Coming out of our COVID haze, it can be difficult to remember a time when employers could be truly strategic and proactive without priorities evaporating due to lockdowns, staffing shortages, travel bans or taking a U-turn due to pressures in other areas of the business. The time is now to pivot back to your strategic plans related to employee benefits. We recommend the road to an optimal benefits program be lined with solutions to specific pain points and cultural considerations at your organization. However, I advise at least considering the following within your strategic roadmap to see if they are a fit and can close gaps within your current program.

1) Employee Surveys

Priorities within your workforce have likely changed considerably in the past two to three years. If you haven’t asked employees about their priorities related to employee benefits, it is time! Some of your more traditional benefits or office-affiliated perks that may have been linked to attraction and retention in the past are no longer a value add to employees. It is not enough to talk about perks and flexibility; needs must be better understood to ensure you are providing something that actually attracts and retains talent, instead of the

2) Lifestyle Accounts

Financial accounts within employee benefits are not new (e.g., a Flexible Spending Account), but recently employers have started using these account-based perks in different ways to fill a gap that exists in their offering while providing ultimate flexibility. These accounts are taxable but can be used within the parameters set by the employer. Organizations may use them to support just about anything, but common categories today include:

– Medical procedures that may not be covered within the medical plan (i.e., infertility services, elective procedures, etc.)

– Travel expenses for medical services

– Family-focused benefits (i.e., doula, etc.)

– Legacy wellness support (i.e., fitness equipment, fitness classes)

The beauty of these services is that they can be selected based on employee needs as well as organizational culture and budget.

3) Absence Policies and Processes

Diversity, equity, and inclusion (DEI) are at the top of the list of internal initiatives, and goals are uniquely defined based on how much progress has already been made. It goes without saying that DEI is critical to the success of all companies, but I think a key area of DEI that requires some additional attention is your corporate absence strategy. Over the past few years, organizations have developed additional absence policies around COVID-19 and Monkey Pox, but there has also been a large push toward more family-focused leave of absences surrounding bereavement, parental leave, and the like. It’s important that DEI initiatives within employee benefits focus not only on the services but also on the time off that may be required, and viewing this through the many lenses of your diverse workforce.

4) Oncology Support

As benefits professionals, we have worked diligently to identify point solutions for high-cost and highly disruptive conditions. While point solutions continue to be part of a strong strategy, most employers have or will see an increase in oncology prevalence and spend due, in part, to expensive treatments but primarily driven by disrupted or delayed care and screenings.

Initial concerns with COVID-19 not only decreased primary care visits but snowballed, as providers later had limited appointments available due to overwhelming demand, which has translated into undiagnosed cancers. Now as participants are getting back to their primary care physicians, many cancers have progressed further or upstaged, creating the need for more intense and complex treatment.

In addition to the direct cost of cancer care, employee productivity is significantly less after a cancer diagnosis, even if that diagnosis is within their extended family.

Spring encourages employers to seek a proactive and holistic approach to oncology support, including some or all the following:

– Monitor screening engagement

– Encourage prevention including reminders and other communications; consider incentives

– Educate and support initial and ongoing care decisions

– Concierge support

– Clinical support

Of paramount importance is to educate and engage employees before a diagnosis, so they know where to go for initial support. Those first few weeks after a diagnosis are critical to setting the stage for appropriate treatment and clinical review and/or second opinions. There are some free and buy-up options in the market provided by top-tier cancer care providers/facilities. Those have brand recognition and are designed to provide unbiased support but, in many cases, they also funnel patients to their service centers. Another consideration available is point solutions that are agnostic to cancer care providers/facilities and provide concierge support but do have an add-on charge, typically as a per employee per month (PEPM) or per referral model.

5) Healthcare Disparities

One of the most complex items that should be on your roadmap is to examine what healthcare disparities exist in your population. For starters, ensure multilingual communications are available to close healthcare gaps for those with language barriers. From there, it is important to begin to stratify your population – if your size warrants – and begin to examine if health outcomes are impacted by race, location, earnings, and/or other social determinants of health. This strategic initiative must be performed in collaboration with your insurers and third-party administrators and will take dedicated time to set a methodology and refine your findings over time. The key is to at least get started by looking at the data and talking about how you can improve your understanding of the current state to work toward better data in the future.

Setting the strategic plan for your employee benefit package should be customized to your organization’s priorities and complexities that are identified through claims experience and survey information. Given each organization has its own culture, demographics, and business priorities, it is impossible to set a perfectly standard list of considerations when it comes to your employee benefit strategy. But as you drive toward the best vision for your company – off in the horizon – be sure to stop along the way to check out these five hotspots of benefits planning.

Spring frequently helps employers assess different solutions, plans, and programs and build them into their roadmap. One client, edHEALTH, is currently organizing three solution committees to refine areas of opportunity and prioritize solutions based on demand and change readiness.

A (Brief) VCIA Session Recap

I had the pleasure of speaking at Vermont Captive Insurance Association (VCIA) Annual Conference last week, joined by two colleagues with impressive backgrounds. Jeff Caudill, Director of Risk Management at Haskell and a client of Spring’s, and Mary Ellen Moriarty, Vice President, Property & Casualty at College Insurance Company (EIIA) joined me to discuss different ways that captives can be used to tackle the hard market hurdles we’re currently facing in the insurance industry.

With myself as the moderator and consulting actuary, Jeff representing a brand new single parent captive, and Mary Ellen representing a veteran captive, it was a well-rounded panel that pulled in multiple perspectives.

The Clouds Behind the Hard Market

This visual does a great job at illustrating the many challenging atmospheric effects in the insurance air right now, particularly on the property & casualty (P&C) side of the fence (no pun intended). With Mary Ellen representing the higher education space, we felt it important to highlight unique risks that colleges and universities are grappling with, in addition to the other complicating factors (or clouds) we see here.

In my work I’ve seen that this climate has resulted in increased carrier profitability for certain lines over the last couple of years, such as auto liability, but decreased carrier profitability in others (such as cyber and commercial property).

In higher education, Mary Ellen explained there have been hard market consequences due to underwriter inability to achieve profitability, and as noted in the visual, they are dealing with risks many organizations don’t need to think about, like traumatic brain injuries, the general public accessing the property, and a different kind of medical malpractice. As a result, there are a limited number of carriers willing to provide coverage in this space. As a nod to captive advantages, EIIA was able to grow surplus from their captive prior to the hard market, from 2002 to 2022, which has been extremely helpful in this “stormy environment.”

This success story led us to a discussion around the business case for captives, a snapshot of which you can see here in this video.

Jeff then gave a bit of a play-by-play regarding the process, implementation, timelines and driving forces behind Haskell’s decision to switch from a group captive to a single parent captive (a synopsis of which you can find in this case study).

Looking Ahead

Both Jeff and Mary Ellen described some next steps for their captives, which may include writing in:

- Integrated deductible plans

- Directors & officers

- Cyber

- Employee benefits

- Other P&C lines

Food For Thought

Like most good things in life, you kind of had to be there to get the full experience and maximize your take-aways. So I don’t want to give it all away, but I will leave you with some food for thought that came out of the Q&A for the session. If you want to know the answers, please get in touch!

- With a newer captive that hasn’t had time to build up surplus yet, how do you think about keeping your captive adequately capitalized?

- What are the next coverages or exposures you see on the horizon for higher ed that you would like to add to the captive program?

- What were the key drivers for your CFO to be on board to establish the captive?

- Can you talk about how reviver statutes have impacted obtaining/maintaining abuse coverage?

- As we face uninsured risks like communicable disease, how do you assess the use of the captives together with unique insurance solutions like parametric options? What is the value pitch to the organization?

- What type of coverages perform well in the hard market and why?

- Does forming a captive in a hard market only make financial sense if your company’s loss ratio is below the industry average?

- How do you handle cyber in a captive? Do you have a TPA on retainer?

- Are you using the captive for deductible reimbursement? Do you take any quota share or excess layer risk?

- What does your auto exposure look like and what risk mitigation strategies have you implemented (via the captive or otherwise)?

- How do you market your captive to new members who may not understand captives? Especially in light of the hard market, where captives are especially attractive.

And last but perhaps most importantly:

- What do you think the impact to the insurance market will be if the Browns win more than 2 games this year?

As you can see, we can have some fun in the captive world, and much of it was had at VCIA! Before you leave, check out our captive business case video here, inspired by this presentation.

In this quick video, we outline 6 points that build the business case for captives. Check them out if you are struggling with getting executive buy-in to enter the captive space, or even if you are looking to do more with your existing captive.

We are all feeling the impacts of inflation, and as the word “recession” continues to be a popular one among political, economic and social conversations, we thought we would sit down with our captive insurance experts (Karin Landry, Prabal Lakhanpal and Peter Johnson) to get their two cents on how a possible recession or economic downturn interplays with risk and financial management tactics, with a focus on captives. Here’s what they had to say.

1. What are some possible impacts of a recession on captive insurance companies?

Peter: Changes in risk profiles driven by economic changes (examples include commercial auto frequency moved down then up, cyber ransomware on the rise, healthcare workers’ compensation programs utilized, excess liability/umbrella rates increased substantially, etc.). This also impacted the commercial market and captives often stepped in to fill the gap.

Prabal: Changes in exposure units: a recession may lead to reduction in workforce and therefore a change in insurance spend. On the employee benefits side, during times of uncertainty we typically see an increase in disability claims as well as a spike in usage of health insurance. When taken together with the change in exposure units, benefits programs may see a reduction in performance.

Karin: A continued increase in captive interest. Clients are looking at different ways to save money during a recession. For those organizations that already have captives, risk managers will need to prove the value of the captive, as typically there are a lot of dollars funding reserves that management wants access to in order to improve cash flow during a period like a recession.

2. Are there steps captive owners can take to safeguard their captive against a recession? If so, at what point should they implement them?

Peter: We recommend having service provider and reinsurer relationships in place to be enable the ability to make quick changes and file a captive business plan change to adapt according to the market.

Prabal: For existing captives, we advise undertaking a captive optimization or “refeasibility study” every few years, and this will be especially important if we enter a recession. This process assesses captive performance against original goals, aims to realign the captive according to changes in corporate objectives or priorities, evaluates impacts from recent regulatory changes and/or market trends, considers additional lines, analyzes the domicile, and so forth. Captive optimization helps organizations understand the vulnerabilities of your captive and help you shore them up.

Further, have your actuaries undertake stress testing of the captive to ensure financial stability and consider getting rates as a captive, where appropriate. Then, implement a dividend return policy, which ensures that in the time of need, there is a clear outline of how the parent organization can access any surplus in the captive. Be careful here as you don’t want the parent entity drawing down the surplus so much that the captive loses financial strength.

Karin: Risk managers should determine whether or not their captives are optimally funded. They should calculate the value of the captive to the organization before it becomes a management issue. They should explore other lines of coverage to determine whether or not it will save money, improve investment income, and/or increase cash flow for the organization going forward.

3. How would a recession affect underwriting?

Prabal: Insurance companies have two main revenue streams: 1) underwriting income and 2) investment income. In a recession environment, investment income becomes less likely or harder to come by. Therefore, underwriters are laser-focused on ensuring underwriting income, resulting in tighter underwriting standards. For example:

Peter: Carriers often tighten underwriting standards and may refuse to underwrite certain risks and/or business types all together. We’ve seen this for certain casualty lines like cyber, GL, and excess liability. Carriers may also be forced to remove manual rate discounts and/or increase rates all together while narrowing coverage at the same time.

Karin: Because underwriting practices may tighten, risk managers must understand their organization’s risks better than the marketplace. You could find that your experience is better than the book of business at the carrier level. If this is the case, a captive may make sense.

4. What about reserving?

Peter: To the extent a carrier’s or a captive insurer’s reserves are in a strong position due to favorable experience, reserve releases can be expected and may offset some of the poor 2022 investment experience we’ve experienced. The opposite also holds for exposures with loss trend on the rise that are driving up overall loss costs.

Prabal: Actuarial stress testing of the captive also comes into play here to ensure stability and dividend return strategy so that there is a consistent approach.

Karin: For captives that book discounted reserves, changes in the discount rates will affect the level of reserves captives carry. For those lines of coverage that are sensitive to recessions like workers’ comp and disability, the impact of negative experience should be factored into the reserving process.

5. Could the economic environment cause changes in captive methodology or the lines placed within a captive?

Peter: We’ve seen captive owners become more interested in captive utilization particularly when they feel like carrier coverage and pricing is unjustified based on their own loss experience.

Prabal: Captive optimization helps with optimal capital utilization. In a recession where capital is scarce, companies benefit from being efficient with how they use it.

6. What sort of pressures might captives face during a recession in terms of loan backs or dividends to the parents, or any impacts on capitalization?

Peter: We’ve certainly seen dividend policies put into place for certain clients that have been hit harder during the recession than others. Some have looked to access their captive capital that was built up to significant levels over the years.

Karin: As noted earlier, management may see the reserves of the captives as a pot of money to access; proving the value of the captive negates that issue.

7. The Great Recession around 2008 caused a stall in captive formations. Do we think that could happen again?

Peter: It seems fairly unlikely to have a similar scenario to 2008 since a portion of the collapse was driven by extremely poor mortgage underwriting standards in place. But anything is possible.

Prabal: Further, unlike in 2008, the commercial markets are still in a hard market cycle. This will likely be accentuated in a recession and therefore yield an increase in captive formations.

Karin: Because capital is scarce during a recession, this may spur the use of cell captive programs as opposed to pure captives to meet the needs that risk managers have to control costs and minimize price increases.

8. Anything else related to economic volatility that captive owners and risk managers should keep in mind?

Prabal: One thing would be the potential to free up captive capital by using loss portfolio transfers. The current interest rate environment is likely to create a preferential market for these opportunities.

Karin: Organizations’ hurdle rate might change as a result of the recession. This would necessitate looking at the opportunity costs associated with captives and their reserving process. Additionally, organizations should evaluate their insurance partners to make sure they are sound as they will be grappling with some of the same recession issues noted here. I wouldn’t be surprised if some of the insurers experienced difficulties and either left the marketplace, contracted and changed the coverage levels that they offer, and/or focused in on certain risks while excluding other risks from their policies in accordance with market shifts.

Whether or not we have seen the worst of The Great Resignation, savvy employers are not new to adjusting their benefits and “perks” programs to better align with workforce desires. At the Disability Management Employer Coalition (DMEC) Annual Conference last week in Denver, I spoke specifically on whether Flexible Time Off (FTO) has taken over as the frontrunner, versus the more traditional Paid Time Off (PTO) approach. I thought you might be curious to know the answer, at least in my opinion, so I’m jotting down the key points from my presentation here.

Background

As with so many things in business and in life, in order to clearly understand the current state of PTO, it’s critical to look back at the history of the concept. In 1910, President Taft proposed 2-3 months of required vacation, “in order to continue his work next year with the energy and effectiveness which it ought to have.” Countries like Germany, Sweden, and others were no strangers to this idea, and set forth on setting global standards regarding minimum levels of vacation. Today, the U.S. is one of only six countries in the world – and the only industrialized nation – without a national paid leave policy. So, what gives?

At least on paper, Americans seem to prefer work over vacation. You may be laughing or rolling your eyes, but it is a fact that significant time off goes unused at the end of the year (people choose to lose it rather than use it). In some cases, this may be the result of a corporate culture that, while they may document PTO programs, do not actually encourage the use of that time. If you’re expected to work while on vacation, you may not feel it worthwhile to take said vacation.

PTO

Over the years additional policies popped up to fill some of these gaps, such as leave related to COVID-19, sick leave, disability, parental leave, and family leave. Many organizations arrived at a PTO program in which an allocated number of days account for different types of leave which vary by employer, but might include vacation, bereavement, sick and personal leave. While this creates efficiency and reduces unscheduled absences, this design (perhaps inadvertently) encourages working while sick, as employees do not want to use days within their bucket when they have a cold, since those same days could be used on a tropical vacation or, on a less happy note, in the case of a personal or family emergency. This flaw went from acceptable to unacceptable in light of the pandemic, and turned some organizations off of PTO and on to FTO.

FTO

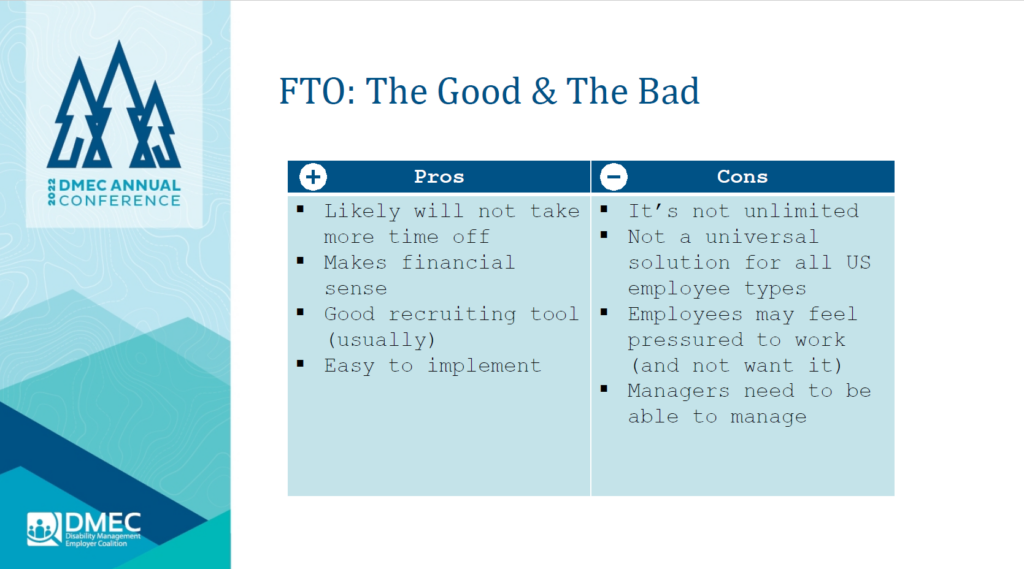

Flexible Time Off (FTO) allows for ultimate flexibility in the volume of “vacation” time taken. With the expectation that employees do their jobs, meet deadlines and achieve their individual and corporate goals, time for rest is scheduled at the discretion of managers. FTO however is not to be confused with unlimited vacation days. While a nice idea, some challenges exist around FTO, including:

- FTO plans are unlikely to meet the needs for vacation plans and sick/safe plans, and are not recommended to fulfill all of these requirements given federal and state law complexities

- Performance management and manager training is critical with this design

- Be careful about creating guidelines around the number of acceptable days off, because it can quickly morph into a PTO plan with wage liability

- Participation in FTO plans for non-exempt employees is not recommended as it will result in payroll obstacles and litigation susceptibility

Given these factors, however, FTO plans can be a powerful organizational tool. If you’re considering FTO, I recommend first answering the following questions:

- Which population should be considered for FTO?

- What approach will ensure managers are managing workload instead of time off?

- What scheduling and approval processes will be implemented?

- How will you ensure employees have the opportunity to leverage their FTO?

- Are you accounting for sick/safe requirements through another policy/program?

- How will you answer to the stigma that FTO is designed to decrease utilization and save you (the employer) from PTO liability?

The Big Reveal

FTO can bring a lot to the table for an organization: it is unlikely to result in more time off (than before), it is financially savvy, a good recruiting tool, and relatively easy to implement. On the flip side, however, I noted some real challenges. In the end, and if you read this article for the clickbait title, my investigative answer is no: FTO is not the new PTO. It should however be considered as one tool within the absence management toolbox, and assessed according to your individual employer needs and priorities.

After a short hiatus, The Disability Management Employer Coalition (DMEC) was able to host their 2022 Annual Conference in-person for the first time since the pandemic started. DMEC is one of the leading organizations in the paid leave industry and their annual conference brings together employers, vendors, government officials, lawyers and more to network and discuss leading trends in the business. This year also marked the 30th anniversary of the creation of DMEC, furthermore solidifying itself as a staple in the world of disability management. It was great seeing so many familiar faces from the industry and learning more about what’s keeping industry professionals up at night. This year’s conference took place in Denver, CO and Spring had the pleasure of both exhibiting and presenting.

Although this year’s conference covered a wide range of topics, I noticed the following three key themes.

1) FMLA & ADA Challenges

Although compliance is often a hot button topic at DMEC, this year there was a specific emphasis on maneuvering around FMLA & ADA challenges. Presenters tackled FMLA & ADA challenges from a range of angles including changes in guidance, a Q&A with federal agency leaders, and a mock trial where the attendees acted as the jury. Some of the of the FMLA & ADA related presentations this year included:

- Helen Applewhaite, Director of the FMLA Division at the Department of Labor (DOL) was interviewed on employer challenges under these laws and key DOL and EEOC priorities in a session titled “A View from the Top: Current FMLA and ADA Challenges”.

- In a session titled “Recent ADA and FMLA Trials: Employer Wins and Losses,” experts included interactive polls where attendees could predict jury outcomes from previous FMLA & ADA trials.

- Lastly, compliance experts from ReedGroup and an Absence Management expert from The Guardian conducted a mock trial titled “Law & Order: DMEC Edition,” where presenters took roles of the judge, plaintiff, defense and plaintiff’s attorneys, and the attendees acted as the jury responding to employers breaking FMLA & ADA regulations.

2) Support for Caregivers and Healthcare Workers

Although COVID has settled a bit in severity, caregivers and healthcare workers are still facing high rates of burnout and overworking, without receiving much federal support. Also, in the past 50 years we have seen the highest rates of children and elderly parents in the home, often requiring some type of care, most often unpaid care by a family member. During this year’s conference, presenters tackled the issue of mental health for employees assuming the role of a caregiver and how employers can offer needed support. Below are some of the groundbreaking presentations tackling this issue.

- Experts from the Lincoln Financial Group explored solutions employers can adopt to support employees who act as caregivers in their “Caring for the Caregivers: A Key to Employee Retention” session.

- The Standard’s Dan Jolivet looked at common stressors healthcare workers face that lead to fatigue and turnover in the healthcare industry and brainstormed possible solutions in his “Costs of Care: The Impact of Stress and Compassion Fatigue on Healthcare Workers” presentation.

3) The Future of Leave

As we tentatively look beyond the COVID-19 era, there was a huge emphasis this year on what we can expect from the disability and leave management industry moving forward. During the pandemic many employers adjusted to remote/hybrid leave policies, introduced new mental health resources and navigated changing COVID regulations. But as we slowly move into a post-COVID world, many speakers, such as those noted below, looked at new-age alternative leave policies and what we can expect for the future of leave.

- Representatives from Unum explained how previous leave programs are not working for today’s workforce and a one-size fits all approach is not suitable for most employees in their “Leave Is Changing: Are You Changing With It?” presentation.

- Spring’s SVP, Teri Weber evaluated whether flexible time off policies could be a viable replacement for traditional PTO policies in her “Is FTO the New PTO?” session.

- Leave specialists from Brown & Brown, FINEOS, New York Life Group Benefit Solutions and Spring looked at “How [Employers Can] Harness Market Forces to Meet Future Absence Management Challenges.” Some of these market forces discussed included Instagram, the gig economy and federal paid leave policies.

a) Utilizing Tech & Data

When looking at the future of leave management, we are seeing a giant increase in leave related tech and software, which allows employers to better understand leave trends and preferences within their workforce. Although tech and data collection software are not new in the industry, we are seeing constant updates and an influx of new software that help measure different facets of absence management policies. Below are a few tech & data related sessions we wanted to spotlight.

- AbsenceSoft’s CSO and CCO showcased how data is key in managing eligibility, entitlement, workflow process and more, as well as common mistakes to avoid when designing a data strategy.

- One panel presented on “Improving the Employee Leave Experience through Technology”, in which they reviewed how tech can expedite the collection of medical documents, identify opportunities for wellness programs and more.

- When it comes to implementing Absence Software, it can be tricky selecting the right program. A discussion including CVS Health and CommonSpirit Health spoke on best practices when selecting and implementing a software-based solution.

b) Moving Past COVID-19

As many organizations slowly move back into the office, employers have been developing and reassessing return-to-work programs and reevaluating leave policies to keep their workforce happy. On a national level, we are seeing changes in COVID-related compliance and a big push to retain talented employees through enhanced benefits packages. Here are some noteworthy sessions related to adjusting to a post-COVID world.

- In a presentation titled “Life Beyond COVID: New Focuses for Absence & Disability Compliance”, representatives from Jackson Lewis review the long-lasting effects of new leave legislation.

- Experts from Voya Financial and FullscopeRMS’s Claims Director, Katie Hunt shared recent research to help enhance leave management and return-to-work programs.

- Another panel including DMEC’s CEO, Terri Rhodes tackled feedback and questions from the audience on challenges for absence management teams, return-to-work programs and ADA accommodation processes.

All in all, being back at the DMEC Annual Conference in-person was a powerful experience! This year I saw so many young and enthusiastic faces which is a good sign for the future of the industry. DMEC never fails to provide innovative insights into the absence and disability management landscape while providing a fun and interactive experience, and I am already looking forward to their next event.

Cell Captive Overview

A protected cell company (PCC) is a legal entity that can be considered as a condo of insurance. A PCC facilitates a turnkey solution for companies by offering clients an individually protected cell that is insulated from the risk of other cells within the PCC; each condo operates as its own captive (with certain restrictions) and does not share risk or rewards with the other condos in the building (PCC). PCCs can vary in type and operational structures. The underlying principle of a PCC is that they are established by a sponsor that funds the capital required by the core. The sponsor is also responsible for ensuring other captives operate within the business plan parameters of the PCC. Clients benefit from a PCC as they spend less time and resources on the operational and establishment activities for the program.

When cell captives were first introduced to the market, they were largely in the form of unincorporated cells, where participation and service provider agreements worked to protect the sponsor’s investment rather than through structural protections.

The model for cell captives has evolved to allow more control for cells with the establishment of incorporated cells. Incorporated cells allow cells to even have their own Board of Directors at the cell level.

Regardless of the type, any cell captive structure allows constituents to benefit from pooled administration, but not from pooled risk, as each cell is independent. Sometimes a company will own multiple cells within the PCC, which are all treated individually.

Cell captives are attractive risk funding vehicles because they offer:

- Easy entry. Cell captives are turnkey and can be established quicker and in a more efficient manner compared to standalone captives.

- Economies of scale. Administrative savings are generated as the costs are pooled across cells.

- Professional captive management. Typically, cell owners can be fairly hands-off with built-in program management.

In addition to being a great solution for small and mid-sized companies, cell captives align with a range of other use cases and can be flexible in structure and purpose, for example:

- A captive owner may want to reform a pure captive into a cell captive to allow different Joint Ventures of the parent company to be insured through cells jointly.

- An organization can use a cell captive to separate higher risk areas of the business, without impacting the rest of the captive. For example, each business unit could head up an individual cell. For instance, an organization may view it advantageous for senior management of each of its subsidiaries to own cells that insure the subsidiaries they manage. In this case, each entity, whose risk profiles may vary greatly, would have its own cell that is run independently but still in favor of the parent organization.

Cell captives were once most commonly leveraged by mid-sized companies entering captive funding for the first time and seeking lower barriers to entry and extra assistance. While still a great fit for mid-sized companies, market conditions are driving more and different types of organizations toward cell captives.

The Surge in Cell Captive Demand

In more recent years, we have increasingly seen large multinational organizations entering the cell captive space, in establishing and owning the entire structure as part of their enterprise risk management strategy. In addition to the basic cell captive advantages listed above, other driving factors that may be of interest include:

- A lower required upfront capital investment, as compared to a standalone captive

- Greater ability to meet different business objectives at once, as well as to adapt

- It is simpler to add a cell to an existing program than it is to set up a new single parent captive for a different line of coverage. On the other hand, it is also relatively easy to “phase out” a cell that was insuring a critical risk two years ago, but that risk or the level of need is no longer there today.

- While all captives offer flexibility over commercial market solutions, cell captives are unique in that each individual cell can be in the form of a reciprocal, a risk retention group (RRG), a limited liability company (LLC), a non-profit, and other types without the need to match each other

- The ability to write third-party risk while leveraging capital and surplus from an additional captive program

Hard insurance market conditions as well as the landscape for emerging risks are making cell captives even more attractive. While often a good fit for more traditional lines, more and more cell captives today are being used for risks like voluntary benefits, cyber insurance, and excess liability. Further, more domiciles have passed cell captive legislation in recent years, opening doors to many.

As with any assessment regarding alternative risk financing, always start with a feasibility study. While cell captives are growing in popularity and advantageous for many, a thorough analysis of the pros, cons, and other contributing factors specific to your organization, its risk and its objectives, is necessary before any decision is made.

A critical starting point in setting up a captive is the captive feasibility study. Captive feasibility studies come in many forms, and there are no industry standard report formats. As a result, many captive owners do not know what to expect as a final deliverable, and we see many feasibility reports that are severely lacking.

The feasibility study forms the cornerstone for the establishment of a captive and is usually one of the first documents that would be requested for in the event of an audit by the IRS.

Every captive actuarial study should include both qualitative and quantitative aspects. Not only should it clearly map out expected financial results, but it should also highlight important insurance considerations that ensure an appropriate and compliant captive structure.

To help provide a framework, here are five key questions that captive owners should be able to answer based on their captive feasibility study.

1. Do you have appropriate data?

As part of the captive feasibility study process, captive owners should work closely with their current insurance carriers to gather as much high-quality data as possible. The study should reflect at least the following for all proposed lines of coverage:

- All Plan Documents or Summary Plan Descriptions

- Current rates, volumes, exposures, and premiums

- At least 6 years’ worth of prior experience reports, which will show paid premiums, constant premiums, paid claims, and reserves by incurred year

- Large claim, premium rate, and plan change histories

This data will be used to develop future loss estimates once the coverage is placed in the captive. All of it should be readily available, and organizations should be reviewing this data regularly, regardless of whether it is undertaking a captive feasibility study.

2. Has an actuary reviewed your loss experience?

Once you’ve gathered the necessary experience data, it is important that an experienced actuary review it. All experience reports are different in layout and content, and an actuary will know best how to interpret the data, develop the best estimate of future losses, and ask the right questions of the carrier. A captive feasibility study should always include a robust actuarial analysis.

A good actuary will ensure that plan changes, rate changes, and overall population changes have been properly reflected in the experience report. If they aren’t, the actuary can make the necessary adjustments.

The actuary should also review the claim reserves that the carrier is reporting. In our experience, carriers typically overstate reserves due to conservative assumptions, inflating the loss ratio. A good actuary will independently calculate reserves to compute a more accurate estimate of historical loss ratios and future losses.

3. Do you have a clear sense for the expected administrative expenses – at the start of the program and ongoing?

Administrative expenses related to operating an employee benefits captive include actuarial, captive management, legal, audit, letter of credit (if used for collateral), carrier fronting fees, premium taxes, captive domicile fees, taxes, and state procurement taxes (if domiciled outside of home state).

These fees play a large role in determining whether the captive will be profitable at fully-insured market rates. If your captive charges rates higher than market rates to turn a profit, then the fees are too high. Carrier fronting fees are typically the largest expense and the most important to get right. Captive owners need to understand how these fees were determined in the captive feasibility study and if they are market competitive and realistic.

We always recommend that a company placing employee benefits in their captive conduct an RFP process to select vendors, and that includes competitive fee arrangements.

4. Is the party that conducted your feasibility study independent, or could there be a conflict of interest?

We have seen many captive feasibility studies completed by non-qualified entities or by organizations that have a vested interest. For instance, many insurance brokers will conduct a high-level analysis to conclude a captive program is not feasible. It is essential to understand the interests of all stakeholders and to work with organizations that have the appropriate credentials to help you make an informed decision.

Find an independent party who can provide an objective, transparent, and unbiased recommendation.

5. Will the coverage qualify as insurance?

Every captive feasibility study must comment in detail on the qualitative aspects of captive insurance including what it means to qualify as insurance. This is an important consideration from a captive owner’s perspective and must be fully understood. There are many case laws that have commented on the lack of understanding of insurance company operations.

For instance, an important aspect of any insurance transaction is that it must achieve risk transfer and risk distribution. There are a few industry-accepted risk transfer tests that will demonstrate that the coverage adequately transfers risk from the insured to the captive. The “10-10 Test” is the most common, determining whether there is a 10% chance of a 10% loss. Alternatively, there is the Expected Reinsurance Deficit (ERD) Test where the threshold is an ERD ratio of at least 1%.

Risk distribution requires that the captive distribute its risk among several insureds. Typical risk distribution tests are meant to ensure that no more than 30%-50% of the risk is from the same insured, and if the captive is a brother-sister insurance company, there must be at least 12 participating entities, each having no more than 15% of the risk.

We also recommend the Coefficient of Variation test to better understand the impact of the law of large numbers. As the number of independent exposures increases the less volatile actual loss experience will become and therefore more predictable.

Employee benefits or not, all captive feasibility studies should address whether there will be adequate risk transfer and risk distribution.

To summarize, a captive feasibility study is one of the most salient parts of placing employee benefits in a captive. Captive owners should aim for feasibility or refeasibility studies that are transparent, objective, highly robust, and consider all aspects of the captive transactions.

I had the pleasure of speaking at The New England HR Association (NEHRA)’s Annual Legal Summit a couple weeks ago. The summit brought together attorneys, CEOs, insurance experts and HR professionals to discuss changes in regulations and laws that directly impact the workplace experience of employees. Some of the major topics discussed included how to adapt to a hybrid workforce, how to know who to hire during and cultural and legal considerations when facing substance use and mental health issues in the workplace. All in all, the conference was a great success and allowed for fantastic networking opportunities and provided guidance around a range of compliance considerations that apply to countless employers nationwide.

During NEHRA’s Legal Summit, I presented on, Piecing Together the Puzzle of the Paid Leave Landscape, in which I dove into history of Paid Family & Medical Leaves (PFML) in the US and explained the current landscape of which states provide PFML (and to what degrees). I moved on to show breakdowns on a global level for paid leave for new fathers, new mothers and for an employee with a health problem. As you’ve probably heard, data shows that the US is far behind when it comes to enacting federal legislation that provides paid family leave in comparison to the rest of the world. Without federal paid leave policies, it has fallen on individual states to create, enact and enforce paid leave policies. Of the fifty states in the US, 23 have rejected PFML proposals and have no safety net for employees who face medical or family issues that would require time off work, unless a program is provided by their employer.

After addressing some of the global and national trends, I explained some of the barriers of access to paid family leave within the US. For instance, women are 20% more likely to leave their jobs when they don’t have access to paid leave and 25% of new mothers return to work less than two weeks after giving birth1. Additionally, when breaking down access to paid leave based on race, research conducted by the National Partnership for Women & Families found that 28% of black respondents reported having requests for leave denied, compared to 9% of white workers. It is clear even within states or organizations that provide some form of paid leave, many Americans are facing very different realities when trying to utilize or understand their paid leave options.

As this was a legal summit, I tackled some of the major questions employers ask about leave surrounding compliance, costs, and leave options if they reside in a state that does not provide PFML. I reviewed some best practices employers can take when developing and evaluating leave policies such as leveraging benchmarks, looking into funding options (e.g. self-insurance, captive insurance, etc.), and utilizing technology and appropriate metrics to evaluate financial impacts. I also noted that different perspectives must be considered when developing leave policies. For instance, employees have different priorities; they are often worried about job security, getting paid and workload upon return when assessing taking paid leave. On the flip side, navigating leave from an employer perspective can be a daunting task when having to traverse FMLA, state laws, ADA/ADAAA, HIPAA, discrimination laws and more; so, it is essential to utilize resources to make sure your company is abiding by all regulatory standpoints.

All in all, I was in great company at the NEHRA legal summit! As per usual, NEHRA hosted some of the leading experts in the field and tackled major topics employers and HR professionals are facing currently. I hope to see many of you again during NEHRA’s 2022 Annual Conference in October.