Our VP, TJ Scherer, was quoted in an article from Captive.com, titled “Property Captives Flourish Despite Softening Market”, he explained how the softening P&C market has allowed for more breathing room for employers; you can find the full article here.

Spring Consulting Group, an Alera Group Company, has been shortlisted in Captive Review’s 2025 US Awards in the following categories:

- Actuarial Firm

- Captive Broking Services

- Captive Consultant

- Captive Service Professional

- Emerging Talent

- Employee Benefits Specialist

You can access the full shortlist here.

Spring Consulting Group, An Alera Group Company was listed as a finalist in Business Insurance’s 2025 U.S. Insurance Award Finalists. You can find the full list of finalists here.

Spring Consulting Group is contracted with the State of Maine to conduct actuarial studies of the Maine Paid Family & Medical Leave (PFML) trust fund. You can read the full press release here.

We are excited to announce that our Consultant, Aviel Shalev was named in Captive Review’s 2025 Ones to Watch. You can find the full list here.

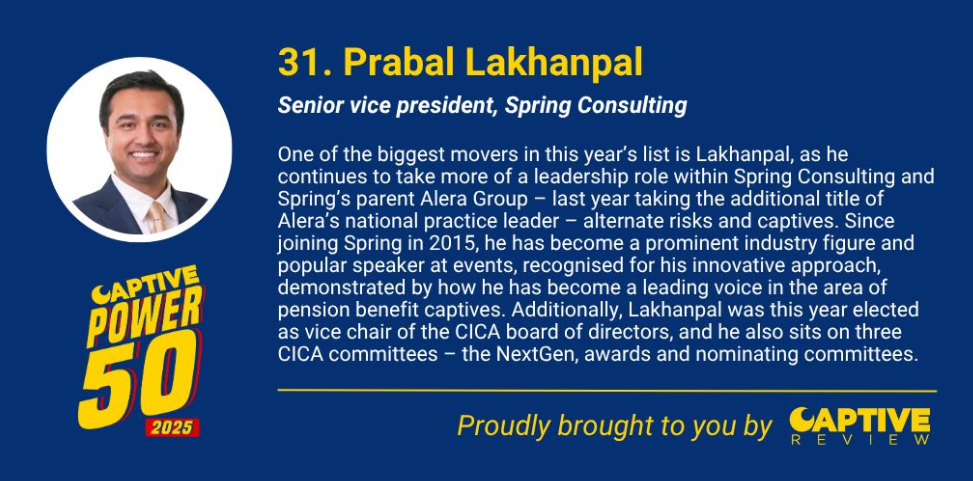

We would like to congratulate all CICA leaders who were recognized in Captive Review’s Power 50, including our SVP, Prabal Lakhanpal. The list spotlights top figures in the captives space, you can read more here.

Every year, Captive Review releases their Power 50 list, which spotlights top professionals in the world of captive insurance. This year our SVP, Prabal Lakhanpal was featured on the list at #31. Check out the full article here.

Our SVP, Prabal Lakhanpal was quoted in an article from Insurance Business on the rise of popularity in captive solutions and how it is shifting market roles. You can find the full article here.

We’re excited to announce that our Analyst, Spencer Towle, was featured in Captive International’s FORTY Under 40 Awards this year! The award spotlights the most influential figures in captive insurance under the age of 40. You can find his winner Q&A responses here.