosophy on the employee value proposition and balancing the investment in employee benefits with the impact on the company’s stakeholders. The impact of Covid-19 has made employers more acutely aware of the need for sufficient healthcare coverage for employees and their families.

In order to provide attractive benefits in an environment of rising costs and volatility, employers must rethink the programs they offer and how they are funded. Many organizations have also revisited benefit program governance structures, how decisions are made, and how programs are monitored.

Perhaps your remote workforce has different needs than they did in 2019, or the pandemic has triggered new problem areas that can be addressed through wellness solutions or advocacy tools.

No matter your path, employers seeking to ensure that they offer comprehensive healthcare benefits to employees at an affordable cost need to consider the financial management benefit of potential long-term cost savings and mitigation of volatility associated with captive structures.

Captive Arrangements for Employee Benefits

As employers look at the impact of the pandemic, organizational planning requires balancing the increasing cost of healthcare with the risk associated with solutions that reduce the total cost of the program. At its simplest form, health insurance can be expensive if a fully insured program is purchased, as organizations pay a risk margin, often 20% to 40%, for transfer of the risk to an insurer. Small to mid-sized organizations typically mitigate this cost by self-insuring a portion of their healthcare risk with medical stop-loss to cover higher cost claims. However, the higher risk premiums required by health insurance, including stop-loss insurance, lead to steep healthcare plan costs and/or, in some cases, being forced to take on higher-than-optimal risk.

A captive arrangement is a strategic way for employers to benefit from self-insurance while creating a sustainable solution to partner with commercial markets. Captives provide substantial competitive advantages over traditional self-insurance, such as:

Reduced total cost of insurance

Insurance carriers develop premiums by heavily weighing on industry averages, state rates and, to some degree, on an employer’s individual loss experience. This may lead to pricing that may not accurately reflect an organization’s actual loss experience. Insurance carriers usually price to include substantial overheads, including risk and profit margins. A captive provides employers an opportunity to recapture premiums from the commercial market and build a sustainable long-term model for their insurance needs.

Insulation from market fluctuations

Conventional commercial insurance is vulnerable to market fluctuations. This has never been more evident than today, with hard insurance markets and premiums that are increasing substantially with almost no change in coverage level. As a member in a captive program, employers are less susceptible to unpredictable rising costs imposed by conventional insurers every renewal season, as a balanced funding approach can smooth the cyclical volatility of the commercial insurance markets.

Protection from cashflow volatility

Leveraging a captive to fund medical stop loss can lower the cashflow volatility often faced by self-insured programs on a monthly basis. Having a captive cover claims at a substantially lower stop-loss level allows employers to smooth out plan funding and mitigate cashflow risk to the company.

For employers that may not have their own captive or the resources to form one, there are a variety of group captive solutions in the medical stop-loss space. These solutions are turnkey in nature and simple to implement. Most well-structured group captive programs aim for a seamless transition for employers where there is almost no disruption. In other words, from an employee’s perspective, the claims process is entirely the same. With group captives in particular, all the mechanical aspects are handled by the group captive management team, with minimal effort required for an employer.

There are several group captive arrangements that employers can tap into. In selecting the most appropriate arrangement, you need to consider factors such as the upfront cost of the program, the extent to which customization will be available, the flexibility you will have for your organization within the group captive model, and how renewals will work.

Looking Beyond the Pandemic

As we look forward beyond the pandemic, employers should consider ongoing healthcare program effectiveness. Healthcare costs will continue to increase and become a larger portion of organizational budgets, but it is not too late to start leveraging innovative solutions to mitigate these costs. You can proactively adjust your tactics today and be better prepared for tomorrow, and with a captive you are truly in the driver’s seat.

Check out Captive.com’s writeup of a panel Spring’s Peter Johnson moderated at the Vermont Captive Insurance Association (VCIA) 2021 Annual Conference.

As seen in Captive Insurance Company Reports (CICR)

For most companies today, its people are one of the largest investments its makes. COVID-19 accentuated this point and further showed us how the health of a company depends in large part on the health and wellbeing of its workforce. Providing competitive benefits is not just the right thing to do, but a sound business decision. Employee benefits usually account for one of the largest expense line items on an income statement for organizations. In a world where employee benefits consistently become both more important and more expensive, businesses of all types are looking for an affordable mechanism to finance these risks. One solution that has become central to discussions about employee benefits has been captive insurance.

To provide some background, a captive is an insurance or reinsurance company – which can help insure or reinsure the risks of its owners, the parent company (or companies).

Employee Benefits & Captives

Over the past decade as healthcare and benefit costs have been rising, captives have become the go-to solution for organizations looking to bend the healthcare cost curve as well as create a more efficient employee benefits program. More recently, however, organizations are recognizing the many qualitative advantages of a captive that can help attract and retain employees- a company’s most import asset. As we enter a new decade, these qualitative advantages or “soft costs” of human capital will drive the next iteration of captive insurance.

Traditionally, captives have been viewed as purely a funding mechanism for employee benefits that provides the following advantages:

- Improved cost savings

Cost savings can be yielded through: better control of premium costs, reduced frictional costs (commissions, taxes, insurer profit, administration), captured underwriting savings, earned investment returns, and improved cash flow for the parent organization.

- Improved risk management & increased control

- Enhanced reporting: Captive programs usually provide reporting in a more timely manner, allowing stakeholders to make decisions regarding potential plan design changes for the upcoming year.

- Centralized risk pool: From an organizational risk perspective, leveraging a captive allows risk managers to have a more complete understanding of the risks associated with the programs. Also, life and disability lines are usually considered to be third party risks and have a positive impact on the captive’s risk distribution.

- Non-correlated risk: Employee benefits usually add non-corelated risk for existing captive programs, thereby, reducing the risk exposure to the captive.

- Quantification of loss prevention programs and wellness initiatives: By utilizing a captive, the organization has the ability to implement data analytics programs that provide actionable insights on the effectiveness of existing programs and the current cost drivers.

- Design coverages and provisions for programs that are unique to the parent company: Every organization has a unique set of risks and captives can be used to fill in gaps in the existing benefit programs.

In our view, the next generation of captive insurance will have a sharper focus on the soft costs of human capital, such as:

- Intangible results

While employee benefits account for large costs for employers, they are running a significant risk by not providing the right benefits. By establishing a captive, employers can open doors to focus on human capital and the more qualitative aspects of a program. Further, a captive allows for customized benefits programs to meet the needs of your unique demographic. Employees a technology company will have different priorities and expectations than, for example, those that work in manufacturing. With a captive you can understand and meet those unique needs better than you could with a commercial carrier, in a cost-effective manner. This will go a long way with retention and engagement, and will make your employees feel their voices are heard.

Another intangible result of a captive program is the parent organization’s ability to capture enhanced data analytics. This data comes in months sooner than it would with a commercial carrier, meaning you can analyze your programs and make real-time decisions to yield better claims results. For example, if you know one of your biggest population health issues is diabetes, you can establish programs to address diabetes before your renewal is up. With commercial carriers, the information comes in too late to make changes for that plan year.

Which Benefits Can I Fund Through a Captive?

A wide range of employee benefits may be funded through a captive – the most common coverages are Medical, Life, Disability, Retiree Medical and Voluntary Benefits.

Captives can be used to fund Employee Retirement Income Security Act (ERISA), or non-ERISA benefits. ERISA benefits are primarily the benefit plans sponsored by and contributed to by employers. Life and Disability plans are usually ERISA in nature. These plans are subject to federal oversight, under the auspices of the Department of Labor (DOL) and require express approval from the DOL to fund them in a captive. Approval from the DOL is subject to meeting certain criteria – using an A rated fronting carrier, not paying any more than market rates for the coverages, no direct commissions as part of the contract, requirement for an indemnity contract, to name a few.

Medical stop-loss is usually not considered to be subject to ERISA and has become an extremely popular benefit to add to a captive. The reason for this has been two-fold. Firstly, the rising cost of catastrophic claims. Self-insured organizations are increasingly concerned about the financial impact of high-cost claims – unfortunately seeing $1M or $2M claims is becoming commonplace. One such large claim could have a material impact on the financial sustainability of the program. Second, the hardening insurance market is driving employers of all sizes towards a captive based stop-loss solution, as it reduces the opaqueness of the pricing process and helps employers get a much clearer understanding of their premiums and cost drivers. Usually a captive stop-loss program involves the employer creating an annual aggregate limit, and purchasing excess coverage from the commercial markets above the captive’s aggregate retention. Thereby, protecting the captive from most catastrophic claims.

Long-tail benefits such as group universal life insurance and long-term disability are ideal captive candidates. Benefits that pay out over multiple years (e.g. long-term disability and retiree medical), provide cash flow stability and loss predictability.

Using a captive for voluntary benefits has recently risen in popularity. This is a cost-efficient way of offering benefits that your employees can choose to participate in, or not. More and more employers are turning to this strategy as healthcare becomes more expensive, as a way to supplement benefits and lessen both their financial burden and the financial burden faced by their employees. One of the most attracting elements of writing voluntary benefits into your captive is that voluntary benefits typically have a very low loss ratio, which means they can generate a lot of savings within a captive. Those savings can then be leveraged to reduce premiums for employees or expand the coverage offered. An example of a prime voluntary benefit often offered in a captive structure is hospital indemnity, which can be critically helpful coverage, but one that is often otherwise too expensive to fund.

How it Works

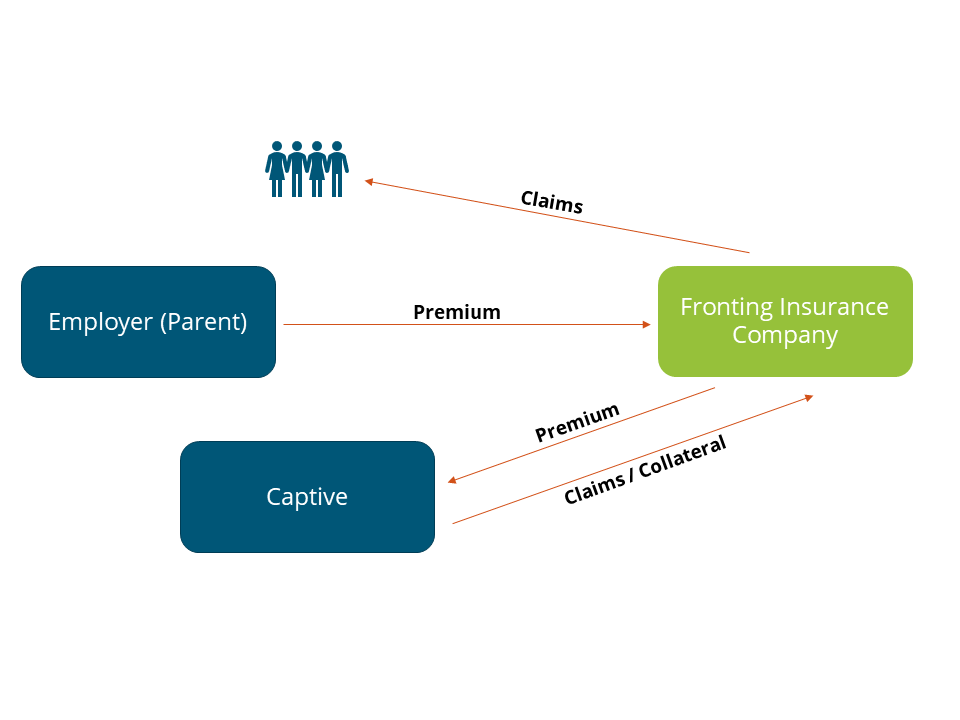

Unlike property and casualty lines of coverage, employee benefit lines have a unique value proposition. They allow organizations to recapture dollars that would have otherwise gone to an insurance carrier. Both life and disability coverages use a fronted carrier, i.e. a commercial carrier stands in front of the captive so that from an employee perspective there is no change in the way they interact with the insurance company. On the back end, the carrier cedes risk and premiums to the captive.

The following illustrates how a typical fronted captive program works.

Under such an arrangement the fronting insurer to continue to administer the program. The employer pays the fronting insurer an annual fee for its services, allowing the captive to retain underwriting profit (if any) from the program. Depending on the risk appetite of the organization and the results of the actuarial modeling – the employer may choose to buy reinsurance for the program.

In Closing

The typical steps involved in adding benefits to an existing captive or forming a new captive are a feasibility study which outlines qualitative and quantitative factors for consideration, such as potential savings, program structures, design alternatives, insurance considerations, and implementation requirements.

Today those in the insurance industry are facing difficult circumstances on a variety of fronts. The recent pandemic has led to hardening of markets. We are seeing substantial rate increases for clients. Captives offer a solution to mitigate these increasing costs in a sustainable manner. In addition, captives provide access to additional data and insights that can help organizations get a clearer understanding of claims drivers and therefore allow for implementation of solutions and tools that reduce claim costs. Further, captives provide organizations the ability to impact the soft costs of human capital by identifying and crafting unique solutions to meet their employees’ needs, more important now as the pandemic shed light on gaps in coverage many did not realize existed.

Captives are useful and versatile risk financing tools, especially for employee benefits. They provide significantly better cash management than can be provided through a trust and can produce impressive cost savings as compared to fully insured guaranteed cost plans.

We hope we’ve piqued your interest and we’re here for you. Over the next months, we will dive further into employee benefits captives to cover things like types of captives, moving to a self-insured program, medical stop-loss, feasibility studies, solutions for small and mid-sized businesses and more. We hope you’ll keep reading.

Spring has been awarded by Employee Benefits Advisor for this Rising Stars 2020 award! Check out the full article here.

Our Senior Consulting Actuary, Peter Johnson has been selected for Business Insurance’s 2019 Break Out Awards! Check out this quick Q&A with Peter that gives insights into his background.

and this is one of the many reasons I love my work. One component of my role is assisting organizations in managing their disability and leave programs, which includes being compliant with the American’s with Disabilities Act (ADA) and Amendments Act (ADAAA). The ADA has pained employers for years due to its regulatory complexity, and although they are making strides and building functional processes to address it, it can sometimes feel like two steps forward and one step back.

I recently conducted a training on the ADA for a large employer team of subject matter experts. After a challenging week of what felt like personal parental fails, I used an analogy that managing your ADA program is a lot like raising a pre-teen! Truth be told, that wasn’t in the script, but it was top of mind at the time and I knew that most of the audience could relate to both parental and ADA struggles.

If you still aren’t convinced of the overlap, I have outlined four challenges with the ADA (that I also experienced with my 12-year-old daughter).

1) Everything must be managed on a case-by-case basis

Organizations must have a prescribed process to identify and manage ADA cases to ensure potential accommodations do not slip through the cracks. However, the regulation is clear in that every case must be reviewed based on its own merit. Employers must consider every request, examine what is needed, and consider solutions that will satisfy the employee’s needs without causing undue hardship to the organization. Key elements of any job must be considered, such as location, essential functions, organizational structure, hardship potential, duration and the like. A simple yes or no is rarely enough. There are often conditions that must be met, including the potential for extensive negotiation, and any decision may be accompanied by resistance from different parties.

At home I also take into consideration things like location, duration, hardship to the family unit and every request must be reviewed on its own merits. Just like with your ADA requests, a yes is always met with delight, but a no will always cause additional work and difficult discussions. That said, that doesn’t mean that you can routinely go the “yes” route just because it’s the path of least resistance.

2) There is a constant demand for “things”

Regardless of whether the request is for Instagram or a sit-stand desk, the requests just keep rolling in! Giving a simple “no” just isn’t going to work. You must engage with your employee (or child) by asking questions, digging into the details, justifying your rationale and following documented policies and regulations (or family rules). Why do they need what they are asking for? Examine both sides of the argument.

With accommodation requests, a simple “yes” is rarely the optimal solution. The key is to really understand what is needed versus what is requested, as there are often gaps in between. The dialogue and documentation need to support what the employee can do and what will ensure they are able to do the essential functions of their job with or without accommodations. Simply approving their request for something may not actually yield a successful solution. Instead as the employer you need to fi nd an accommodation that suits not only the employee but as many stakeholders as appropriate. I recently worked with a client surrounding parking accommodations which were on the rise and extremely challenging given their various office locations and distances to sites. It highlighted how a simple “yes” doesn’t always work. Instead great care needs to be taken with each request and each potential accommodation.

With my daughter it started with an iPod and grew to the iPhone, which has now turned into social media requests. Just saying yes doesn’t work for me – I need to dig in and see what I can provide her that might satisfy her need to fi t in without creating an undue hardship for me. And if I do say yes, you can bet there is going to be a social meeting agreement (similar to an accommodation agreement) to hold us both accountable!

3) Your voice is drowned out by others

Employees requesting an accommodation typically have resources to work with at an organization. They may be working with a disability or workers’ compensation partner, their supervisor, HR, benefits and even occupational health resources. All those voices become noise in the ADA process. Even with the best of intentions, those sources put pressure on the situation that may drown out the voice of the accommodation team. Some parties may be encouraging return to work too aggressively or not aggressively enough. Silence from those resources may be perceived as lack of support the same way that vocalization may be viewed as intimidating. How do you fi nd the right balance?

The key is to manage expectations within the ADA process and bring the stakeholders together by giving them a seat at the table. The interactive process is a very critical part of accommodation reviews; it cannot be avoided in a compliant process. Instead of dreading that part of the process, try to embrace it. Use it to get to the best solution for the employee and the stakeholders and then make a firm decision on what can be implemented.

All parents understand that our children aren’t always listening to us even though we may think every word we utter is critical and wisdom-filled (just like a strong HR professional). Further, what they hear from us may differ from what they hear from their friends, friends’ parents, teachers, or even your spouse. But regardless of the frustration or eyerolls, the ultimate decision related to our children rests with us. They may try to change our minds or tell us all the reasons why other opinions should be valued, but we determine the best solution and do our best to implement it at home.

4) Everything must be managed on a case-by-case basis

An organization cannot be compliant with the ADA, or appropriately manage absence, unless they are dedicated to developing an accommodation program and following through with clear processes and documentation. With that said, it is a long game – a marathon, not as print. Most employees and supervisors will not be singing your praises immediately. At first, they will feel like you are making it “too easy” for employees, or “rewarding” employees who are abusing the system. At the same time employees may think you are “asking too many questions” or “forcing them to pay more money to get paperwork completed.” On any given day all those things may be true, but you are also working to provide a compliant work environment that accommodates employees fairly. You want a solution that returns employees to productive work, processes that are in good faith and interactive and a way that documents what steps were taken and what was agreed to. All of those are beneficial to your organization and to the individual as well.

I was recently working with a client that learned the hard way about documentation. They had a healthcare resource that was given an accommodation around not performing CPR as it was not viewed as an essential function. This employee was transitioned to a new role where CPR was required but the knowledge of her accommodation and lack of ability to perform this function was missed during transition. Unfortunately, this placed an unanticipated strain on the organization, which could have been avoided with greater documentation. Instead, the involved parties were working to solve the immediate need without thinking about the long-term impact on the employee or the organization.

As you focus on return to work and accommodations, try to aim for incremental change toward the most successful program possible, keeping the long-term vision in your view. Start with your policies and procedures, ensuring they reflect the type of program your organization needs. Consider them as living documents that will require revisions as your accommodation program matures. Build an efficient process around those policies, doing your best to move toward that pre-defined,

distant goal post.

At home, incremental change is necessary as well. Do I want a clean room, laundry done, dishes finished and homework perfect? Yes. But I will settle for incremental change toward a successful and productive member of society. This may mean taking things one step (or chore) at a time or placing more focus on the achievements compared to the gaps.

So next time my daughter tells me I am “annoying” and “all the other kids have Instagram” and “I don’t know what it’s like,” I will remind myself that on any given day those things may be true, but I’m trying to raise a healthy, happy kid and building this foundation is necessary to create long-term success. Right now, it’s hard for me to see the goal post but I know it’s there.

Regulation around the ADA is complex, like my pre-teen, but it’s important to remember that it is built on the core premise of avoiding discrimination and pushing employers to do what is right. It sometimes forces a difficult dialogue between employers and employees, but the goal is optimal for both parties.

Whether you’re an office manager, business owner, or a human resource or benefits professional, renewing your company’s health insurance plan may become automatic. Considering alternatives is a daunting task that many feel they lack the bandwidth to handle. However, at a time when healthcare costs are rising, the market is in flux, and employees are expecting more and unique benefits, choosing the most convenient option is probably not your best bet.

It’s imperative to routinely review your package, your results and rethink your strategies to make sure you’re minimizing your costs while giving employees the best coverage at a reasonable rate. You may think you’ve considered everything, but you probably haven’t. Before your renewal date, make sure to address the following questions.

1) Does your medical trend align with market standards?

Before you renew, take a hard look at the medical trend being used this year for next year’s renewal. The market has been seeing downward trends, so you’ll want to make sure you’re seeing that in your rates. For2019, renewals are in the low single digits.

2) If you’re self-insured, have you considered medical stop-loss?

While advantages of self-insurance include flexibility and savings opportunities, self-insured companies are also exposed to an extra level of risk – unexpected, catastrophic loss that they’re expected to cover themselves. Stop-loss insurance, sometimes called catastrophic insurance, can help mitigate this risk. Medical stop-loss is coverage specific to healthcare spend, and involves the establishment of a threshold by the employer over which they have external coverage for.

With an uncertain future for US healthcare, medical stop-loss is something all self-insured organizations should include in their program. Employers will need to consider where the stop-loss program attaches to make sure you don’t over or under purchase coverage. Also, captive stop-loss solutions should be considered to maximize your savings, providing a savings of 10% or more on your stop loss spend.

3) Do you have the right tools in place to support and communicate benefits with your employees?

You may have an impressive health plan and competitive benefits offerings, but if your employees aren’t aware of them, don’t know how to utilize them, or fi nd them irrelevant, you’re not going to see the results you’re hoping for.

It might be time to give these questions some thought:

- How and when are you telling employees about what’s available to them?

- Do they truly understand their options?

- Do you know what benefits your workforce finds most valuable? Are you giving them what they want, or what you think they want? Think about your demographics here.

- Do you have streamlined processes for benefits administration, claims fi ling, etc.?

Consider a formal or informal survey of employees to fi nd out what is working and not working. Further, there are a number of administrative tools, such as Bswift, that you may want to evaluate. For compliance and HR initiatives, ThinkHR and like platforms may be appropriate.

4) Is it time to consider an actuary?

An actuary is a certified professional that measures and predicts insurance risks and premium rates. They are math-based risk experts and can help organizations with insurance policy development, forecasting, valuations, audits, and more.

Most small businesses believe they have no need for actuarial services. However as organizations grow and consider more advanced and varying insurance options, the greater the need for an actuary becomes. While the work of an underwriter is crucial, actuaries take a deeper look at the numbers. They are a neutral third party, and can offer crucial information such as how much volatility you can expect over a one and five-year period. These insights allow you to make smarter insurance decisions.

5) Could your organization benefit from alternative funding strategies?

If you’re fully-insured, have you thought about aiming for a self-funded structure? If you’re self-insured, have you thought about a captive insurance company? If you’re a small businesses, have you thought about an Association Health Plan (AHP)?

We recommend thinking about these alternatives every couple of years. As businesses change and grow, along with market regulations and options, what once made sense for an organization may no longer be the best fi t.

Captives provide unparalleled transparency of and control over an insurance program, which helps with cost savings and customization. Once only an option for jumbo-sized employers, more and more smaller organizations are utilizing a captive structure, either as a standalone captive or part of a cell or group captive.

Further, the AHP market is expanding quickly, due in part to new regulations passed earlier this year. This is a great avenue for a small business to benefit from economies of scale and get the same rates as a large employer. For more information about how to set up or join an AHP, please get in touch.

Healthcare is complicated, but with that complexity comes new and exciting opportunities. Before you decide to maintain the status quo and renew your plan, take some time to think about what’s truly best for your organization and its workforce.