As seen on Alera Group’s Insights Page

In the cyclical market for Property and Casualty Insurance, we are more than a year into hard-market conditions, leading growing numbers of businesses to consider alternative risk funding. That, in turn, has created an abundance of work for insurance actuaries and Captive Insurance consultants.

OK, that’s a lot of insurance speak for one paragraph. Let’s unpack:

— A hard market for insurance is characterized by a rise in rates, a reduction in options for coverage, heightened scrutiny by policy underwriters and reduced carrier capacity for coverage limits. A combination of catastrophic weather events and so-called “nuclear verdicts” in liability lawsuits — as well as the cyclical nature of the Property and Casualty (P&C) Insurance market — were the driving forces behind the hardened conditions before the onset of COVID-19, and the pandemic exacerbated matters. Rate increases have leveled off to some extent in 2022, but, in general, most conditions in the market remain unfavorable to consumers.

— Alternative risk funding — also known as alternative risk financing or alternative risk transfer — is a mechanism for providing coverage by means other than commercial insurance. Types of alternative risk funding include Captive Insurance programs, in which a business or group of like businesses creates and funds its own private insurance company to cover one or more risks in the realms of both P&C and employee benefits. Workers’ Compensation, General Liability, Auto, Professional Liability and Medical Stop-Loss are the more common coverages to start with when insuring through a captive, but captives often expand into a funding mechanism for many of an organization’s other lines of insurance, including Cyber and Umbrella (also known as Excess Liability Insurance).

— Insurance actuaries use math, statistics and financial models to analyze the cost of risk and determine how much money a company should pay to protect itself against risk. All insurance carriers employ actuaries to help set policy premiums and limits. Some insurance agencies work with actuaries to negotiate policy details with carriers or, in a captive arrangement, to determine a premium that will cover claims and, in the long term, reduce the insured’s total cost of risk. Captives have the advantage of also building up retained earnings over time and allowing companies to take on more risk, generating additional insurance cost savings for the parent. Among multiple P&C capabilities, actuaries who work with or for an agency also educate clients on the cost of risk and how to manage it.

Now that we’ve cleared that up, let’s talk about the role of an actuary in managing the cost of risk and protecting your business with a customized insurance program — whether you’ve chosen to pursue alternative risk funding or not.

Why an Alternative Solution? And Why Now?

Business leaders know all too well about the hard market for Property and Casualty Insurance. Just as the pandemic began to wane early in 2022 and there were some signs of casualty rate increases leveling off, Russia’s invasion of Ukraine escalated supply-chain disruption and fuel shortages, accelerating the rise in economic inflation. Damage resulting from Hurricane Ian only made matters worse, of course, driving reinsurance — insurance for insurers — into what the Bank of America termed a “true hard market” of its own, with rising costs getting passed on to consumers. These issues have led to overall increases in U.S. P&C industry combined ratios over the past few quarters, sparking further rate increases for certain lines.

It’s no wonder more organizations are looking at captives and other alternative risk-funding solutions.

“Overall, between 2017 and 2021, captives added $4.3 billion to their year-end surplus while returning $5.8 billion in stockholder and policyholder dividends, representing $10.1 billion in insurance cost savings over purchasing coverage from commercial market third parties.”

“The number of U.S. captives continues to rise, although the growth of captive formations was tempered by the onset of economic uncertainty resulting from the pandemic, as well as ongoing scrutiny from the IRS and greater regulatory and reporting requirements.”

“However, these adverse conditions can serve to highlight the benefits of the captive segment and provide businesses an incentive to establish them,” said Fred Eslami, associate director, AM Best.

“‘This current environment allows captives to customize coverage for risks that may be uncommon or difficult to write or place in the standard market,’” Eslami said.

The growth in Captive Insurance has led to an increasing willingness on the part of carriers to work with captives and regard them as partners rather than threats, increasing options for captive solutions. And even if an organization in the end chooses to forgo alternative risk funding – either for an entire P&C program or for individual coverages, such as cyber or commercial umbrella – simply exploring an alternative and having it as an option can improve its position in the insurance market.

Actuary Capabilities: Your Data, Your Future

For insurance agents and brokers, designing an insurance program tailored to your industry and company is as much art as it is science. Working with an actuary enables you to incorporate greater amounts of empirical evidence into evaluating risks and determining insurance solutions: Here’s what the numbers demonstrate about your situation now, and here’s what our analysis shows about how you’ll perform using this solution.

While any good broker will work to design an insurance program customized for your business, a broker working with an actuary will be especially well-equipped to design a solution tailored to your unique needs and goals. Among the key issues an actuary can help brokers work through are:

- Determining appropriate retention/deductible levels to help the client reduce the total cost of risk;

- Estimating client retained unpaid claims liabilities at quarter/year-end;

- Estimating carrier letter-of-credit need for a large deductible program;

- Estimating possible retained loss outcomes at various confidence levels;

- Performing a captive feasibility study.

Many brokers work in silos, taking a vertical approach in evaluating risk based on industry. Actuaries generally don’t distinguish by industry; they analyze across various industries, focusing on each individual client’s loss history (including frequency and severity), claim status, policy details, exposures and risk-control program before determining financial projections for the organization. Taking the long-term view allows for consideration of fluctuations in company and market performance over a period of time, and increases the likelihood of long-term savings and profits.

Optimizing Your Insurance and Benefits Solutions

As companies grow, they generally reach a point where their claims experience is predictable across one or more lines of coverage. Able to determine such predictability, an actuary can then help you:

- Minimize your total insurance spend, directing more money to the coverage your business needs the most.

- Reduce spending on the risks you have under control. This is where alternative risk funding becomes viable.

If you’ve reached the point where your business is paying, say, $100,000 to $250,000 in annual premium, a group captive might be the best solution because you probably aren’t yet structured appropriately to meet the insurance tests required to form a single-parent captive and the economies of scale may not be there for a single-parent captive solution. In such a case you may need to diversify your risk with other organizations (heterogeneous or homogeneous) — in a group captive or in a shared-risk pool solution utilizing reinsurance — for at least the time being.

The bigger, more complex, more diversified a company becomes, the more a fully funded, single-parent captive emerges as an optimal solution in which the business is insuring only its own risk. A single-parent captive also allows for more coverage flexibility and transparency than a group captive program. Quite often, both benefits and P&C risks are insured by a single-parent captive.

What drives the decision to move from traditional, carrier-based insurance to a captive program is savings and, ultimately, return on investment (ROI). How? By moving expenditures that create carrier profits into the captive solution. Captives are highly efficient, with very low expense ratios, unlike carriers. Free from providing a carrier with underwriting income and investment income on held reserves, you’re able to retain this income to ultimately generate a profit and facilitate an insurance mechanism that competes with the commercial market.

An Organization-Focused Approach

In taking an organization-focused approach toward financial analysis, actuaries look not only at funding for Property and Casualty Insurance but also at spending on employee benefits. Most captive insureds will see annual savings between 10% and 40% for premiums that flow through a captive instead of the commercial market.

As we approach the end of the year, Alera Group invites you to the final event in our 2022 Engage series of employee benefits webinars, A Look Ahead to 2023: Hot Topics and Trends. Join us on Thursday, December 15 as we discuss benefits financial officers and HR professionals need to think about now — including alternative solutions — as they plan for the year ahead.

ACCESS ALERA’S WEBINAR HERE

As the Cayman Captive Forum starts just this week. We are proud to announce Spring and our consultants have been recognized for multiple awards from Captive International’s Cayman Awards 2022. We look forward to continuing to do excellent captive work in all domiciles, including but not limited to the Cayman Islands.

Spring has been awarded for:

Background

On election day, Massachusetts voters were asked to approve or reject four ballot questions when casting their votes for Governor and Attorney General. The 2nd ballot question focused on regulating Dental Insurance, which if passed would “require that a dental insurance carrier meet an annual aggregate medical loss ratio for its covered dental benefit plans of 83 percent1” In layman’s terms, this means dental insurers will have to spend at least 83% of premiums on patient care instead of administrative costs, salaries, profits, overhead, etc. The legislation mandates that if an insurance carrier does not meet that 83% minimum requirement, they will have to issue rebates to their customers. It further allows state regulators to veto unprecedented hikes in premiums and requires that carriers are more transparent with their spending allocation.

Prior to election day, Massachusetts did not have a fixed ratio when it came to dental insurance and will soon be the first state in the nation to have a fixed dental insurance ratio. Although MA requires reporting from dental plans, there were no regulations on premiums. The proposed law sets up a protocol similar to what the Affordable Care Act (ACA) requires of health insurers, where in Massachusetts health insurance carriers must spend at least 85%-88% of premiums on care.

Over 70% of voters voted in favor of regulating dental insurance, the most one-sided response of all four ballot questions. Although at face value regulating dental insurance may seem beneficial for patients, the impacts are not cut-and-dry, and the legislation may affect multiple parties, from consumers to carriers and dentists and practice owners.

Leading up to election day, general reactions about the legislation from dental insurance carriers were negative, while it was supported by most dental practitioners. In fact, the ballot initiative was brought to fruition, in large part, due to an Orthodontist in Somerville. As we can see from the polling results, the general population, or consumers/patients, were also in favor of question #2 passing.

Potential Impacts

For patients: On the intangible side for patients/consumers, the law would provide some peace of mind that the money they pay for their dental insurance was going, in large part, to their care. There is also an indirect advantage to increased transparency, mitigating the typical confusion that surrounds insurance plans and payments. More tangibly, the change could mean that insurers are willing to cover more procedures as a means to hit their minimum requirement (good), however that could result in dental practitioners charging more (not so good).

For employers: We anticipate that the new law will give employers who sponsor a dental insurance benefit plan more control over pricing and protection against unreasonable rate increases. Since many businesses do not offer a dental plan, or offer it on a voluntary basis, the effects should be relatively small. On the other hand, if the law were to create a change in the number of carriers in the marketplace, this could have an impact on plan and network options and negotiating power.

For dental practitioners: With the change, one perspective is that dental practitioners will be able to better focus on the best care for each patient. They may also see an increase in business and revenue if insurers are allocating more dollars towards care and procedures.

For dental insurance carriers: Dental insurers largely opposed question #2 for obvious reasons, such as restrictions on how much they can charge and additional requirements they need to adhere to, but also for less obvious reasons. For example, some carriers argue that the law will require them to make up for profit loss by raising premiums, warning that they could increase by as much as 38% in the state2. They have reason to believe this law will lead to less competition in the dental insurer marketplace, which typically does not benefit the consumer.

Conclusion

Having worked with Massachusetts employers of all sizes on their benefits, including but not limited to dental insurance, as well as interfacing with insurance carriers, being the broker representative for a large percentage of dental offices in the state and working with MDS, we are looking at this update from all angles. Our expertise and decades of experience in this industry enables us to make the following conjectures about passing of ballot question #2:

- Dental insurance premiums may rise, but at a minimal rate

- We ultimately believe this is a step in the right direction as an advocate both for our employer clients and their employees, and that transparency is a positive attribute largely missing from the healthcare experience today

- Immediate impacts will also be minimal, but we may see some of the other factors mentioned above play out over the next few years

If you have specific questions about how the new law might impact your dental plan(s) or practices, please get in touch. In the meantime, you might be interested in watching our recent webinar, “Why Long COVID Needs Short-Term Attention” as you develop your 2023 benefits strategies.

1https://www.sec.state.ma.us/ele/ele22/information-for-voters-22/quest_2.htm

2https://www.wbur.org/news/2022/10/18/massachusetts-ballot-question-2-explainer

Within the last couple of years, we have seen drastic shifts in the wants and needs of employees nationwide. The COVID era sparked and enhanced new practices and benefits that were not popular in the past, such as mental health resources for remote workers, utilizing tech in HR and addressing burnout. Now that COVID effects are less severe and we have returned to more normalcy in many ways, employers must grapple with remote, on-site, and hybrid work models while keeping their workforce happy and engaged. These trends were evident in this year’s Annual Conference hosted by the Northeast Human Resources Association (NEHRA). NEHRA is one of the leading organizations that brings together HR industry professionals to network and share best practices. This year’s conference took place in Newport, RI and Spring had the pleasure of attending and exhibiting.

Here are some of the areas most focused on this year:

1) Adapting to a Hybrid Workforce

Although hybrid and remote work may seem like the norm for many of us, employers are still struggling to keep their workforce connected and satisfied while retaining efficiency. During the peak of the pandemic, many organizations moved to fully remote and are now looking at whether they will require employees to be in the office full-time, part-time, or not at all. Below are some of the sessions that best tackled this issue.

– A session titled “Driving Career Development in a Hybrid World” explored how the adoption of technologies during the pandemic has led to an increase in professional career development tools, but on the other hand, has prevented many employees from showcasing their true talents.

– In the Closing Keynote Panel, three local HR executives from Mersana, Progress and Ocean State Job Lot explained how their organizations have maintained award-winning workplace cultures with a dispersed workforce.

2) Acquiring/Retaining (Next Gen) Talent

As baby boomers are exiting the workforce and Gen Zers are entering, it has caused a great shift in office culture and employee benefits. Gen Z grew up in a technological world with an emphasis on mental health, and often expect their organization to reflect the same standards. Here are a couple of noteworthy sessions related to attracting and retaining next gen talent:

– During “Bridging the Generational Gap through Wellness Initiatives,” a representative from the Town of Barrington, Rhode Island, described how their wellness initiatives have helped increase retention and alleviate burnout among cross-generational employees.

– Experts from Apprentice Learning and FHL Boston explained how organizations can introduce a workplace culture that attracts young people of color in their “Engage Your Employees to Build an Equitable Workforce for the Future” presentation.

3) Reinforcing Employee Wellness

At previous NEHRA conferences and other industry-related events we have seen a giant emphasis on mental health. This year the topic of mental health resources has taken a back seat and many industry leaders chose to focus on the related subject of employee wellness practices instead, spotlighting the importance of…

a) Creating a Culture

Creating a workplace culture with employees of different ages, experiences, locations, and expectations can be a daunting task as an employer. Below are a few of the sessions that provided insights on how to best establish an inclusive company culture.

– National Behavior Health Leader, Dr. Joel Axler discussed signs and symptoms of someone struggling with mental health challenges employers should look out for during his session “Empathy in the Workplace.”

– Roman Music Therapy Services, Meredith Pizzi spotlighted unique ways HR teams can generate workplace cultures that reflect the company’s vision while also inspiring employees.

b) Just Add Joy!

Creating a workplace culture with employees of different ages, experiences, locations, and expectations can be a daunting task as an employer. Below are a few of the sessions that provided insights on how to best establish an inclusive company culture.

– In the Keynote Presentation titled “Create a Workplace People Love – Just add Joy!” the Co-Founder of Menlo Innovations, Rich Sheridan, suggested organizations move away from outdated corporate traditions and adopt new approaches based on what employees want.

– In the breakout session, “What is Stealing Your Joy? Simple Steps to Bring it Back,” attendees had the chance to openly discuss what obstacles are weighing them down at work and possible solutions.

All in all, the conference was a great success and provided an excellent atmosphere for networking and discussing industry trends. Every year I feel like I’m seeing more young talent, which gives me a good feeling about the future of our industry. I am already excited to see what next year’s conference brings!

Captive International has released the winners for the 2022 US Awards. Spring is proud to announce that our company and our Managing Partner, Karin Landry were selected as winners for Best Feasibility Study Firm and Best Feasibility Study Individual (respectively). We were also highly commended for Best Actuarial Firm, Best Individual Feasibility Study (Prabal Lakhanpal) and Best Actuary (Peter Johnson).

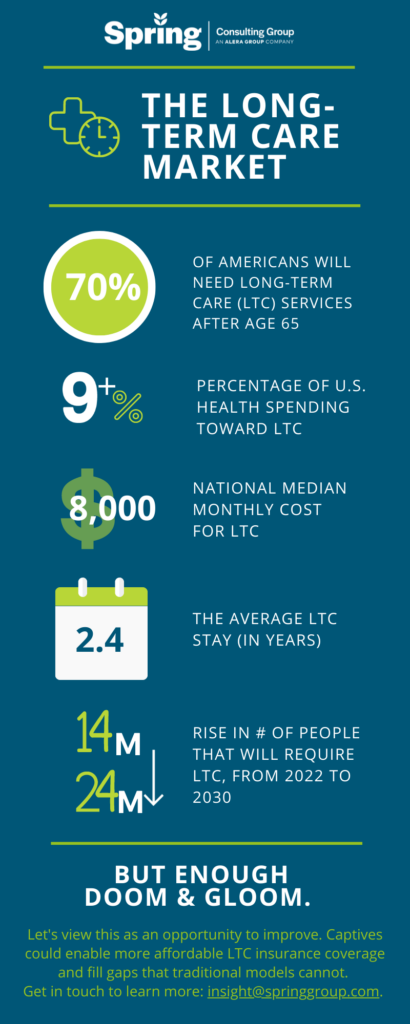

At the VCIA 2022 Annual Conference, our Managing Partner participated in a panel that highlighted the scary long-term care landscape, but that ended on a high note in exploring the possibility of captives as a next generation solution for long-term care insurance.

With innovation embedded in the DNA of both Spring and captive insurance, we are interested in helping reshaping the long-term care market of the future. Check out the other discussions our team members had on VCIA session panels, or get in touch to talk in more detail about long-term care captive strategies.

Pharmacy Benefit Managers (PBMs) serve as intermediaries between insurance companies, pharmacies, and drug manufacturers. Large PBMs are often accredited with securing lower drug costs through volume discounts and aggressive negotiations with manufacturers, which has the potential to make prescription medication more affordable. Unfortunately, many large PBMs lack the transparency that would be required to validate their impact on the cost of prescriptions.

As employers work to find optimal partners, it is important to understand the primary PBM models available in the market and how they align with each employer’s corporate culture. Each model has its own set of pros and cons, so there is not one optimal solution. The key when evaluating is to understand the strengths and weaknesses of the model you are leveraging so you continue to move toward the best approach for your organization and employees. At a high level there are three types of PBM pricing models:

- Traditional Pricing

- Pass Through Pricing

- Hybrid

Traditional Pricing

In Traditional Pricing, also known as spread pricing, PBMs are reimbursed at a higher rate by health plans and self-insured employers than what they are paying manufacturers and pharmacies for the drug. The PBM keeps the difference to offset their administrative costs as well as profit margins. This model is sometimes referred to as spread pricing, which is leveraged by most of the largest PBMs in the market. The model has been highly scrutinized as very little financial data is available and contractual gag clauses often leave insurers and employers with little knowledge of the actual price of the drug. In addition, some prescriptions also have a rebate payment made but only aggregate information is shared, making it impossible for health plans and employers to understand the true cost. With that said, given the buying power of these large PBMs, even with increased spread, employers may still save money within a traditional pricing model.

Pass-Through Transparent Pricing

The Pass-Through Transparent model operates based on the actual costs of the drugs. Clients are billed the amount the PBM is paying the manufacturer and/or pharmacy. All Rx rebates and discounts are passed onto the client. The PBM is compensated not through traditional/spread pricing but through an administrative charge, typically at the prescription level. Although this model seems more economical, PBMs leveraging a pass-through model may not always have the buying power of the traditional pricing PBMs and therefore savings may or may not be realized by health plans or self-insured employers. It is often hard to quantify savings in advance since pharmacy utilization under traditional pricing PBMs are steering utilization to those prescriptions that have the most margin for the PBM in the form of discounts and rebates.

Hybrid

The Hybrid model is a mix between the Traditional Pricing and Pass-Through Transparent models. In this model, rebates and discounts are typically passed to client(s), but it may or may not be in full. Some hybrid models indicate all received rebates are passed back to clients but may have an intermediary that receives some spread that is not disclosed and not considered a rebate. In short, hybrid PBMs have diverse disclosure practices. At a quick glance it may seem more transparent, but it’s difficult to validate.

Solving for the Transparency Issue

With the lack of transparency, some policies at the state and federal level aim to decrease the complexity. For example, most states with transparency laws require reporting from manufacturers when wholesale cost is increased above a certain threshold. The first drug transparency law was passed in 2016 in Vermont, but now over 20 states (including CA, CT, ME, MN, NV, NH, ND, OR, TX, UT, VA, WA, WV) have implemented their own requirements. Maine has one of the more robust approaches, collecting and analyzing the data with the goal of identifying each supply chain’s average net, allowing the public and policymakers to follow the money through the supply chain[1].

The Consolidated Appropriations Act also has requirements for pharmacy reporting that will require PBMs to report on some data that is rarely shared, including but not limited to rebates by drug for the top 25 prescriptions. In some instances, PBMs will share that data with health plans and self-insured employers; in other instances, they will file directly with Centers for Medicare & Medicaid Services (CMS) without employers understanding those plan details.

More recently, on May 24, 2022, the Pharmacy Benefit Manager Transparency Act of 2022 was introduced. Sponsored by Senator Chuck Grassley (IA) and Senator Maria Cantwell (WA), this bill will empower the Federal Trade Commission (FTC) to increase drug pricing transparency and hold PBMs accountable for unfair practices that increase cost. It also will require PBMs to report to the FTC the amount of money they make through spread pricing and pharmacy fees[2].

While we wait to see if the Pharmacy Benefit Manager Transparency Act is passed, other solutions are available. There are companies that are striving to help clients save money when it comes to prescription drug costs. They often run analyses on current employer prescription drug costs to determine how much they could save if they moved away from traditional PBM models.

At edHEALTH, we work hard with our member-owner schools to bend the trend in healthcare costs. Pharmacy continues to be an expensive cost-driver, at a national level, and something we’re addressing head-on. We continuously look for opportunities to bend the trend in healthcare costs, including exploring all options to reduce prescription drug costs.

Tracy Hassett, President and CEO of edHEALTH

When our client, edHEALTH, carved-out prescription drug benefits, the goal was to provide additional savings and transparency to its members. edHEALTH continues to work with their vendors and evaluate various options so that they can offer additional transparency and cost savings. To learn more about potential solutions, talk to your current advisor or reach out to Spring Consulting Group.

[1] https://www.nashp.org/drug-price-transparency-laws-position-states-to-impact-drug-prices/

[2] https://www.natlawreview.com/article/pbms-continue-to-draw-federal-scrutiny-pbm-transparency-act-2022#:~:text=The%20Pharmacy%20Benefit%20Manager%20(PBM,and%20state%20attorneys%20general%20in

The World Health Organization defines burnout as: a syndrome conceptualized as resulting from chronic workplace stress that has not been successfully managed and recognizes three identifying characteristics of the phenomenon:

- Feelings of energy depletion or exhaustion

- Increased mental distance from one’s job, or feelings of negativism or cynicism related to one’s job

- Reduced professional efficacy

Burnout has gained its status as a bona fide buzzword for good reason. A recent survey by Indeed found that 52% of workers were feeling burned out, up 9% from pre-COVID times; while a 2021 American Psychological Association study showed that 3 out of 5 employees reported negative impacts of work-related stress, such as lack of interest, motivation, and energy. The impacts of burnout go beyond an unhappy workforce. In fact, employees struggling with burnout are:

- 63% more likely to take a sick day1

- 23% more likely to visit the ER1

- 2.6 times as likely to look for a different job2

- Less likely to participate in meetings or projects, which can have a negative influence on company culture

All of these factors contribute to lost productivity, a drain on both financial and non-financial resources (e.g., other team members needing to take on more from a burned-out colleague, or resources spent on replacing employees that have resigned due to burnout), and overall a workplace environment that is far from ideal. Although every industry is struggling with burnout, healthcare and higher education are industries with unique challenges. Both require a higher onsite presence than other industries and have experienced a lot of change related to the pandemic.

At this point, you have likely heard the term burnout and understand its prevalence, but perhaps don’t have a clear path forward to prevent or mitigate the issue.

What to Do About Burnout

If you notice a team member seems less engaged or enthusiastic, tangibly overwhelmed, is declining in performance, or just less present – these are all flags for burnout. Often burnout can be nipped in the bud before getting to a more extreme state if you know the signs and have tactics in place toward resolution. Often supervisors will notice these signs early in the process, which means training related to burnout and compassion are imperative.

From a quantitative perspective, we’ve seen organizations successfully respond to employee burnout by implementing or boosting the following:

- Facilitation of work-life balance, by offering resources to help employees find that balance

- Regular monitoring of responsibilities and schedules

- Encouragement, or even a mandate, to use paid time off

- Flexibility regarding hours, place of work, etc.

- Management training including how to deal with burnout, and establishment of best practices

- Creation of clearly defined career paths and professional development opportunities

- Open, frequent, and honest communication

- Wellness programs and tools

- Protocols for recognizing accomplishments where the work matches the reward

On the more tangible side, wellness tools like Headspace, Calm, and Noisli have been developed to tackle stress, focus, and productivity. There is also a range of virtual counseling and mental health platforms available for employers to provide additional support to employees. At Spring Consulting Group, we have access to a platform called Spring Health, which offers counseling services, Employee Assistance Programs (EAPs) and more.

Burnout solutions must align with your organizational goals and demographics. I mentioned that industries like higher education and healthcare have different forces at play, which need to be accounted for in a burnout strategy. It can be a challenge to know where to begin but expanding on current offerings can be an easy first step as well as surveying employees to understand what services would be considered value-add to most participants. The key is to know burnout is negatively impacting your population and if unaddressed it will compound an already burdened attraction and retention strategy. The time is now to make it a priority and find solutions.

1https://thrivemyway.com/burnout-stats/

2https://www.gallup.com/workplace/237059/employee-burnout-part-main-causes.aspx

Executive Summary

Musculoskeletal (MSK) conditions are a driving force behind healthcare spending, representing an estimated 17% of all spending in the US healthcare market. In addition, MSK conditions are the leading contributor to disability worldwide.1 Some examples of MSK conditions include osteoarthritis, rheumatoid arthritis, osteoporosis, sarcopenia, back and neck pain, and fibromyalgia.2 MSK pain may be acute or chronic, localized or affecting the entire body.3 Additionally, conditions may or may not be related to work, creating an added layer of difficulty in understanding the condition and addressing individual patient needs.

Many models currently exist that attempt to control costs related to MSK conditions. While the vendors providing these programs are confident in their success, it can be difficult for employers to select a program that addresses the needs of all employees with relevant conditions. Therefore, a thorough and ongoing review of organizational health data is necessary. For example, what a hospital needs in an MSK program may vary greatly for an employer operating solely out of an office setting. When reviewing workers’ compensation claims, how many are MSK related? If there is a concern, employers may want to start by implementing ergonomic reviews where the employee works to ensure there is nothing at work that is negatively impacting the employee. Other attempts to address MSK costs focus on care and treatment after the injury or disorder exists such as overall wellness programs, one-on-one coaching, and digital physical therapy offered as an employee benefit.

What is the impact on healthcare spend?

– Musculoskeletal (MSK) conditions are the top cost driver of healthcare spending, followed by heart disease, cancer, and diabetes.

– The average health cost per member with MSK condition increased by 40% between 2010 and 2019.

– COVID-19 aggravated this trend as more workers shifted to remote work; 70% of employees with MSK conditions experienced new or increased pain.4

-The Department of Labor’s Bureau of Labor Statistics estimates that about 30% of workers’ compensation injuries fall under MSD.5

As costs have increased, traditional approaches to treating MSK conditions have not shown a corresponding improvement in patient outcomes. This may include surgery, advanced imaging, injections, and pain management.6 It may be time to consider alternative treatment options to appropriately address these rising costs and employee pain levels.

What alternative models exist?

As employers, employees and providers begin to understand that traditional treatment options may not be the best approach for specific cases, alternative approaches have grown in popularity. Workers’ compensation claimants receiving opioids dropped from 55% to 24% between 2012 and 2018, while there was a 131% increase in the use of massage to address chronic pain, a 26% increase in the use of orthotics, and a 15% increase in the use of physical therapy, according to the National Council on Compensation Insurance (NCCI).7

Employers who have identified a significant impact of MSK conditions on their claim costs should seek programs that can be added to their benefit offering. There is a large market for these alternative treatment options, some components of which are listed below:

- Digital physical therapy clinics using wearable technology

- Pain relief wearable technology

- Custom physical therapy programs and coaching, in person or remote

- Case review by leading medical providers

- Therapy addressing psychology and education of conditions and pain

- Remote work ergonomics

- Focus on chronic pain management

- Corporate wellbeing programs

Specialty MSK vendors track data that implies overall success including a 50% to 70% reduction in pain, 40% to 75% reduction in anxiety and depression, increased adherence and participation in programs, surgery avoidance, and return on investment for employers.

What should I do as an employer interested in an MSK program?

Employers must begin by understanding the cost associated with musculoskeletal conditions within their population, as well as the range of conditions employees may be experiencing. If costs (medical and pharmacy) are significant or increasing, employers should consider alternative programs that would benefit employees and the plan. Identifying a pattern may demonstrate the need for a specific approach like preventive programs or ergonomic assessments.

From there, market research will be necessary to understand pricing and select a vendor with the best program for your population. Spring’s consultants are here to help with market research, claims and data analysis, and/or a Request for Proposal (RFP) process so that you find a solution that best meets your organizational needs.

1https://www.businessinsurance.com/article/00010101/NEWS08/912336312/Musculoskeletal-disorders-in-comp-highlight-prescribing-changes, https://www.who.int/news-room/fact-sheets/detail/musculoskeletal-conditions

2https://www.who.int/news-room/fact-sheets/detail/musculoskeletal-conditions

3https://my.clevelandclinic.org/health/diseases/14526-musculoskeletal-pain

4https://healthactioncouncil.org/getmedia/a738c3c5-7c23-4739-bb8d-069dd5f7406b/Hinge-Health-State-of-MSK-Report-2021.pdf

5https://www.businessinsurance.com/article/00010101/NEWS08/912336312/Musculoskeletal-disorders-in-comp-highlight-prescribing-changes

6State of MSK Report 2021, Hinge Health

7https://www.businessinsurance.com/article/00010101/NEWS08/912336312/Musculoskeletal-disorders-in-comp-highlight-prescribing-changes